Good morning, Paul here.

Please note that I added a section on Treatt (LON:TET) (in which I hold a long position) interim results to yesterday's report, which is here.

Apology to Wargamers

Something really strange has happened on Twitter over the last couple of days. My account started to be bombarded with pictures of happy people on their wedding days. Most of the pictures were very nice, but I had no idea why they were being sent to me.

Anyway, it turns out that someone decided to stir up a Twitter storm, by copying some daft, tongue-in-cheek comment that I'd made here (in Jan 2014) describing customers of Games Workshop (LON:GAW) as nerds who never get married!

Now obviously, readers of my blog would understand that I often throw a daft aside into my commentary, just to raise a smile and lighten the mood a little. Also, there was a bit of irony involved, as I've never got married myself! Poking fun at myself, and others, is what I do sometimes. However, in text form, the intention can sometimes be misunderstood by others. So I should have chosen my words more carefully - a good learning point for me.

Taken out of context though, and copied to Twitter into a group reinforcing situation, I can see how people would take umbrage. Therefore I think the decent thing is to apologise.

Apology - on reflection, my comment was ill-considered. It was only intended as a joke, and had no malice behind it whatsoever. However, given that a whole bunch of people on Twitter have decided to take offence, then I retract my comment, with my apologies, and will amend the original article to remove my daft comment once I've finished today's report.

As a general point, I think urging people to spam any Twitter account with which you disagree, is wrong. However, sending pictures of happy marriage scenes is actually quite a nice way to protest! It's better than the abuse that usually pertains on Twitter.

Oh apparently I further put my foot in it, by saying that my favourite comedy is the Big Bang Theory! lol. Just to clarify on that point, I think it was hilarious up to series 4, passable in series 5 & 6, and terrible ever since.

Anyway, if any wargamers want to stick around, you're very welcome here. You could learn a lot about successful small caps investing from me & the gang here! Your input on GAW would be very interesting too, next time I report on it.

Good. On to today's news.

Today I shall be reporting to you on the following;

Vertu Motors (LON:VTU) - results for y/e 28 Feb 2017 - car dealership group

W7L - results for y/e 31 Dec 2016 - recently floated make-up vendor

Michelmersh Brick Holdings (LON:MBH) - AGM trading update - brick manufacturer

Plus anything else of interest that crops up.

Vertu Motors (LON:VTU)

Share price: 48.25p (up 7.2% today)

No. shares: 397.3m

Market cap: £191.7m

Final results - year ended 28 Feb 2017.

This is a car dealership chain. Its website is here. It operates from over 120 sites nationwide, with multiple car brands.

There's a useful results video (8 mins) from the company, courtesy of BRR Media, here.

These numbers look good. The company had previously said that new car sales were down, but used car sales and aftersales (servicing, etc) up. A few key numbers;

Revenues up 16.5% to £2,823m - most of this increase has come from acquiring new sites. Within that figure, organic growth was 4.4%. That looks a good result, considering new car sales were down 6.4% on a LFL basis.

Used car sales were strong - up 7.1% on a LFL basis. It's interesting to how the link between new car sales and profitability, which the stock market usually assumes to be the case, actually isn't the case. Poor new car sales has been compensated for by increased used car, and aftersales, and margin improvements.

Outlook & current trading look surprisingly good. There's a lot of detail in this, and sounds encouraging to me;

In March and April 2017 ("the post year-end period") the Group has continued to trade strongly, with profits ahead of the prior year on a like-for-like and total basis. Margins strengthened and operating expenses on a like-for-like basis were reduced as the cost base was flexed for lower new vehicle sales volumes and cost efficiency programmes delivered.

Used cars continued to see like-for-like volume growth and margin improvement. Service also witnessed growing revenues and stable margins on a like-for-like basis.

The March plate change month saw a record number of new vehicle registrations in the UK according to the SMMT. The 4.4% growth in March new retail UK registrations was aided by an element of pull forward of demand due to increasing vehicle excise duty from 1 April 2017 and the timing of Easter. April, as anticipated, saw a decline in SMMT new retail registrations of 28.4%.

In the post year-end period SMMT new retail registrations declined by 3.5%. The Group saw significant growth in new retail vehicle profit contribution in the post year-end period despite a 9.7% decline in like-for-like new retail volumes. Pricing disciplines and cost control delivered higher margins and profits year on year in new vehicle sales.

The Board is also pleased to report an excellent contribution in the post year-end period from dealerships acquired in the previous financial year.

While the Board is aware of the wider reporting of the UK entering a more cautious consumer environment, trading in the post year-end period has been strong. The Board remains confident about the Group's prospects for the current financial year and in delivering further progress in enlarging the scale of the Group.

Balance sheet - looks alright to me. Although as with all car dealerships, there is a vast amount of working capital tied up - massive inventories, financed mainly with massive trade creditors - i.e. the money owed to the manufacturers & other suppliers.

In this case, NAV is £246.4m, which reduces to NTAV of £150.4m. Therefore about 78% of the market cap is supported with tangible net assets - a fairly secure position, in my view.

Potential problems - one of the reasons car dealers are cheap at the moment, is because of Brexit worries. Could this stifle the importation of cars from Europe? Personally I very much doubt it - why would the Germans allow the EU to cripple their export industries? (the UK apparently takes about 20% of the entire output of Germany's car companies). Although in reality, at this stage, nobody knows. So it's educated guesswork for investors to a certain extent.

The other potential issue is that of possible mis-selling of personal contract hire vehicles. We've seen how the banks were clobbered with mis-selling of PPI, which cost them billions. Could this be a risk for car dealers? I have no idea, but it's being discussed in the press as a possibility, so is bound to weigh on share prices somewhat.

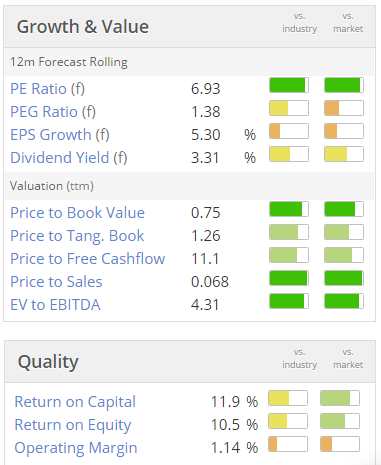

Valuation - as you can see from the Stockopedia graphics below, the share looks dirt cheap - on the most popular valuation metric of forward PER.

My opinion - I like it. It's not one I hold personally at the moment, as I'm focusing more on growth shares. That said, am really tempted to buy back in, as the valuation seems compelling.

It's not often you find a reasonably well financed company, paying divis, which has reported strong results & outlook, and is on a PER of around 6 or 7. There could be upside here, if the various downside worries sort themselves out in due course.

The StockRank is 82, so Stockopedia's computers rather like it too!

Michelmersh Brick Holdings (LON:MBH)

Share price: 68.7p (down 0.4% today)

No. shares: 81.5m

Market cap: £56.0m

AGM statement - this sounds a solid update;

"After a very satisfactory trading performance in 2016, I am pleased to report that the Group has performed well for the first four months of 2017. The Board expects the Group's trading performance for the twelve months to 31 December 2017 to be in line with market expectations.

I reviewed its 2016 results here, if you're interested.

Warpaint London (LON:W7L)

Share price: 224.5p (up 8.2% today)

No. shares: 64.5m

Market cap: £144.8m

Final results - for the year ended 31 Dec 2016. Very late published accounts - why so late?

This is a cosmetics company, including owning the W7 cosmetics brand.

It listed on AIM on 30 Nov 2016. So this is my first time here reporting on it. Although I do recall reviewing the prospectus last year at home, but don't have my notes to hand (if I made any). It looked quite interesting I thought at the time, but not enough to make me want to invest.

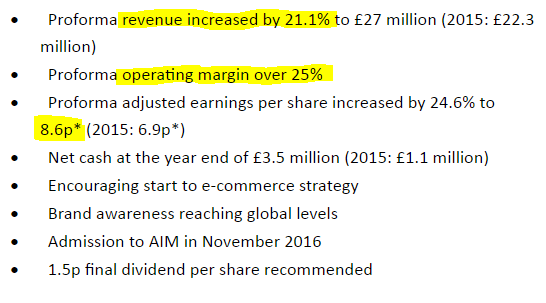

The highlights section today looks good, in particular my eye is drawn to the decent growth, and excellent operating profit margin;

Stockopedia shows a broker consensus forecast of 7.9p, so the 8.6p reported today looks a decent beat.

The PER is 26.1- so it looks fully priced, maybe even a bit toppy? Although that depends entirely on what profit growth is likely in future.

Outlook comments sound alright;

Warpaint enjoyed many years of successful growth prior to joining AIM and we are confident that with increasing awareness of our brands we remain well placed to continue this expansion.

The Company remains at the forefront of developing on trend products for its ever discerning range of customers. Overseas business will continue to be a major driver as we aim to gain a larger share of the global colour cosmetics market.

With a flexible supplier base and a tight control of working capital the business remains inherently cash generative...

...The current year has started well and we look forward to updating shareholders on our progress.

Balance sheet - this looks strong.

There are hardly any fixed assets - so a capital light, highly profitable business - positive attributes.

Working capital is very strong, with a current ratio of 3.97 - therefore this is a well financed business, with no worries at all about solvency.

Also, it has no debt, with only £278k of long term liabilities - so insignificant.

It has £3.5m in cash, and no debt.

So a big thumbs up from me here - this is a solid, well-financed business.

Dividends - 1.5p final divi has been declared. Interim divis prior to the IPO need to be ignored, as circumstances were different then. So I'm not sure what the divi yield is likely to be going forwards - I'm sure broker notes will estimate this, but I haven't looked at any today, as this share doesn't really interest me particularly.

My opinion - these look good figures, but the share price reflects that, being on a fairly high rating.

I know nothing about cosmetics, so have no idea how sustainable the company's bumper profits would be. On the basis of strong figures today, and a sound balance sheet, this share might be worth a closer look. The sector doesn't interest me though, and I wouldn't know how to assess the business model.

Finding out what the target market thinks of the product is key. So a good excuse for readers to ask lots of ladies what they think of the W7 brand make-up, perhaps?

I tend not to trust recent IPOs. So for me, it's one I'll keep on the watch list, as well as asking my niece what she thinks of the W7 product.

That's it for today.

I'm pleased to report that the mobile phone repair shop has managed to fix my iPhone, after its encounter with a synthetic fibres (well, I do my clothes shopping mainly in Primark, so lots of polyester) 1400 rpm spin cycle over the weekend. So if your smartphone suffers a similar watery death, then my advice is to rush it to a decent mobile repair shop immediately, before it rusts, and they might be able to fix it.

You see - small cap shares analysis & views, wargaming controversy, and practical consumer advice - my reports here really are a one-stop-shop for everything you could wish for! ;-)

Kind Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.