Good morning! The Agenda is now complete.

In macro news, the main item today is a Federal Reserve interest rate decision at 6pm (UK) / 2pm (Eastern Time), when the Fed is expected to hold rates at 4.5%.

News filtering is here! Stockopedia has a brand new News Feed. Check out the release notes here.

Today's DSMR is finished, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Rio Tinto (LON:RIO) (£79.7bn) | Statement: AGM resolution | Rio explains why it recommends shareholders oppose a resolution to unify its dual-listed structure. | |

M&G (LON:MNG) (£5.3bn) | Full Year Results | Adj operating profit +5% to £837m, operating capital generation -6% to £933m. New progressive dividend policy, dividend +2% to 20.1p. Net flows negative | AMBER/GREEN (Graham) Very confident noises by management today and they have increased their cost target by another £10m to £230m. I'm a fan of many aspects of this business but it is a little more complex than other fund managers and does have some very heavy adjustments applied to these results. On that basis I hold back from taking an outright positive stance. |

Softcat (LON:SCT) (£3.2bn) | Half-year Report | 2024 rev +17%, op profit +10%. 2025: H1 slightly ahead, now exp >10% FY25 op profit growth. | GREEN (Roland) A strong set of figures as this IT reseller continues to win new customers and persuade existing customers to spend more. Upgraded full-year guidance today suggests momentum remains strong. I think this may justify a positive view, despite a fairly full valuation. |

Alpha International (LON:ALPH) (£1.0bn) | Full Year Results | Rev +23%, organic +20%. Adj PBT +10%, margin 35%. +ve momentum, confident outlook. | |

Serica Energy (LON:SQZ) (£542m) | Triton FPSO update | Repairs taking longer than expected. Prod not exp restart before May (prev mid-late Mar). | AMBER/GREEN (PINK) [no section below] (Roland holds) The rusty old Triton is still causing trouble, limiting SQZ’s production. It’s not good news and Serica is working with operator Dana to improve matters. However, I think a more material factor for shareholders at the moment is whether a mooted combination with North Sea rival Enquest goes ahead. My hope is that 25% SQZ shareholder Mercuria will ensure a decent deal in any negotiations. Under takeover code rules, a decision is due on 4 April. |

Ferrexpo (LON:FXPO) (£489m) | Full Year Results | Rev +43% due to volumes, EBITDA -30% on lower iron ore prices. Net cash $101m. | |

Advanced Medical Solutions (LON:AMS) (£465m) | Full Year Results | Rev +43% inc acq, +10% organic. Adj PBT +14% to £29m.4. 2025 outlook in line with exps. | |

Judges Scientific (LON:JDG) (£455m) | Full Year Results | SP +4% Revenue down 2%, adj operating profit -29% to £28m. Organic order intake +7% vs ‘23. 2025 YTD in line with expectations. 2025 has started well with order intake "slightly ahead" of last year, and with a coring expedition for major subsidiary Geotek. The long-standing Chairman retires. | AMBER (Graham) [no section below] I'm maintaining my neutral stance. For a few years now, the main problem has been that Judges is unable to find acquisition targets that are a) attractively valued and b) large enough to move the needle. Hopefully this changes soon. c. £17m was spent on acquisitions in 2024. Other concerns include: Demand from China has proven to be volatile, net debt is over £50m, and the shares continue to trade at a hefty earnings multiple (c. 19x). Therefore while I do have huge admiration and respect for what Judges has achieved historically, prospects from the current level strike me as uncertain. Stockopedia ranks it currently as a "Falling Star" - in general, this is considered to be a losing category of investment. See coverage in January for further background. |

Essentra (LON:ESNT) (£332m) | Full Year Results | Rev +0.3%, adj PBT -15% (constant FX). End markets mixed. 2025 exps unchanged. | |

FDM (Holdings) (LON:FDM) (£244m) | Full Year Results | 2024 in line: rev -23%, adj PBT -32%. Divi -38% to 22.5p. 52 new clients (‘23: 47) & net cash. | GREEN [no section below] (Roland) Today’s half-year results have received a positive reception despite showing a sharp drop in profit. Net cash of £41m provides a margin of safety, while a 10% operating margin highlights FDM’s ability to flex its cost base. The 2024 dividend gives a 9% yield at current levels, albeit FY25 forecasts (unchanged today) suggest a further cut to the payout this year. If expectations for a return to growth in FY26 are accurate, I think FDM could offer value at current levels. |

Filtronic (LON:FTC) (£228m) | Expanded Strategic Agreement with SpaceX | Agreed to increase supply of SSPA modules. 10.9m warrants issued to SpaceX at 92.8p. | AMBER/GREEN (Roland) FY26 earnings forecasts remain unchanged today despite an increase in sales. Filtronic’s operating costs are rising as the group scales up and profits are expected to fall next year. I’m concerned by dependence on SpaceX and the lack of visibility beyond FY26. But I can’t ignore strong recent growth and recognise that Filtronic could be well positioned to continue expanding in the LEO satellite sector. |

| Big Technologies (LON:BIG) (£221m) | CEO Suspension | SP down 28% yesterday Concerns re: conduct over lawsuit relating to an acquisition. | |

Science (LON:SAG) (£184m) | Bank Refinancing & Ricardo Investment | Refinanced RCF & loan - these facilities have been increased and extended. Has net cash of £14.1m. Strategic investment: Average cost of RCDO shares is 231p including costs. They now own 16.1% of the company. | AMBER/GREEN (Graham) [no section below] |

1Spatial (LON:SPA) (£71m) | TU | SP down 10% Profit warning - looks like a miss against exps. Rev £33.4m, adj. EBITDA £5.6m+. Positive outlook. | |

AFC Energy (LON:AFC) (£57m) | Full Year Results & Strategic Update | Rev £4m, net loss £17m. Closing cash position £15m. Material uncertainty re: going concern. | |

Ten Lifestyle (LON:TENG) (£55m) | HY TU | H1 rev c. £31.8m (+5% at constant FX). Various contract launches/ renewals. Net cash £6.8m. | |

Nexteq (LON:NXQ) (£41m) | Full Year Results | Adj. PBT -67% ($4.8m). Net cash $29m. Destocking but order book improvement expected in 2025. | |

Centaur Media (LON:CAU) (£39m) | Full Year Results | Rev £35.1m, adj. EBITDA £5.9m ahead of £5.6m exps. Outlook: solid foundations for 2025. | |

Gelion (LON:GELN) (£17m) | Interim Results | Total income £0.4m, reflecting grant income. Adj. EBITDA loss £2.9m. Cash £3.5m. | |

4Global (LON:4GBL) (£10m) | TU | Profit warning caused by delivery schedules. Rev £5.1-5.3m, adj. EBITDA £0.9-1.0m (prev: £1.9m). | |

LPA (LON:LPA) (£8m) | AGM Statement | On track to deliver market expectations. H2 to be much stronger than H1. | |

Plexus Holdings (LON:POS) (£7m) | Proposed Placing, Subscription & Retail Offer | Up to 54m new shares (existing share count: 105m) to raise up to £3.5m. Directors to invest £2m. | AMBER/RED (Graham) Enormous dilution for existing shareholders who don’t take part in the fundraise. But that’s all part-and-parcel of investing in early-stage companies. This is now back in startup mode after the previous business plan didn’t lead to sustained financial success. |

Companies Reporting

Plexus Holdings (LON:POS)

Up 5% to 7p (£7m) - Proposed Placing, Subscription and Retail Offer - Graham - AMBER/RED

Disclosure: our former colleague Paul is a shareholder in Plexus.

I’m covering this as it’s #2 on Stockopedia’s “Most Viewed” widget today.

This company provides a range of wellhead equipment for purchase and rental to oil and gas operators. Its technology is said to be extremely safe and cost-effective.

Financial performance has been up-and-down:

Like the share price:

A recent AGM statement talked about a refreshed strategy under their new CEO, targeting offshore opportunities: Carbon Capture & Storage, and Plug & Abandonment work. It also had ambitions in product development and in finding new strategic partners.

Full-year results to June 2024 showed the company having a cash balance of £2.5m. Officially there was balance sheet equity of £15.4m but this wasn’t liquid, with a big chunk of intangibles and a smaller chunk of PPE taking up most of the value.

Therefore, the news that the company wishes to raise funds doesn’t strike me as hugely surprising. The small existing cash balance doesn’t match the scale of their ambitions.

Some details of the fundraising announced today:

Placing and subscription to raise £3m. Of this, directors to subscribe for £2m.

Retail offer for up to £0.5m.

Pricing: 6.5p, only marginally below latest share price 6.7p.

If it all goes ahead this will increase the share count by over 50% (54 million new shares).

It’s an enormous amount of dilution for any existing shareholder who doesn’t take part in the fundraise. But this is par for the course, for very small companies who need additional fund. If the business plan succeeds then I doubt that many shareholders will be complaining about dilution.

Use of proceeds:

The net proceeds of the Fundraise will be primarily used to fund the manufacture of eight additional sets of Exact-Ex wellhead equipment, which will double the Company's rental fleet and enable Plexus to capitalise on the growing demand for Jack-up rental wellheads for deployment on exploration and P&A projects

Loan note: an outstanding convertible note held by directors will be converted into equity, creating an additional 13.5m shares.

Graham’s view

I’m going to take an AMBER/RED stance on this due to what I perceive as very high risk levels.

The existing business did have one very good year (FY June 2024), thanks to one “major special project” and a licensing agreement. But that hasn’t fed through to sustained financial success, which has led to this fundraising. My perception is that they are back in startup mode. There’s nothing wrong with that, but it’s inherently speculative. I would tread cautiously.

M&G (LON:MNG)

Up 3% to 227.6p (£5.5bn) - Full Year 2024 results - Graham - AMBER/GREEN

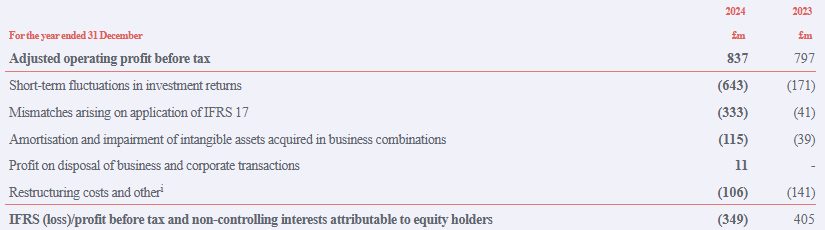

This asset manager has released full-year results for 2024, with the robust profit number standing out to me:

Adj. PBT £837m (2023: £797m)

Net outflows £1.9bn (2023: net inflows £1.7bn). Continued (but reduced) outflows from UK institutional clients, offset by continued inflows from international clients.

Assets under management rose to £346 billion (Dec 2023: £343.5bn), helped by positive market movements

Unfortunately there is a statutory loss of £347m (2023: statutory profit of £309m). Let’s immediately get to the bottom of this. The main adjustments are shown here:

The £643m loss in “short-term fluctuations in investment returns” was caused by rising yields, rising interest rates and rising equity values. M&G hedged itself against falling rates and falling equity markets, but this meant that it incurred a loss when the opposite happened.

It’s reasonable to look past this when calculating underlying profitability, but the size of the numbers involved - £643 million being more than 10% of the company’s market cap - should give us pause for thought.

“Mismatches arising on application of IFRS17” - I’m happy to look past this entirely as it relates to how long-term annuity contracts are accounted for. The negative mismatch number is expected to unwind over time.

Amortisation - the usual considerations apply.

Restructuring - this is something I don’t like to allow, as companies very often have reasons to restructure, so I’m reluctant to treat it as an exceptional charge. Note that the restructuring charge is over £100m for both of the last two years.

Let’s turn to the CEO comment for a snippet. Note that the cost reduction target does help to explain high restructuring charges. The new 2025-2027 targets have grabbed headlines:

…we are today announcing two new targets for 2025-2027: to grow adjusted operating profit before tax on average by 5% or more per annum, and to generate £2.7 billion of operating capital.

We also remain focused on operational efficiency as demonstrated by the reduction in the Asset Management Cost-to-Income ratio from 79% to 76% excluding performance fees and the £188 million cost savings delivered by our transformation programme so far. We are not resting there and are upgrading our cost target, for the second time, from £220 million to £230 million by the end of 2025.

The 2025 cost savings target was initially £200m.

Outlook, key points:

Geopolitical uncertainty/market volatility weigh on client sentiment

Confident M&G are well positioned for profitable growth over long term

Continued confidence in delivery of financial targets

Dividends: new progressive dividend policy. The previous policy was for “stable or growing dividends”, so this does signal confidence in the company’s ability to deliver higher payments.

Graham’s view

I’m positive in general when it comes to asset managers, due to the cheap valuations on offer.

With M&G, however, it seems to me that there is a greater level of complexity. I’ve read and re-read their explanation of the adjustments to their accounts today, and I’ve previously managed with-profits funds. However, I’m still a little fuzzy on some of the adjustments that have been applied to these results.

And with some of the adjustments being very large, this makes me a little more cautious than I am with other fund managers.

On the bright side, it’s difficult to deny that management are making improvements in terms of cost reduction and simplification. Net flows are fine and AUM is stable.

And I like the heavy weighting that M&G has in fixed income, as it’s an asset class less suited to passive investing.

I can take a moderately optimistic view on this (AMBER/GREEN)

Roland's Section

Filtronic (LON:FTC)

Up 1% to 105p (£230m) - Expanded Strategic Agreement with SpaceX - Roland - AMBER/GREEN

Filtronic plc (AIM: FTC), a leading provider of high-performance RF, microwave, and mmWave components and subsystems for the defence and space markets, is pleased to announce a significant development in its strategic partnership with SpaceX.

We have covered Filtronic a number of times in these pages this year – check the archive here. I’ve also published an in-depth Stock Pitch on the company that provides more background. So in this update, I just want to focus on the potential impact of today’s news.

Filtronic says it has expanded its existing April 2024 partnership with SpaceX “to enable an increased allocation of business to Filtronic”:

As part of this agreement, Filtronic will increase its supply of advanced E-band SSPA modules to support the ongoing deployment of SpaceX's Starlink constellation, which provides high-speed, low-latency internet to users worldwide.

These E-band SSPA modules are being used to upgrade and expand Starlink’s network of ground stations. This is the product that’s driven the company’s spectacular growth over the last year.

Warrants: Filtronic has issued SpaceX with 10.9m warrants. These entitle the US firm to subscribe for up to a maximum of 5% of Filtronic’s existing share capital (subject to receipt of irrevocable purchase orders). They have an exercise price of 92.8p, allowing SpaceX to buy at a c.12% discount to the current market price.

This is the first of two 5% tranches of warrants SpaceX is entitled to, subject to order volumes. I believe the threshold for entitlement to these warrants was c.$30m of orders.

If SpaceX exercises these warrants, it will raise around £10m for Filtronic, at the cost of some dilution to shareholders.

Outlook: as a result of today’s news, CEO Nat Edington believes Filtronic is now trading slightly ahead of previous forecasts for FY26:

This gives us greater visibility and confidence that we are trading marginally ahead of market expectations for our financial year ending 31 May 2026.

Updated estimates: the company doesn’t provide any updated figures, but we do have updated broker forecasts for FY26, with thanks to Cavendish.

Cavendish’s analysts have increased their revenue forecasts for FY26, but not their profit forecasts. The reason given for this is higher operating costs, due to engineering recruitment. FY25 forecasts are unchanged:

FY25E revenue: £50.4m

FY25E EPS: 5.0p

FY26E revenue: £46m (previously £43m)

FY26E EPS: 3.2p (unch)

Roland’s view

Today’s update highlights a few points on which I think investors need to form their own view.

Earnings visibility & margin dilution: Filtronic’s sales are expected to fall by c.10% next year, while its earnings are expected to fall 36%, based on their house broker’s forecasts.

Margins are also expected to weaken, suggesting that the company’s growing scale may be putting pressure on profitability. Of course, it’s possible that this is temporary, dependent on future growth.

One potential concern for me is the lack of visibility beyond FY26.

The previous narrative on this is that the current programme of upgrades to Starlink ground stations is expected to complete in the next financial year.

The second stage of the SpaceX agreement is said to be dependent on Filtronic delivering new technologies in FY26 and winning customer orders to drive growth in FY27 and beyond.

Presumably there’s scope for significant further growth, but it’s not guaranteed. As outsiders, we have zero visibility on this process. Unfortunately, with the stock trading on over 30 times FY26 earnings, I think there is a certain amount of cliff-edge risk here:

SpaceX customer concentration: it’s clear to me that Filtronic is heavily dependent on SpaceX at the moment. What I would like to understand better is whether SpaceX is dependent on Filtronic products. Are suitable alternatives available?

Shareholder dilution: this isn’t a huge issue for a growing business, in my view, but it’s not ideal and seems to favour SpaceX over existing shareholders. I’d prefer to see SpaceX exercise its warrants at the current market price.

I’m going to take a slightly more positive view than I have previously on Filtronic and go AMBER/GREEN following today’s update. While my concerns are unchanged, the reality is that both momentum and profitability remain strong. I don’t see anything in today’s update that’s likely to alter Filtronic’s High Flyer status.

Softcat (LON:SCT)

Up 12% to 1,830p (£3.7bn) - Half-Year Report - Roland - GREEN

Yesterday we covered results from valued-added IT resellers Computacenter (I hold) and Bytes Technology. Today we have half-year figures from the UK’s third large listed IT reseller, Softcat.

Softcat plc (LSE: SCT.L), a leading UK provider of IT infrastructure products and services, today announces its half year results for the six months to 31 January 2025 ('the period').

As with CCC and BYIT yesterday, SCT’s results have also been well received by the market:

Half-year summary: today’s headline numbers cover the six months to 31 January 2025 and seem very positive:

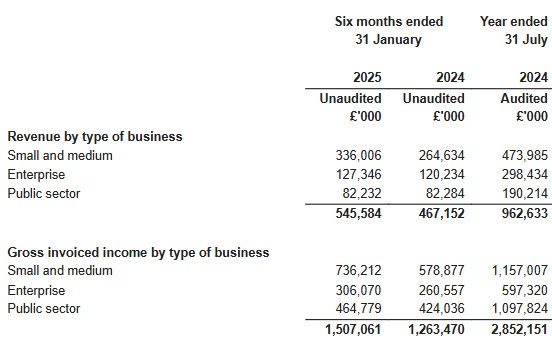

Gross invoiced income up 19% to £1,507.1m

Statutory revenue up 16.8% to £545.6m

Operating profit up 10.4% to £73.7m

H1 operating margin: 4.9% (H1 24: 5.3%)

Earnings up 12.3% to 28.7p per share

Interim dividend up 4.7% to 8.9p per share

(Softcat calculates operating margin as a percentage of gross invoiced income, rather than statutory revenue. The difference reflects whether the company is acting as a principal or agent in its transactions with customers. The company warns peer group comparisons are “not uniform”.)

Perhaps more importantly from the perspective of investors, today’s results are said to be slightly ahead of expectations. This has prompted Softcat’s board to upgrade its full-year guidance (my emphasis):

Outlook: operating profit growth in the first six months of the financial year is slightly ahead of the Board's expectations. We continue to expect to deliver another year of double-digit gross profit growth in FY2025, with operating profit growth now expected to be low double-digit, up from high single-digit previously.

Trading commentary: companies in this sector have reported somewhat mixed trading over the last year and CEO Graham Charlton also describes a “persistent backdrop of generally more challenging trading conditions”.

So what lies behind Softcat’s strong growth? My understanding is that this is very much a sales-driven organisation. The CEO explains it slightly differently:

Our progress is attributable to the breadth of our offering and sustainability of our growth model, powered by Softcat's special culture and the differentiated customer service it delivers.

Helpfully, he then splits out growth between new and existing customers:

During the period we made further good progress against our two key strategic goals: winning new customers, up 1.4% year-on-year, and selling more to existing customers, with an increase of 10.7% in gross profit (GP) per customer.

Demand was said to be particularly strong in security, networking and data centre infrastructure – unsurprisingly, perhaps.

Softcat has branches in Europe, APAC and an office in the US, but the company doesn’t provide a geographic split of revenue.

However, it does provide a split across customer segments. This highlight’s Softcat’s historic strength in SME and its growing presence with larger customers – a segment led by Computacenter in the UK:

Outlook: the company provides updated FY25 guidance on gross profit and operating profit today:

Gross profit: “another year of double-digit gross profit growth”

Operating profit: “now expected to be low double-digit” (previously “high single-digit”)

Consensus forecasts on Stockopedia ahead of today suggested earnings could rise by 8% to 64.2p per share this year.

Based on the commentary in today’s results, I think it’s reasonable to tweak these estimates a little higher – perhaps to +10%, or c.66p.

That would price the stock on a FY25E P/E of 27.

Roland’s view

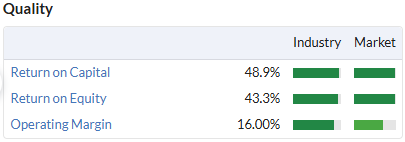

Softcat shares don’t look cheap at face value. But the company has delivered operating profit growth at nearly 13% CAGR since 2019 and benefits from very strong quality metrics:

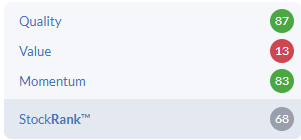

This combination of high quality and momentum and poor value is reflected in the StockRank and High Flyer styling:

However, I think it’s fair to suggest that this level of profitability and growth supports a premium valuation.

It’s also useful that Softcat carries net cash, although as is normal with this type of business, there’s a large balance sheet relative to profits:

H1 25 receivables: £609.5m

H1 25 payables: £440.8m

H1 25 operating profit: £73.7m

Profits and cash generation for distributors and resellers often come from leveraging supplier credit and earnings a small margin on high volumes – that’s true here, I think. There’s a degree of risk in this, although when well managed it can help to support impressive growth.

One positive for me is that like Computacenter, Softcat still benefits from significant founder shareholding. In my view, this is likely to help ensure management maintain good financial discipline:

Softcat shares have seven-bagged since the company’s IPO in 2015:

While the value investor in me would probably prefer to wait for a time when Softcat shares are less popular, I can’t argue with the stock’s High Flyer credentials or its track record since listing. GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.