Good morning! I trust everyone had a relaxing break over Christmas. Four days of the markets being closed is enough for me, so it's good to be once again getting an adrenaline fix from the markets today!

As expected, there's not much in the way of news today. However, I always like to keep my eyes peeled at this time of year for unusual price blips up or down, which can create good opportunities for things on the watch list, where I'm already fully prepared on the fundamentals, so know exactly what prices would be attractive to buy or sell at.

Year end tips in the press can also distort prices in a thin market.

Inland Homes (LON:INL)

Share price: 59.5p

No. shares: 202.8m

Market Cap: £120.7m

My observation from a stormy AGM several years ago was that management had a very high opinion of themselves at this brownfield property development company, which was not justified from the company's results at the time. However, as you would expect in a housebuilding boom, things are improving dramatically now, with a lot of good newsflow lately. There's more good news today:

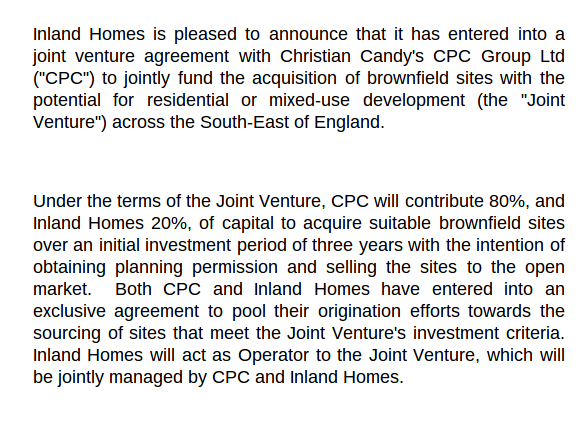

Funding JV - today's announcement is self-explanatory;

This looks an interesting deal, whereby the two companies pool their expertise, and CPC Group provide 80% of the financial firepower, to secure development sites in London. Interesting also that they are looking to sell them on, once PP has been obtained, so booking profits more quickly and presumably recycling the capital.

The Candy brothers are usually associated with ultra-high end London developments, so it will be interesting to see how this pans out, but it looks positive for Inland anyway.

Starcom (LON:STAR)

Share price: 10.5p (up 75% today)

No. shares: 84.4m

Market Cap: £8.9m

A reader has asked me to take a look at this micro cap, which has put out news today that has triggered a 75% rise in share price, about a partnership with a large Porsche dealership in Germany, for the company's tracking devices.

Whilst it sounds a great endorsement of the product, putting my sceptical hat on, the announcement contains no financial details, and also note that it is only to offer the Starcom product as an optional extra - so who knows what the take-up will be? Also there have been vehicle tracking devices around for years - I can remember an insurer insisting on me having a Tracker fitted to a new car I bought about 12 years ago!

Looking back at Starcom's most recent interim results, they're not very good - a downturn in sales moved them from profit into loss, and I don't particularly like the Balance Sheet - there is a bit of bank debt, but it's the extremely high debtors figure which worries me. Although bearing in mind the type of product, maybe customers pay a monthly fee for revenues booked up-front? (which could result in large debtors). That would need clarifying though.

Last of all, it's an overseas company (Israeli) listed on AIM, which is generally a blanket no-no for me.

So personally I won't be investing in this company, although it might make an interesting speculation for people who want to have a punt, rather than invest? The company has been profitable in the past though, but hasn't paid any divis, so one wonders how real those profits are? Note there are some intangibles capitalised on the Balance Sheet.

Having said all that, the product must be good if a big Porsche dealership approves it for being offered to customers as an optional extra, so perhaps it might be worth doing a bit more research on the product?

Chinese stocks

As regulars will know, I've had a blanket ban personally on investing in UK-Listed Chinese stocks for a long time, and that rule has served me well, and hopefully also saved readers some money too. In fact I know it has, as quite a few readers have told me that my repeated warnings on risky stocks has helped them avoid losses.

Anyway, today we wave goodbye to two China-based stocks - Bodisen Biotech Inc (an American registered company, which operates in China) is abandoning its AIM listing, but keeping a pink sheets listing in the US.

Shares in the China Food Company have also today de-listed.

It almost goes without saying that both have been disastrous investments even before the de-listing. Now they look like 100% losses. This won't be the end of it for Chinese (and other overseas stocks) de-listing from AIM. That is the only logical outcome for most of the smaller ones, in my view.

Why on earth do people get involved in these shares? Do people actually enjoy losing money or something?? You do wonder sometimes. Anyway, don't be surprised when (not if) more Chinese and other overseas stocks de-list from AIM, which in most cases will result in a 100% loss for shareholders. Although I am keeping a close eye on Tinci Holdings (LON:TNCI) to see if the company does actually follow through on its offer to buy out shareholders at a huge premium, although that is a tiny company, so it's only £600k total cost.

CityLink - Better Capital

As it's topical, here is the announcement today from Jon Moulton's Better Capital, concerning the insolvency of CityLink.

Yes it's terrible that the employees learned about losing their jobs on Xmas Day, apparently due to news of the Administration being leaked, according to Better Capital's statement today. However, in a capitalist system, inefficient, loss-making companies go bust, which benefits the more efficient competitors, who are able to hire more staff thanks to the additional business they win.

It's frightening how few Brits seem to understand the basics of how capitalism actually works, hence they are so easily misled by mischevious politicians, who will no doubt be out hand-wringing in force, blaming evil, croney capitalists for spoiling Xmas for thousands of families.

In reality it seems to me that Better Capital gave CityLink a chance to turn itself around, and took heavy losses in the process. Although it does look very bad that the taxpayer is apparently picking up the bill for the redundancy payments, whilst Better Capital is able to apparently retrieve £20m (half its original investment) due to having security over assets. Doesn't look great to ordinary people, does it? There again, without that security, they probably wouldn't have invested in the first place. Jon Moulton was on Radio 4 this morning apparently, putting their side of the story, so I shall catch up with that later on iplayer.

With news and events thin on the ground this morning, I shall sign off for the day.

See you tomorrow morning.

Regards, Paul.

(of the companies me mentioned today, Paul has a long position in INL, and no short positions.

A fund management company with which Paul is associated may hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.