Serco (LON:SRP) is a FTSE 100 listed support services and outsourcing company. It has over 100,000 employees, international operations and provides a wide range of operational and process related services. Recent contract wins include ground maintenance in Canterbury, operation and maintenance of a new Bus Rapid Transport System in Indore, India, and an extension to continue running the Docklands Light Railway.

Shares in Serco Group currently trade at 560p.

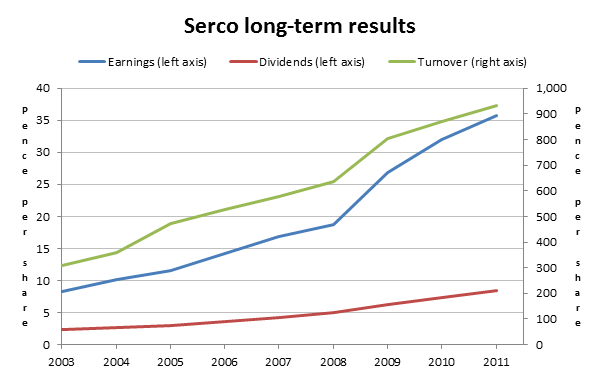

Financial results

Any investment in shares should be seen as a long-term commitment. The standard advice is to have a time horizon of five years or more, and I think that’s sensible.

Since you should be expecting to hold your shares for five years or more, it makes sense to look at the long-term financial results of the company, rather than just what they’ve done in the last year or two, as you may still be holding the shares five or ten years from now.

Growth – Serco’s growth rate is about 18% a year over the last decade. In comparison, the companies that make up the FTSE 100 have grown on average by about 4% a year over the same period, so Serco’s growth rate is some 350% higher than average.

There is an element of industrial “wind at their backs” when it comes to this growth rate though.

I own shares in MITIE, Mears and Interserve, all of which are in broadly similar support services and outsourcing businesses. Each of these companies has seen rapid growth over the last decade and more, partly due to the outsourcing boom which has taken place in that time.

This means that much of Serco’s growth is probably driven by being in a growth industry, rather than being driven by some general superiority over its peers.

Consistency – Serco is top of the class in terms of consistency, with a 100% track record of profitability and dividend payments, and a 100% record of growing sales, earnings and dividends in every single year. By comparison, the FTSE 100 companies as a whole have only hit these targets 74% of the time.

Debt – Debt levels at Serco are somewhat high, but given the consistent and growing nature of the company, this may not be a problem.

Debt interest payments (£28 million) are around 11% of recent profits. While I prefer…