One-line summary

RWS Group is a profitable and well managed company, with a defined moat of expertise, but EU legislation threatens its business model and this uncertainty will take many years to play out.

Introduction

RWS Group are one of those low-profile, sensibly-profitable, cash-rich companies that many investors like to have in their portfolio. They may not be a household name but in the world of technical translation for global corporates they appear to be a "go-to" kind of firm. Even better while their listed history, on AIM, extends only to 2003 the group can trace its patent translation roots back to 1958. So that provides a lengthy track-record and a sensible name (derived from Randall Woolcott Services) as good points already!

In addition RWS Group is a proper growth company with turnover tripling, and profit increasing five times over, during the past decade. Most of this has been generated organically, with only a few targeted acquisitions here and there, and the company truly provides global operations serving multiple industry verticals.

What's not to like? Well such success has drawn the attention of government regulators; they, quite sensibly, see the mish-mash of national patent laws as a sizeable frictional cost for business and a deterrent to innovation. Back in 2008 the London Agreement came into force with the explicit goal of reducing the volume of translation required. Now the European Unitary Patent is moving slowly towards ratification. These risks will be considered later but before that I'm going to look into the quality of earnings, the sustainability of cash generation and the equity used to support both of these.

Excellent track-record

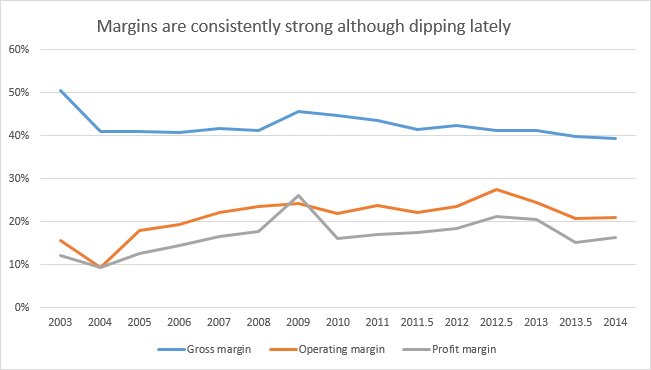

When looking at a new company I always check out the various profit margins (gross, operating and net). This gives me a feel for how much pricing power the business has and whether they have good control over their sales and administration costs. If any of these margins are slim (less than 10% say) then that's a cause for concern.

Fortunately RWS is able to command decent margins and these show very little volatility:

However the margins have fallen off 2-3% in the last couple of years and much of this…