Good morning! I was settling down to my evening meal last night, when the phone rang. It was the CFO of Avation (LON:AVAP). I had been rather negative about some aspects of the company's interim results statement, so he wanted to chat through the numbers and clarify a few points. It's always slightly awkward when I've been critical of a company, and they then get in contact, but it happens quite a lot, and as long as my criticisms have been fair, then I stand my ground.

In this case, the CFO was refreshingly honest, in saying that my criticism was fair, and that he took full responsibility for not explaining the numbers clearly enough in the narrative to the results statement. I should emphasise that no new information was given to me, but he did explain the way in which rapid growth in the aircraft fleet had skewed the figures somewhat.

So what originally looked like a big miss against forecast, will probably turn out to be reasonably alright, as the H2 numbers are expected to be stronger than H1, due to H2 containing a full 6 months income on the newly leased aircraft - and with the operational gearing of more income flowing through a fixed cost base that should boost H2 profits vs H1 profits. Sounds reasonable to me.

Rather than repeating it all here, I just want to flag up that I added a new "Update" section to yesterday's report, explaining what was said on my phone call with the CFO. So for anyone interested, that is in yesterday's report, in the Avation section, just below the chart.

I like talking to company management, as it helps me understand the business better. Although some scepticism is necessary, as obviously they will always talk up the company's performance and prospects - that's part of their job!

I'm reassured that my decision to buy a few more Avation shares yesterday morning was probably a sensible one, but time will tell.

Pinnacle Technology (LON:PINN)

This is only about a £3m market cap, so I won't spend more than a few moments on it. There are hardly any results out today, so I've had a quick look at this micro cap's results for the year ended 30 Sep 2014.

The results are absolutely terrible! A £1.9m loss, on turnover of £8.4m. Even adjusted EBITDA is negative, at £512k. The balance sheet is bad, and the company is out of cash. So it looks to me as if they are about to go bust. So I've checked the RNS, and there was a small fundraising in Nov 2014 of £0.6m before expenses (so maybe £0.5m after expenses?), which might keep the wolf from the door for a little while longer perhaps? Costs have been reduced too, including closure of their own data centre.

It seems to me that the company needs to either go private, and/or raise a sensible amount of money to shore up its balance sheet. It never seems to have made a profit, and looks to me very much like a lifestyle business, with little prospect of upside for outside shareholders, but high risk of downside. So very much the opposite of what I look for.

Good luck to them, but it's not for me, and I've added it to the bargepole list.

Unfortunately there's nothing left of the barrel for me to scrape - Fridays are always quiet, but today is bizarrely bereft of results & trading updates.

STOP PRESS! UPDATE AT 17:00

Mar City (LON:MAR)

Share price: 67.5p (down 31% today)

No. shares: 110.3m

Market Cap: £74.5m

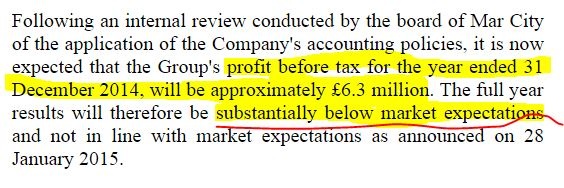

Profit warning - this is an absolute disaster. The company has put out a profit warning today, just three weeks after a previous trading update which said that everything was fine, and they were heading for 2014 profit before tax of "more than three fold the previous year".

Checking back, in the 2013 accounts profit before tax was £3.2m. Therefore the company was saying on 28 Jan 2015 that 2014 profit would be over £9.6m. The 28 Jan 2015 update is full of positive commentary, and doesn't give any hint that anything is wrong. Unsurprisingly, this positive update triggered some buying, and a modest share price rise.

Now we come to today's update. Where do I start?

1. Related party debtor balance - £31.2m was owed at 30 Jun 2014 to MAR by another company that is controlled by Tony & Maggie Ryan (who are both Directors of MAR, being CEO & COO respectively).

Today's statement says that this balance is currently £29.5m, but that £10.0m is "expected to be received next week". So assuming that £10.0m is indeed received next week, then that leaves a balance of a £19.5m debt due to MAR by its own CEO & COO.

It now appears that they haven't got the money to repay it. So instead, a "proposed property acquisition" is being done, whereby the Ryans will sign over £14.5m of property assets to MAR, instead of paying in cash. Independent valuations are currently being undertaken on the properties concerned.

The remaining balance that the Directors are not able to repay, of £5.0m, "will be eliminated by 31 December 2015". Note the use of the word "eliminated". So what does that mean? Another offset agreement for any other stray property assets they've got lying around? Written off? Who knows.

The assets comprising the £14.5m offset arrangement seem to include partially completed flats in Colindale, North London. The flats are likely to be completed in Jun 2015. They are being dumped onto MAR's balance sheet, pending disposal basically.

As this is a major related party transaction, independent shareholders will be invited to approve this transaction at a general meeting. I hope as many shareholders as possible attend this meeting, and absolutely read the Riot Act to the Directors of this company. What on earth do they think they are doing, behaving in this way with a Listed company? It's outrageous!

2. Trading update - it gets worse! (and as usual, sorry about my wonky highlighting!)

Two reasons are given;

(a) A revaluation surplus of £3.5m on some residential properties that were going to be retained (and presumably rented out) by MAR, are now going to be sold. Any profit (if there is any) will therefore only be recognised in future when individual units are sold, which they reckon should be possible mostly within 2015.

(b) Some (unspecified) profit which had been advance booked on some development sites was too high, given the stage of building that they had reached, so has been reduced.

In the closing remarks, the company says it will be reviewing its procedures regarding announcements and their verification, and also that it is operating within its banking covenants, and has adequate headroom to finance its development pipeline. It also says that NAV should be "at least as high as the net asset value reported for the period ended 30 Jun 2014 being £68.3m".

Valuation - I don't think the reported profits are credible any more, so it's not really possible to value it on a PER basis. Looking at NAV, the £68.3m figure mentioned is a good start. It's nearly all tangible assets too, so £67.6m in NTAV. That is 61.3p per share in NTAV.

There's no way I would pay NTAV for the shares now, as all the figures are suspect now, in my opinion. So I'd want at least a 20% discount on the 61.3p NTAV to tempt me back in - which works out at 49p per share.

My opinion - I'm absolutely appalled by this situation. The Directors are treating a stock market listed company as if it's private. They can't repay a huge debt to the company, so they are dumping a load of their own surplus property assets into MAR to clear the debt.

Would MAR have wanted those properties, on an arms length basis? Very probably not, I would suggest, so the Directors seem to be abusing the company, and I hope shareholders give them hell at the EGM. They deserve it. Will the independent valuations really be independent? I doubt it very much. It's easy to find a friendly valuer who will smile on the properties to give them a nice fat valuation. I would only accept the independent valuations if the independent Non-Execs have appointed the valuers.

With hindsight the large related party transactions were a massive red flag. There will always be a huge conflict of interest, as is clearly the case here.

I think the reasons given for the shortfall in profit call into question how real the profits are? It looks to me like revenue recognition policies are too aggressive, and that the company is now clearly nowhere near as profitable as they were previously making out.

As such I believe management here now have zero credibility, and combined with the related party transactions, that makes this stock uninvestable. It's a private company with a listing basically. So they should either take it private again, or have a complete clear-out and bring in proper independent management with no further related party transactions.

I should add that, as soon as I got the gist of this announcement, I didn't have any hesitation whatsoever in immediately selling all my shares in this company. It wasn't a large position, but it's not something I will be revisiting, unless management are kicked out. Trouble is, they hold enough shares to be more-or-less immovable.

This is yet another example of the mess that AIM has become, I'm afraid.

On that bombshell, I will sign off and try to calm down a bit over an ice cold beer.

Wishing you a most pleasant weekend!

Regards, Paul.

(of the companies mentioned today, Paul has a long position in AVAP. A fund management company with which Paul is associated may also have positions in companies referred to here)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.