On Monday, as I was looking for investments to potentially replace stocks in a portfolio I'm fast feeling is no longer obviously cheap, I stumbled back upon my thoughts on Quarto group a couple of months ago. The price is more or less the same, and I remember being bullish then, so I booted back up the spreadsheet and clicked back on their website, only to find they were reporting results two days from then.

On Monday, as I was looking for investments to potentially replace stocks in a portfolio I'm fast feeling is no longer obviously cheap, I stumbled back upon my thoughts on Quarto group a couple of months ago. The price is more or less the same, and I remember being bullish then, so I booted back up the spreadsheet and clicked back on their website, only to find they were reporting results two days from then.

That's always a slightly uncertain moment for me, because I'm still not sure what I feel about buying directly before results. If I'm of the conviction that the stock is undervalued, surely the balance of risks on every results day is going to be positive - it's more likely to surprise (since, if the stock is cheap, expectations are implicitly low) on the positive and see upwards share price movement. I think that logic is solid, but I rarely follow it. I prefer to wait for results and see where the cards lie before making my decision. Perhaps that's just my all too-human aversion to being in the dark. Maybe I pay a premium for the privilege!

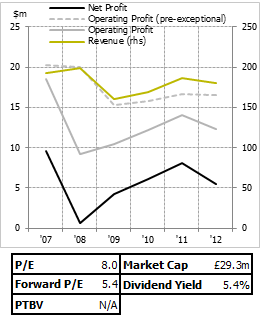

Either way, the business is obviously functionally the same as it was in my look at it the last time, with two posts; one focusing on the business, and one focusing on the figures. Click through to those for a more complete representation than I'll put here, but to sum up the business in one sentence; Quarto are an international book publisher who focus on non-fiction books - manuals, 'lists' etc. - which makes their revenues and operations less volatile than fiction publishers.

What do the half-year results tell us about how the business is progressing? Well, not a lot, but perhaps that's a good thing given that I was thinking of buying. It meant the price of the company stayed roughly flat today. It is interesting to see co-founder Robert Morley resinstated to the board after his departure in all the Orbach-related intrigue last year (discussed in first post). The company's working on the usual objectives one comes to expect when a company gets ruffled up - debt reduction and cost reduction. In Quarto's case, there's also a notable hat-tip on digital revenue, after Orbach's level-headed but evident scepticism meant they had a rather…

.png)