Good morning! I had a second wind again last night, and added comments on James Latham (LON:LTHM), Accsys Technologies (LON:AXS), and the takeover bid for Nationwide Accident Repair Services (LON:NARS). So to recap on yesterday's full report, please click this link. As you've probably already gathered, I'm more of an evening than a morning person!

Mello Workshop

Many of you know David Stredder ("Carmensfella"), a highly successful small caps investor, and creator of the Mello investor events. These are going from strength to strength, and after the tremendous success of the 3-day event in Derby last year, we are rapidly approaching the next event, which is a slightly different format, and will be held in Peterborough, on Thu 23 & Fri 24 April 2015.

The format this time focuses on investor workshops, run by experienced investors, on many interesting themes, such as "hidden nasties on the balance sheet and how to spot them", "how to use spread betting to your advantage", and many others. It should be another excellent event, of interest to investors from beginners to experts, and tickets are selling fast, so I do urge you to come along if you can. I'll be there for the two days, and am having my arm twisted to do a couple of sessions - one on balance sheets, and one on my (disastrous) experiences in 2008 from being geared up in illiquid stocks during the financial crisis. So hopefully people can learn from me what not to do with spread betting accounts, since I learned the hard way unfortunately.

There will also be about 20 or more interesting smaller caps - David hand-picks the companies at these events, and refreshingly, doesn't waste your time with dodgy junior resources stocks!

More info & sign up links are here.

STOP PRESS! Mello have kindly given us a special discount code! So if you enter this code in the box at the top of the booking form, you'll get a discount: STOCKDISC

Koovs (LON:KOOV)

Share price: 65p (down 45% today)

No. shares: 24.1m

Market Cap: £15.7m

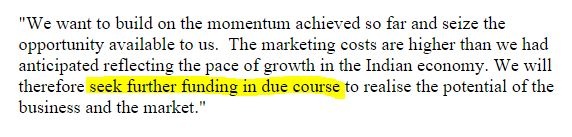

Trading update - the market is seriously unimpressed with this update, with the shares down 45% this morning. Growth for the year ended 31 Mar 2015 has been strong in percentage terms, with sales up 268%, but it's coming from a very low base, so £720k last year, and £2.65m this year just finished.

Koovs is an early stage fashion website in India, and it was hyped up as being the next Asos, since its Chairman, Waheed Alli was involved with Asos for many years.

Trouble is, it's not easy to create a successful fashion business online. People mistakenly think there are few barriers to entry, whereas actually you have to invest a considerable amount in warehousing, stock, the website itself, but then of course you have to spend millions on marketing to drive customers to the website.

In this case the company says it spent £3.2m on marketing in the y/e 31 Mar 2015, so that's more than their entire turnover! This was almost three times what was originally planned.

There was net cash of £12m at the year end, so at £15.7m the market cap actually looks quite reasonable, and I would have been prepared to take a punt at this level. However, the fly in the ointment is this statement, which looks a massive own-goal to me;

My opinion - telling the market that you have £12m, but that you're going to spend the lot and come back for more, is a ridiculous thing to do, in my opinion. Of course the shares are going to be smashed down, because everyone will just wait for the Placing, instead of buying in the market now.

Having said that, I am tempted to have a nibble at this level, as the market can suddenly change its focus to growth rather than cash burn. Also, maybe existing shareholders might tell the company to manage with the cash they already have, rather than agreeing to a further fundraising? Lord Alli owns 19.6% of the company himself, so presumably will not be keen on dilution at this sort of price, which makes it all the more perplexing as to why this has been handled in such a ham-fisted way.

The market is being brutal at the moment towards micro caps that come back fro more cash, just look at what happened with Synety recently - its share price halved on a tiny follow-on fundraising.

Forbidden Technologies (LON:FBT)

Share price: 7.25p

No. shares: 131.8m

Market Cap: £9.6m

Prelimiary results - for calendar 2014 are out, and they're not a pretty sight. Turnover actually fell, to only £689k, but operating losses ballooned from £824k in 2013 to £3.6m in 2014.

It looks like there is enough cash in the bank to last for the rest of 2015, but unless future sales make a step change of multiple 100%'s, then it's difficult to see there being much of a future here. The business model just isn't working so far, and probably needs a complete re-think.

The company describes 2015 as "an attractive challenge", which makes you wonder what the CEO is smoking! I wish the company well, but it doesn't look an appealing investment proposition at all, unless they can start delivering dramatically improved sales. So my caution about this share has been proven correct.

So few jam tomorrow shares actually deliver the expected level of jam, that it amazes me the market continues to price them so aggressively on initial hope, which rarely succeeds.

Renew Holdings (LON:RNWH)

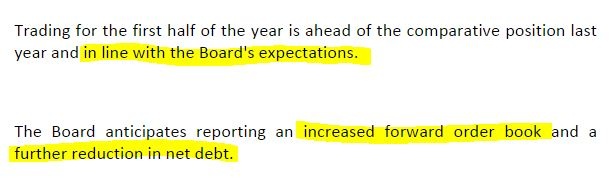

Trading update - this reassures on H1 performance;

My opinion - this group of civil engineering companies seems to be trading well, with the main profits coming from rail framework contracts, and the boom in high end property (excavating basements) in London. A number of other contracting companies have been bolted on, in various acquisitions.

The main problem here is that the balance sheet has a serious deficiency of capital, which the company is able to work around, due to favourable working capital characteristics - i.e. customers paying up-front, and some costs being deferred using subcontractors.

Competitor Costain (LON:COST) recently repaired its balance sheet with a fundraising, and at some point Renew needs to do the same thing. They should fix it whilst the sun is shining, in my opinion.

FW Thorpe (LON:TFW)

Acquisition - it's good to see this lighting company do something useful with its surplus cash pile, that has been sitting on the balance sheet doing nothing for years.

Thorpe is buying a Dutch lighting company called Lightronics. About £5.7m is being paid for a 65% stake, with the balance being deferred for 3-6 years, and the final payment being based on the same earnings multiple as the initial purchase, which sounds a sensible way of keeping management (who are the sellers) motivated. Dutch management are also contractually locked in.

Lightronics made an profit margin of about 10% on sales of E13.9m in 2014. Given that Thorpes has a 30 Jun year end, the acquired company will only make a minor contribution to group profits in this year, but will kick in for the full year for y/e 30 Jun 2016.

The impact looks to be about a 10% increase in the run rate of group profitability, assuming that Lightronics performance in 2014 is typical.

My opinion - this is a good example of how companies with surplus cash on the balance sheet can make acquisitions which drive up earnings. This deal should take Thorpes EPS up to a run rate of about 10p. So at 153p the shares are probably priced about right.

Checking back to my report here on 19 Mar 2015, I flagged that Thorpes had £33.9m in net cash, and that there was potential for acquisitions. So this deal at £5.7m, plus an additional loan amount (amount not stated, but some part of £3.1m), still leaves Thorpes with a substantial cash pile - worst case scenario of c.£25m. So we could perhaps see more European acquisitions in future?

Nice company, and this looks a sensible deal. The shares look priced about right for the time being, in my opinion.

Stanley Gibbons (LON:SGI)

Share price: 242p (down 9.6% today)

No. shares: 46.8m

Market Cap: £133.3m

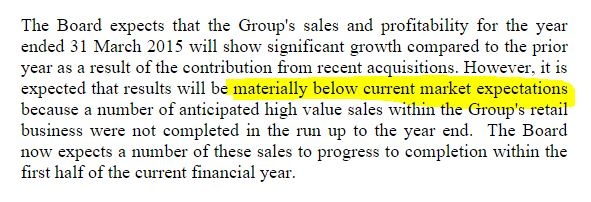

Trading update - oh dear, it's a "materially below" profit warning;

However, there is quite a lot more detail in the announcement, and the outlook comments sound upbeat, so that might explain why the shares have bounced from the initial opening low this morning.

Broker consensus is for 20.2p EPS this year, so "materially below" could be anything from about 18p downwards.

I see that the Chairman has bought 22k shares at 238p today, a £52k vote of confidence. Although I am increasingly ignoring PR-driven Director buys after bad news, as it's becoming increasingly obvious that advisers are urging Directors to buy in order to prop up the share price. Therefore I feel that following Director buys is becoming a far less useful indicator than it used to be, now that it is being used as a routine method to manipulate the share price. Although it does at least reassure that things are not absolutely dire, but there was not really any suggestion that was the case here anyway.

Overall, this share doesn't appeal to me, although I note that it has been a reaonable dividend payer in recent years - no gaps in the sequence, and steady increases in the payout most years. It's the type of share that I would only consider if it was on a single digit PER, and paying a divi yield of 5%+, and the valuation is some way above that right now.

Audioboom (LON:BOOM)

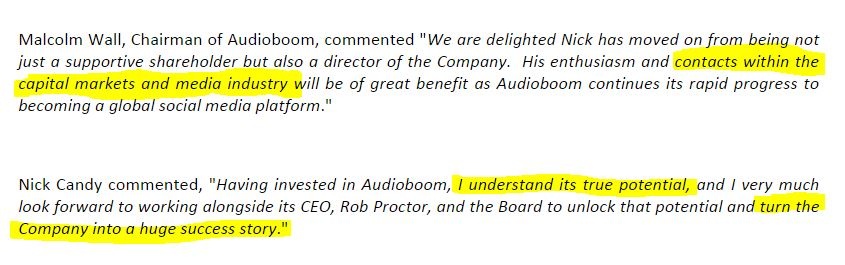

Nick Candy - has been appointed as a new Non Exec at this social media App. The Candy brothers of course are top end London property developers, so are wealthy & well connected. That doesn't mean they can suddenly transform Audioboom into a viable business!

It all fits the hype over substance mould in which Audioboom is firmly lodged (in my opinion). Candy owns 15.65m shares (2.9%), and in an unusual step (normally taken by companies which are out of cash, which is NOT the case here), instead of taking a fee for acting as a Non Exec, Candy has been granted warrants to subscribe for 12m new shares at 8.375p.

That looks reasonable to me, since the strike price is the same as the current market mid price. However, if the share price of Audioboom were to double on the next speculative surge, then Candy's warrants would be £1.0m in the money. The beauty of warrants of course is that they have no downside risk - if the share price is below the exercise price, then you just let them lapse on expiry.

Put another way, 12m warrants would, if exercised, become 2.26% of the company's enlarged share capital. So giving a new Non Exec the risk free upside on 2.26% of the company in lieu of fees, strikes me as a bit irresponsible on the part of the company. Will a Non Exec with no apparent relevant sector expertise, really add that much value?

The comments from both parties reinforce my view that this stock is mostly about hype, and that the £46m market cap looks irrationally high. The argument is that you can value social media website/Apps on a per user basis. Well, yes and no. You can do if it's something like Facebook or Twitter, but a free App that distributes largely non-unique content, hmmmm I'm sceptical.

This was a lovely speculation last year, and was one of my best gains in 2014, but I'm a lot more sceptical about it now, because there is no viable business model that is apparent, with turnover to date being negligible, and ongoing losses until the cash runs out, now looking the most likely outcome.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.