Good morning!

A couple of things to note. Firstly, the market crash in China is continuing apace - I'm not sure which Index is the main one, but currently the China 300 Index is at 3,660, which is down c.32% from the peak less than a month ago. It doesn't seem to be having any impact on our markets though, thankfully.

The second striking thing was the big drop in the price of oil yesterday. Looking at the chart of US Light Crude, it was trading in a range of $58-62 in May-Jun 2015, but suddenly lurched down to $53.18 over the last week. I don't know why, just the forces of supply and demand I suppose. It's making me wonder whether I should defer any further attempts at bargain hunting in the oil, and oil services sectors?

Right, quite a few interesting trading updates this morning, so let's get cracking!

Churchill China (LON:CHH)

Share price: 554p (price unchanged today)

No. shares: 11.0m

Market cap: £60.9m

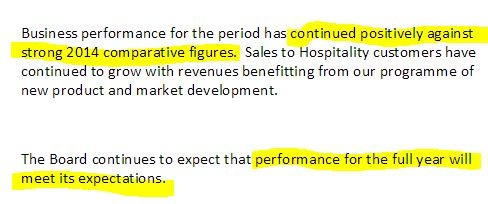

Trading update - today's update is reassuring:

Valuation - I last looked at this company at 595p per share in Jan 2015, and concluded that it was rather too pricey. It's drifted down about 7% in share price since then, combined with broker estimates having edged up, so a double positive there.

The fwd PER is now 16.2, and the dividend yield is 3.2%.

Combined with a strong balance sheet, I think the shares look fairly priced.

My opinion - I like this company, its sound finances, and the valuation has come down from a touch expensive, to reasonable now, in my view.

There seem to be new restaurants and cafes popping up all over the place (in the South anyway), so I expect CHH will continue to enjoy buoyant trading for some time to come. Although it's important to remember that demand is cyclical, so profits are likely to drop when the next recession comes along.

I wonder if they are likely to be impacted by the strength of sterling? I've just checked the last Annual Report (page 57), and 60% of turnover is UK, with Europe being the next largest region, at 23%, N.America 8%, and RoW 9%. No mention is made about currency in today's update, so presumably the company must have either hedged, or absorbed the impact itself.

Somero Enterprises Inc (LON:SOM)

Share price: 146.5p (price unchanged today)

No. shares: 56.1m

Market cap: £82.8m

(at the time of writing, I hold shares in this company)

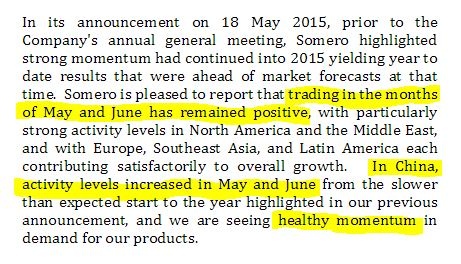

Trading update - this maker of laser-guided concrete screeding machines reported positively on trading at its AGM on 18 May 2015, and says today that it is "slightly above current market expectations".

More detail is given, and I'm particularly reassured that demand in China has picked up, as that was a worry previously:

Valuation - the shares still look cheap to me, on a PER of about 11, with a strong balance sheet (containing net cash), and a StockRank of 98. There's a 2.7% divi yield too. Note the very high quality scores on Stockopedia too.

Set against that is the high cyclicality of the business historically - so demand considerably reduced in the last recession. There again, that's true of many cyclical industries, and arguably the 2008 financial crisis was such an extreme event, that future recessions may not be quite so bad?

My opinion - overall I really like this share, and hold it personally.

To my mind it's the ideal scenario really, of a high quality business, with sound finances, at a reasonable (cheap, even) valuation. So it's perplexing that the shares have slipped back down to level for the day, after an inital 5p mark-up. Quite why anyone would sell at this valuation, is beyond me! But that's what makes a market I suppose - buyers and sellers with different perspectives.

Globo (LON:GBO)

Share price: 46.3p (up 3% today)

No. shares: 373.7m

Market cap: £173.0m

Situation in Greece - Globo tries to reassure the faithful that the crisis in Greece is not really affecting it very much. Key points are;

- Greek Euro exit would lower their cost base

- in 2014 only 12% of Group revenue came from Greece

- All receivables relating to 2014 Greek sales have been received

- 2015 Greek turnover will only be 6-7% of the group total

- 42% of total group headcount are based in Athens

- Computer systems are cloud-based, and they have backup power generators, and satellite connections

- Cash reserves are outside of Greece, with only E100k in Greek bank accounts

- Capital controls should cause no interrruption to their financing, as their purpose is mainly to control/stop the export of currency from Greece

- They reassure that the Greek 49% Associate is trading alright, and paying the instalments due to the group on time

- The situation in Greece "has not arisen overnight", hence they have had time to prepare

My opinion - overall, the above sounds reassuring. However, the bigger question is whether Globo's accounts can be relied upon - in particular, where is the cash, and why do they borrow extensively (incurring E4m interest cost last year) whilst simultaneously holding greater cash balances?

I remain of the view that the accounts for this company don't look right at all, and explained specifically why here.

Communisis (LON:CMS)

Share price: 49p

No. shares: 207.5m

Market cap: £101.7m

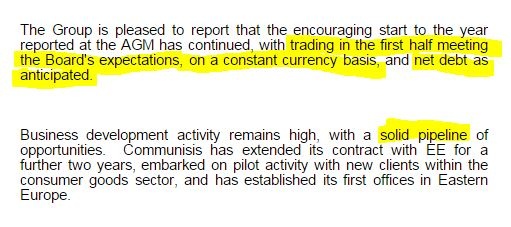

Trading update - this direct marketing group (junk mail, presumably?!) updates positively today;

That sounds fine, but note the "on a constant currency basis" caveat - which possibly implies that they could be below expectations in sterling terms? That depends whether or not expectations factored in adverse currency movements, which it sounds like possibly they didn't?

"Net debt as anticipated" - fair enough, but it would have made more sense to actually give the figure! They're probably coy about this because the company has a ropey balance sheet, so it's easier to gloss over the negatives I suppose.

Outlook comments sound encouraging.

Valuation - looks tempting at first sight, with a PER of only 7.4, and a good dividend yield of 4.8%. However...

Balance sheet - this is where, for me, the investing case falls apart. Checking back to the last reported balance sheet, on 31 Dec 2014, note the following;

1. Net tangible assets are negative, at -£59.8m. So effectively the balance sheet has a big hole in it, caused by bank debt, and a pension deficit.

2. Bank debt - gross bank debt was £60.4m on 31 Dec 2014, which looks a hefty level of borrowings for a company that made an adjusted operating profit of £16.0m last year. On the year end date the company also held £24.5m of cash, so net debt is a more reasonable £35.9m. However, I like to focus on gross debt, as the cash figure is usually window-dressed at most companies in my experience.

The £2.4m interest cost for bank debt implies a fairly hefty average balance, of say £48m if we guesstimate 5% interest cost.

Overall then bank debt looks a tad too high to me.

3. Pension deficit - I'm more relaxed about pension deficits than bank debt, but it's still a liability, and sits on the balance sheet at a hefty £39.1m.

My opinion - the reason Communisis looks cheap is because it has a weak balance sheet. I feel they should properly tackle this issue by cancelling the dividends for say 3-5 years, to put the company on a more secure financial footing. However that's a call for management and shareholders.

Connect (LON:CNCT)

Share price: 144.5p (up 0.3% today)

No. shares: 243.7m

Market cap: £352.1m

Trading update - there's a good update from this group today, with the key part saying that "overall performance marginally ahead of management expectations", covering 44 weeks, so they should be more-or-less home and dry for the full year.

Details on divisional performance are also given, which I haven't looked at. The statement concludes that "There has been no change in the underlying financial condition of the Group".

This is a similar situation to Communisis above, in that Connect looks cheap on a low PER of 7.7, and a fantastic dividend yield of 6.5%. However, once you dig into the balance sheet, it's far from rosy, in fact it's bad.

Balance sheet - as usual my main three tests are as follows:

1. Net tangible assets should be positive - FAIL. Once you write off intangible assets of £172.9m, net assets of £2.8m becomes net tangible assets of -£170.1m - so again, a company with a massive hole in its balance sheet.

2. The current ratio should be at least 1.2 - FAIL. I'ts only 0.67 here, which is very weak. Trade payables looks very stretched to me, so they're probably getting money up-front from customers (which shows up as deferred income within creditors), and/or stretching their trade creditors.

3. Bank debt should be reasonable - this is an area of personal judgment, but for me the bank debt looks excessive, and had risen to £157.9m at Feb 2015, due to £53.0m spent on the acquisition of Tuffnells.

However, as the company points out, its net debt was 1.94x EBITDA, which is well within their main bank covenant of 2.75x. It also says that it is "committed to continue to paydown this debt towards our historic leverage ratio".

My opinion - the bull case here is that the group is a cash cow, which can handle the high level of debt, and still pay a bumper dividend yield. Personally I don't agree with that. It's all very well quoting EBITDA, but when you take into account the reality of cashflow, where tax, interest, and capex have to be funded, I don't see any evidence that this company can afford to pay such large dividends as well as reduce debt.

So one could argue that the big divis are being funded, at least in part, by bank debt, which isn't a good idea in the long run. So I suspect there might come a point where the divi here needs to be scaled down to a more sustainable level of say 2-3%.

Bottom line, it's cheap on a PER basis for a reason - the core activities are arguably in structural decline (newspapers, books - although they are supplementing this with other distribution activities), and the balance sheet is weak. Overall then, it's not for me.

Solid State (LON:SOLI)

Share price: 855p (down 4.7% today)

No. shares: 8.3m

Market cap: £71.0m

Results y/e 31 Mar 2015 - shares of this niche electronics maker & distributor have had a terrific run, more than tripling in price over the last two years, driven at least in part by a large order from the UK Govt for offender electronic tags. So the big question here is over sustainability of earnings, and whether the group is too reliant on one product/customer?

Looking first at the numbers reported today, turnover is up 14% to £36.6m, profit before tax is up 40% to £3.0m, and basic EPS is up 38% to 34.9p. So my immediate reaction is that the shares look expensive - that's a PER of 24.5 - very high for a business that has historically been quite modestly valued, on a PER of about half that.

Although Stockopedia shows broker consensus at 31.6p EPS for the year ending 31 Mar 2015, so today's results seem to be ahead of forecast by about 10%, so it's surprising to see the share price actually down today.

The order book is up, at £19.4m (vs £15.1m a year earlier).

Balance sheet - this looks OK to me, with a solid working capital position (current ratio of 1.61), positive net tangible assets (of £7.0m), and net debt at a reasonable level of £2.5m.

Valuation - I've mentioned above that the historic PER looks high, but it's really all about the future when valuing companies of course. The current year forecasts show a big increase in turnover and profits, so EPS is forecast to rise to 55.5p this year (ending 31 Mar 2016), which would bring the PER down to a much more reasonable 15.4.

That's fine, but a PER is only relevant if that level of profitability can be sustained.

My opinion - sustainability of profits is the only issue that really matters here. There's interesting commentary with the results, suggesting that there are new products in development with potential to further boost sales and profits perhaps.

That's as far as I can go with analysing this share - to form an opinion one would really need to dig into the detail about the company's products, competitive position, potential for new products, and repeatability of big orders (like the MoJ tagging contract). If this is the start of a period of big orders then the shares could be cheap. However, if it's a one-off bumper period which won't last, then the shares could be expensive.

I don't have a view on this, as I've not done enough research on the company to form a considered opinion.

McBride (LON:MCB)

Share price: 103p (up 1% today)

No. shares: 182.2m

Market cap: £187.7m

Trading update - this relates to the year ended 30 Jun 2015 - the company says that "adjusted operating profit for the full year will be in line with expectations".

Germany saw "strong growth", offset by lower revenues in other key markets.

Cost-cutting seems to be of key importance here, with £5m savings achieved for y/e 30 Jun 2015, and a further £7m savings targeted for 2016.

Broker expectations are for 7.84p, so the PER is 13.1, dropping to 10.4 times forecast EPS for the current year. That sounds a sensible rating for a very low margin business which is struggling to deliver growth.

Balance sheet - unfortunately, this is yet another company with a weak, over-geared balance sheet, that also has a pension deficit. So the 5p divis (yielding 4.9%) don't look safe to me. Again, as with other companies reporting today, McBride should really be getting their debt down, rather than stretching the balance sheet to reward shareholders, in my opinion.

The trouble is, if companies stretch their balance sheets in the good times, then they have nothing to fall back on when recessions hit.

My opinion - the shares here have had a good run, but don't appeal to me at the current valuation.

I'll leave it there for today. See you tomorrow!

Regards, Paul.

(of the companies mentioned today, Paul has a long position in SOM, and no short positions. A fund management company with which Paul is associated may hold positions in companies mentioned.

NB. There reports are Paul's opinions only, and are NEVER financial advice, nor recommendations. We encourage readers to do your own research, and make your own decisions).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.