It feels like a lot of companies have come to market recently. Poundland, Pets at Home and Boohoo.com hold very little appeal for me at current valuations - and the whole IPO process is one which immediately makes me a little suspicious, anyway. There is one company which caught my eye enough (just post IPO) to give them a proper read through, though. I was planning to write this post last week, but the imminent publication of their full year results for 2013 gave me enough of a reason to sit on my hands and twiddle my thumbs for a while longer. I now look at them with a round 33% more financial data (four years of results instead of three!). Quite the boon.

It feels like a lot of companies have come to market recently. Poundland, Pets at Home and Boohoo.com hold very little appeal for me at current valuations - and the whole IPO process is one which immediately makes me a little suspicious, anyway. There is one company which caught my eye enough (just post IPO) to give them a proper read through, though. I was planning to write this post last week, but the imminent publication of their full year results for 2013 gave me enough of a reason to sit on my hands and twiddle my thumbs for a while longer. I now look at them with a round 33% more financial data (four years of results instead of three!). Quite the boon.

Many of my UK readers will, I suspect, have heard of Safestyle. I might go so far as to read your mind with regard to the first thought, which I suspect will be this; one of those adverts so annoying it becomes memorable.

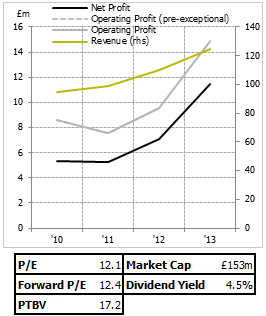

For those who don't know them, they are a manufacturer/distributor of windows. They're the largest seller of replacement windows in the UK, which is a market worth about £2bn a year and which has a surprisingly fragmented structure; their market share sits at 7.9%, with Anglian and Everest (which I assume are the other two in the top three) pooling 20% between them. The rest is made up of smaller, regional players. Their positioning - if you couldn't tell from the advert - is distinctly at the value end of that spectrum. From anecdotal experience, Safestyle are significantly cheaper than their competitors. The scale of that cost difference - as well as the incentives at work in replacement windows (how long are you planning to stay in the house for? How much do you care about quality?) likely explain Safestyle's continually increasing market share; 4.4% in 2007 and 7.9% now. The value proposition to customers appears to be sticking.

They manage all of this with a relatively slim amount of capital; their corporate structure is extremely (overly?) light on commitments. 'Asset-light' is a term you often hear, but with Safestyle it goes one step further; their door-to-door canvassers are self-employed, their installers are self-employed and their sales team is self-employed. Obviously, there are logistical and cost benefits to this, but I feel a little suspicious…

.png)