Good morning!

I'm away from home today, with a very poor internet connection, so am hoping I'll be able to get through this article without any more technical problems!

Netcall (LON:NET)

Share price: 51.5p (down6.4% today)

No. shares: 137.0m

Market cap: £70.6m

Takeover deal is off - an unusual announcement today from Eckoh (LON:ECK) stating that a major Netcall shareholder has been reluctant to support the deal which had been agreed between the companies' management:

This is certainly embarrassing for both Boards - usually when a recommended deal is announced, the deal would go through, with major shareholders having been taken inside, and agreeing it beforehand.

Netcall's biggest shareholder is Livingbridge VC LLP, who hold 17.9%, so presumably it must have been them who scuppered the deal? The next largest shareholder is Gartmore, with 10.8%, then Investec with 8.7%.

The problem with this mooted deal was that it was mainly in shares - 63.94p for each Netcall share, of which only 13p was in cash. The balance was in Eckoh shares (based on them being priced at 40.75p), but in my view Eckoh shares are significantly over-valued, so personally I wouldn't want to swap shares in something reasonably priced, and get paid in shares that are over-priced! Perhaps that's why the deal floundered?

From the point of view of Netcall shareholders, at least they now have the comfort (and potential future upside) of knowing that a third party is interested in buying their company. A better deal might come along in the future perhaps?

Ubisense (LON:UBI)

Share price: 96p (-13.1%)

No. shares: 36.3m

Market cap: £34.8m

Profit warning - yes, another one! It last warned on profit on 30 Apr 2015, and stated that it needed to raise more money. Then on 8 May 2015 a Placing at 90p was announced, to raise £10m (pre-expenses). Then on 4 Jun 2015 new banking facilities were agreed with HSBC.

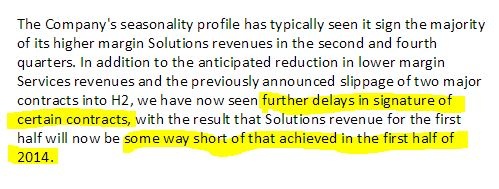

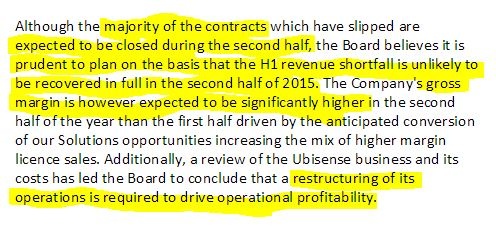

Today it says there have been further contract delays:

More detail is given:

So a bit of a mixed bag. Without guidance on how these various points will combine to affect profits, it's difficult to draw much of a conclusion. So it would be a case of trying to get hold of updated broker notes, since they will have been given a steer by the company.

My opinion - I've always been sceptical about this company. Nice products, but they don't seem to be gaining traction on sales/profit growth as yet.

At least the company has sorted its cash shortfall (for the time being), and seems to be taking action to restructure, so purely as a punt, this might be worth considering possibly? It's the sort of thing that will either continue disappointing, or might shoot up on improved trading, who knows?

These days I try to avoid buying things on hope alone, as it nearly always goes wrong.

Stadium (LON:SDM)

Share price: 112.2p (up 2% today)

No. shares: 31.1m

Market cap: £34.9m

Trading update - this all sounds fairly upbeat:

Valuation - it looks reasonable, on a fwd PER of only 10.3, but bear in mind that the balance sheet isn't great now, and the pension deficit recovery payments are material - see my article from 17 Apr 2015 for more details. So a lowish PER is to be expected, due to these other factors.

My opinion - it looks a nice little company, and seems to be trading well. The Chinese factory implementation introduces a risk factor. Overall, I think this share is worth doing a bit more research on.

Provexis (LON:PXS)

Placing via Primary Bid - just a quick comment to flag up an interesting announcement that the new Primary Bid platform - which allows private investors to participate in small Placings - has successfully raised £280k for this company, at a 22.4% discount.

I hope this platform succeeds, as it looks a cost-effective way for small companies to raise modest amounts of fresh share capital. The costs of this raise were only £12,600, or 4.5%, so it's clearly an efficient way to top up the coffers for small and micro caps.

No doubt the vested interests in the City don't want to see their fees gravy train de-railed though! Personally I am supportive of anything that gives PIs a fairer deal, so Primary Bid gets a thumbs up from me (just to be clear, I have no connection whatsoever with PB).

ECO Animal Health (LON:EAH)

Share price: 305p (up 1.8% today)

No. shares: 63.2m

Market cap: £192.8m

Results y/e 31 Mar 2015 - the headline bullet points look really good - all key metrics up significantly, e.g. sales up 22%, pre-tax profit up 38% to £5.1m.

Diluted EPS is the best measure of performance here in my view, and that rose from 4.3p last year to 6.79p this year, an increase of nearly 58%. Although note the rating is very high, at a PER of 44.9. However, if that rate of growth continues, then the company would grow into the valuation quickly, so I don't rule out high PER stocks where they are on a strong & sustainable growth path.

We should of course be looking at what the PER would be for this year & next year. Broker consensus is for 12.3p EPS this year, so that's a PER of 24.8, which is high, but doesn't seem outrageous for a fairly high margin growth company.

I flagged up this stock as potentially interesting in my report of 28 Jul 2014, but didn't get round to doing any more detailed research, which is a pity as the shares have risen 76% since then. Hopefully some readers picked up on the idea, that's the purpose of these reports after all, to hopefully give some pointers for stocks that might be worth looking into in more detail.

From what I can tell, growth seems to be organic too, since the Goodwill line on the balance sheet has not changed in the last two years. As I mentioned on 28 Jul 2014, investors need to be aware that a large element of costs are capitalised into intangibles here. So the focus on EBITDA in the narrative should be ignored, in my view - since it over-states performance by ignoring capitalised costs and the amortisation of historic costs.

Almost £5.3m of development costs were capitalised into development costs on the balance sheet in the year. That's fine, as a drug company will have substantial development costs, but it's important to bear in mind when valuing the company.

Balance sheet - overall this remains very strong, and has £17.7m net cash.

Outlook - upbeat, "The new financial year has started well with revenue maintaining momentum. I look forward with confidence to ECO delivering another impressive performance..."

My opinion - overall, although the shares look expensive, this looks a credible growth company, which is decently profitable, and growing well.

That's everything which has caught my eye today, so I'll sign off for the day & the week. Have a great weekend, and see you back here on Monday morning!

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions. A fund management company with which Paul is associated may hold positions in companies mentioned.

NB. These reports are Paul's personal opinions only. They should never be misconstrued as being recommendations or financial advice)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.