Good morning!

For anyone interested, myself and David Stredder recorded a two-part audiocast last night, recapping on companies reporting over the last few weeks, and covering our outlook and favourite share ideas for 2015. We make these purely for entertainment, so we are not recommending or giving advice. Feel free to laugh at us when our NAPS for 2015 plummet in due course! The audiocast link is here.

Although both David and I picked the following share as one of our 2015 NAPS, and it's gone up 11% this morning on a very interesting announcement (warning this stock is volatile & very speculative);

Tungsten (LON:TUNG)

Share price: 269p

No. shares: 103.5m

Market Cap: £278.4m

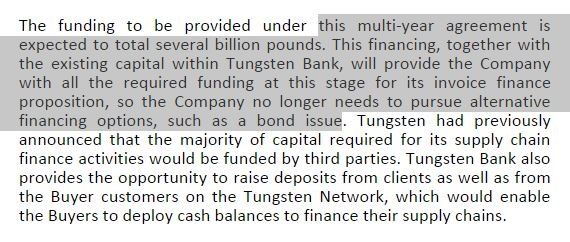

Financing update - this looks a potentially very significant annoucement. I won't regurgitate all the background to Tungsten, my previous reports here cover that. In a nutshell though, they needed to raise a substantial amount of money (think billions rather than millions) to provide the financing for their invoice discounting through e-invoicing platform, and it looks like they have been successful in raising that money.

Today's announcement of a deal (unspecified terms) with Insight Inv Mgt is described;

1. Insight is a massive asset manager, with £318bn funds under management.

2. This is a big deal ("several billion pounds"), although it's not clear whether that is referring to the cumulative total to be lent over the years, or if that is the total facility outstanding at any one time.

3. Tungsten doesn't need any additional financing at this stage.

My opinion - this looks like a big milestone. The shares are very speculative, and volatile, so come with a high risk warning. That said, I think this one has significant potential, so we'll see what happens. But be prepared for a bumpy ride - see the two year chart below!

Pure Wafer (LON:PUR)

Share price: 46.5p

No. shares: 28.3m

Market Cap: £13.2m

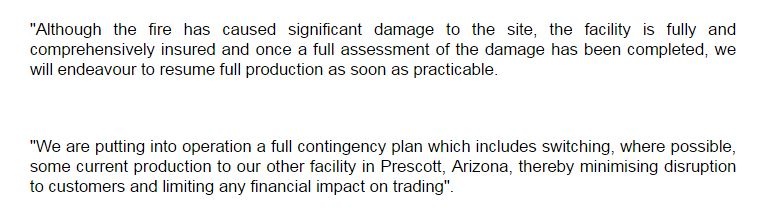

Warehouse fire - This company, based in Wales, had a disaster over the weekend - a warehouse fire. Nobody was injured thankfully, and the company has put out a statement this morning saying that they have insurance cover;

My opinion - I'm neutral on this, from an investment point of view. Some holders have obviously bailed out this morning on the bad news, hence the price being down about 19% this morning. The other side of those trades is obviously being taken by people who are taking the view that the insurance should cover the costs (assuming they also have business interruption insurance, not just cover over the physical assets), and that therefore in due course the company should be left in pretty much the same position it was in before.

Haynes Publishing (LON:HYNS)

Share price: 155p

No. shares: 15.1m

Market Cap: £23.4m

Profit warning - the company blames retailers de-stocking for a poor H1 to 30 Nov 2014, but I think it's obvious that this is a company in structural decline, just look at the Stockopedia graphs;

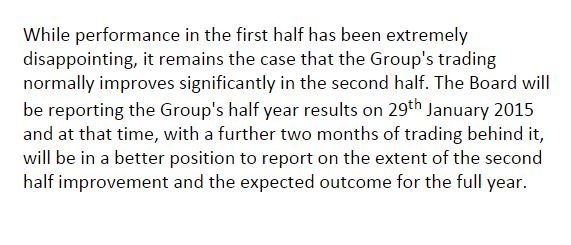

The wording in today's announcement sounds gloomy to me;

My opinion - with earnings estimates likely to come down a fair bit from 18.9 EPS, then the apparently low PER is likely to go up, and it is therefore likely to stop looking a bargain after all. It's all very well chasing the 6% dividend yield here, but is that sustainable? Probably not, in my view. I'm steering clear because it's difficult to see much long-term future for this company, or more likely a slow, gradual withering away.

Tinci Holdings (LON:TNCI)

Share price: 14p (up 225% today!)

No. shares: 53.0m

Market Cap: £7.4m

This is by far the highest riser of the day, up an astonishing 225%. The even more bizarre thing is the the news which has triggered such an explosive rise, is the company announcing its intention do de-list! You would normally expect that to crash the share price by about 50%, not make it increase. So clearly there is more to it than just a plan to de-list.

I should add, this is a Chinese company with an AIM listing, so by going further into this, we're entering a strange and (at least partly) fictitious world, where things are often not what they seem!

Proposed de-listing - in today's announcement the company gives all the usual reasons for wanting to de-list, e.g. lack of liquidity, very low share price, lack of interest from investors, costs of maintaining the listing, management time, inability to raise fresh capital, etc. All of which is perfectly valid - there is no point in something this small, on the other side of the world, being listed in London.

The de-listing will go ahead, as 80% of shareholders have agreed it already, so enough to secure the requisite 75% vote at an EGM, to authorise the EGM.

Here's the interesting bit - the major shareholder (who holds 63.3% of the company) is apparently offering to buy out other shareholders at 20p per share. Yes, 20p per share! Look at how that compares with the prevailing share price of this company over the last two years;

Therefore, the major shareholder is offering a premium of roughly 345% to last night's closing price. Why on earth would he do that?!!! He's either an extremely generous man, or there's something funny going on here!

The deal is that the major shareholder has said he will pay other shareholders 20p a share, conditional on the shares being de-listed. Moreover, he has agreed to deposit £600k (being the full required amount to buy out other shareholders) into an escrow account managed by Computershare, the registrar, prior to the EGM. The EGM will be postponed if there is any delay in that money arriving.

This will be a fascinating situation to monitor. Will he honour the deal, and pay the 20p per share to minority shareholders? Or is this a last desperate share price ramp, to lure in traders thinking there is an arbitrage to pay 14p now, and get 20p in the future, with the whole buyout then being dropped, and holders of the shares getting nothing?? Who knows!

I've been saying for a while that de-listing is the inevitable end game for small Chinese stocks on AIM. Usually that's a disaster for shareholder value, but in this case, apparently the mould has been broken with an amazingly generous exit being laid on for minority shareholders by the generous major shareholder.

Personally, I'm not convinced that this is a lovely Xmas present for shareholders, but it will be fascinating to see how things pan out. If Chinese companies leaving AIM result in 5-bagger exits, then maybe we should re-assess our attitude towards Chinese companies on AIM? Hmmmm, perhaps not. It usually pays to be a tinci-winci bit suspicious of this type of stock!

Mello Derby videos - there is a small charge for these, to cover the costs of professional production staff & editing, but they are really worth a look. The AO World one in particular is quite an eye-opener! The link is here.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in TUNG, and no short positions.

A Fund management company with which Paul is associated may hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.