Good morning!

Greece

Well, what an interesting 24 hours, what with the Greece Euro crisis finally coming to a head. I find that Twitter is the best source of breaking news, if you follow the right people. I was glued to Twitter last night, trying to assess whether the stock market here was likely to go into full-blown panic mode this morning, or not.

As it's turned out, the markets are recovering well from the overnight plunge, which makes sense really - if anything, a conclusion to the Greek crisis could be cathartic for equity markets, removing a major source of uncertainty. How it all pans out, who knows, but I've seen stats which show that not much of the Greek debt is held by the private sector, so default if/when it comes may not even have that much of an impact? Although I am a bit worried about the ripple effect of derivatives, and possible contagion to other Eurozone countries.

There again, the banks have had 7 years to plan for the inevitable Greek default, so any bank that can't cope now doesn't deserve to remain in existence anyway.

China

The plunging stock market in China doesn't concern me, as it's a largely self-contained bubble, from what I can make out. Its gyrations won't affect the valuation of my small cap investments, so I'm not concerned about this factor either. The key thing to remember with China, is that it's not capitalism. It's a command economy (or a strange hybrid anyway), so the Govt can pull levers whenever required, to achieve policy aims.

In the long run though, with company and Bank balance sheets filling up with bad debts, there will have to be a gigantic flushing out of the system. When that will happen, who knows? It may not even be in my lifetime, so why worry about it?

ShareSoc Masterclass/Garden Party

Sounds like this event, hosted by Killiks, in their wonderful Mayfair office, will be excellent. It's this week - on Thu 2 July. Full details are here. There is a special offer for Stockopedia readers - click here.

The panelists for the discussion part of the evening are star small caps investors - David Stredder, Lord Lee, and Leon Boros (all three are self-made millionaires from small cap investing), plus Mick Gilligan (Partner and Head of Fund Research at Killik).

My view is that the best people to learn from (about any topic), are those who have a proven track record of success - and this panel is positively groaning with it - as you may well be at their jokes too (David & Lord Lee especially!)

Anyway, on to the day's results & trading updates, although I wonder if there's any point - is anyone interested today?!

It's quite interesting to watch the prices & trades of stocks I either own or follow, as that can be very revealing on a day like today. I can see how many nervous holders there are in particular stocks, and also at what price buyers steam in and find the price too attractive to turn down, as on a day when there's panic around that level could be a short term floor.

With one of my holdings, I was even able to sell some on the opening bell, and then buy them back 7% cheaper a few minutes later - very pleasing - especially as they're half way back up again now. So a market wobble isn't necessarily such a bad thing.

Redde (LON:REDD)

Share price: 136p (up 5.6% today)

No. shares: 295.1m

Market Cap: £401.3m

Q4 & full year trading update - this is a legal claims group, which seems to go from strength to strength. There's no dodgy accounting here either, unlike some competitors. Shareholders will no doubt be very pleased with today's update, the latest in a long line of good news from this company:

There are also updates on cash - reported as £64.9m at 31 May 2015, or 22p per share - fairly material at just over 16% of the market cap.

Net cash is also reported at £38.8m (net of fleet financing), although I would say this fleet funding debt can safely be ignored, as it is asset-backed, with assets that could be readily realised at book value if necessary - i.e. its fleet of hire cars.

Autofocus - this is a long-running legal dispute. It sounds as if progress is being made, with "a number of negotiated settlements have been achieved", but no financial details are given, probably due to confidentiality agreements I would imagine. Although the amount will be revealed in due course, as it will be shown as exceptional income.

Dividends - this company has been a cash machine for shareholders in recent years, churning out divis, which is all the more impressive considering the share price has gone up a lot (the company was almost bust a few years ago, but has undergone a remarkable turnaround since). So the total shareholder return has been remarkable.

A 1p special divi is announced today, on top of an indicated 4p or more final divi. So the total divis for the year will be at least 9p (including the 1p special divi announced today). Not bad going!

My opinion - the price is looking a bit full now, in my view. If you assume they might do say 8p EPS this year (current broker forecast is 7.1p, so I've allowed for several upgrades, given that has been the pattern in recent years), then that puts them on a PER of 17, which I think is rather pricey for this type of business (legal services), which is a controversial sector, where companies and investors frequently slip up.

I'm not convinced there's much more upside left in these shares at 136p, for the time being, but who knows, they've surprised on the upside many times before! At some point it makes sense to top-slice I think, maybe we're at or near that point now? That's up to individual investors to decide, I'm only giving my opinion, not any recommendation, as always.

Quindell (LON:QPP)

Shares suspended still

Update - there's an update today from Quindell, whose shares were suspended last week, but today's update doesn't really say much. It says that work on the audit for 2014 is "in its final stages", but won't be completed by the deadline for filing its accounts of 30 Jun 2015.

I thought that was a given, as I thought it was the main reason the shares were suspended? There's also the FCA investigation into the company's past alleged misdemeanors to think about.

The company confirms that its shares will remain suspended until the publication of the 2014 accounts, as expected.

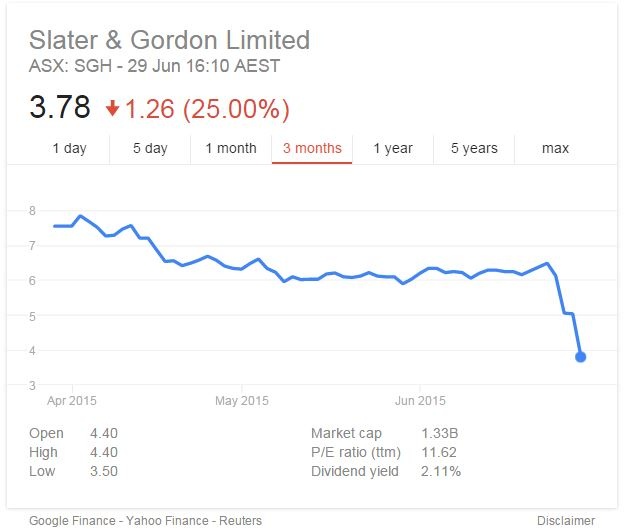

Slater & Gordon

This is the Australian & international firm of lawyers, which perplexed the market by paying a remarkably rich price for Quindell's legal services business. Anyway, the deal looks to have been a disaster for S&G - their share price has more than halved from its peak three months ago:

This is scarcely believable, but revelations that S&G has itself been incorrectly reporting its figures have emerged! I don't know how serious the accounting "errors" are, but this article gives more detail.

Dear oh dear! Ambulance-chasing lawyers, eh?! Such a reliable and trustworthy bunch, aren't they!

Progility (LON:PGY)

Share price: 4.0p (down 43% today)

No. shares: 199.7m

Market Cap: £8.0m

Profit warning - I've not looked at this one before, and probably won't do again, so am only writing this so that I have a record of the details to refer back to in future.

Today's update says that the last few months of their financial year ending 30 Jun 2015 has been disappointing, with EBITDA after central costs "markedly below expectations". Actions are being taken to address the underlying business performance, it says.

This company's main problem is a terrible balance sheet. Basically its Chairman is propping up the company with loans, charging interest at 12%. In my assessment, the company would have gone bust without this support.

The last reported balance sheet has net assets of £8.1m, but take off intangible assets, and that turns negative at -£11.7m. The current ratio looks quite weak at 0.94, but the biggest issue is the £13.1m of loans & overdrafts in long term creditors. These creditors effectively control the business, so equity holders are entirely at their mercy. However, since the Chairman owns 64.75% of the equity, then he probably wants to preserve the value of the equity.

I think a debt for equity swap is the only solution here, which would make the free float an even smaller percentage, and might be on terms that are unpleasant for minority shareholders. Given the inappropriate capital structure, and the poor current trading, I'll put this one on my Bargepole List, to remind myself that it's a can of worms as currently structured.

Am popping out for lunch now. Will try to write a bit more later. Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.