“Coming out of a recession and into a vigorous economy, the cyclicals flourish” - Ex-Fidelity fund manager, Peter Lynch. The UK's economic outlook has been improving over the last few years, bringing good news for cyclical industries like automobiles and housebuilders. This is because cyclical stocks typically rise faster when the economy improves, but fall harder when the going gets tough.

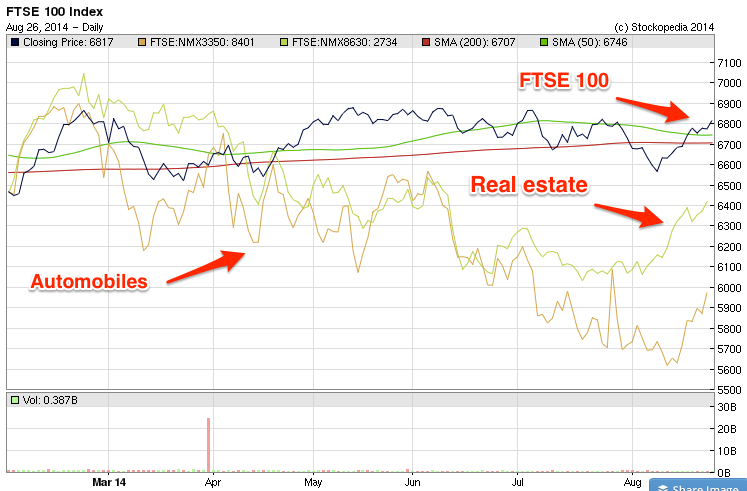

Cyclicals have outperformed the FTSE 100 since around 2009, but charts suggest that some sectors have taken a breather since early 2014. Automobiles and real estate in particular have under performed the FTSE since the start of the new year (see chart below). This is partly because investors are probably fearful of a rise in interest rates, which would of course harm sectors that have been fuelled by cheap consumer credit in recent years.

The question is whether Mr Market is acting rationally, or acting on emotion and fear. Quantitative checklists are a useful way to keep our emotions in check, so this week we take a look at a couple of cyclical companies that have recently qualified for Stockopedia’s GuruScreens.

Lookers

The motor retail service company, Lookers, has the characteristics of a cyclical stock, and looks well placed to take advantage of improving consumer confidence. The company’s earnings dropped by 17% during the crash of 2008 as consumer budgets tightened. Lookers’ share price took a hit. A quick glance at the chart below shows that the share price plummeted by a gobsmacking 90% between April 2007 (176p) and March 2009 (16p).

However, consumer demand has been picking up. The company’s annual report notes that “volumes in the UK car market have returned to a more normal level of activity in conjunction with further improvements in the UK economy.”

This trend has helped Lockers grow earnings each year since 2010, but investors will be asking whether this growth is sustainable. Peter Lynch liked to keep a close eye on inventories to assess consumer demand. He explains that when “inventories grow faster than sales, it’s a red flag”, because it suggests that demand is starting to weaken.

In the case of Lookers, inventories have generally been declining in relation to sales. The Inventory Turnover ratio has indeed been getting higher, implying strong sales and demand (see Table 1). Furthermore, brokers expect earnings to grow by 28% in…