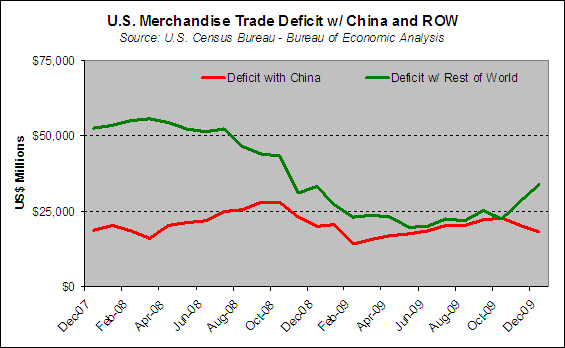

Trade figures out of the United States and Canada today confirm that the global recovery is slowly moving forward. Looking at the trade of physical goods is one of the best measures of economic momentum. In my look at these figures last month, the story was of robust German trade in November. That robustness softened for Germany in December and now the focus has returned to the United States, where the trade deficit has widened further.Japan put in a strong showing, while Canada still struggles to return to a trade surplus. In all, "normalization" is happening and trade is returning to incremental growth. This, of course, means that the United States trade deficit is on the rise again. Yet, this is not coming from its trade dynamic with China as many might assume.

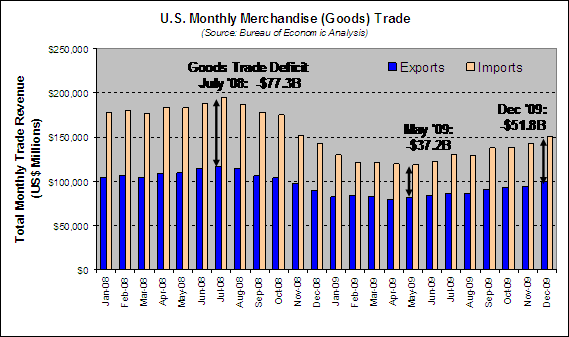

U.S. trade grows as does the trade deficitU.S. trade ended the year on a strong note. Monthly totals for merchandise trade (imported and exported goods) reached $244B, about 30% above their lows in February of last year. This rise has returned trade levels back to early-2007 levels but has also brought back the growth in the U.S. trade deficit. This deficit in goods in December stood at -$51.8B but is moderated to -$40.2B when services are factored in.The pessimistic view holds that, as trade recovers, the U.S. deficit growth spurs new borrowing that must be funded by China and other countries. One counter to this is the fact that the deficit is a third less than it was in early 2007. Additionally, recent deficit growth is more the result of energy imports and prices than the U.S.-China trade relationship.

China is starting to buy from the U.S. en masse

While conventional wisdom often links the U.S. trade deficit with U.S.-China trade issues, the pattern might not be holding. Thanks to surging purchase of U.S. goods by China, the deficit has narrowed in the past two months. These purchases remained consistent at roughly $5.5B throughout last summer before jumping 18% in October, 7% in November and another 14% to $8.4B in December. Prior to that, such Chinese purchases had never reached $7B, even in the best of economic times.It is as if China is no longer satisfied holding dollars and bonds as IOUs for future purchases but, rather, is cashing that paper…