Building engineering firm Alumasc has triple-bagged since hitting a low of 62p in 2012. A tighter focus on sustainable and high-spec products appears to have served the group well.

As with housebuilders, this gives rise to an obvious question. Is it too late to buy into such a cyclical stock?

No -- or at least not according to Stockopedia’s computers, which currently rank the firm very highly. Alumasc is one of only a dozen UK firms with a StockRank of 99. The stock also qualifies for five Stockopedia’s Guru Screens and was one of the qualifying stocks for Stockopedia founder Ed Croft’s 2016 NAPS portfolio.

In this article I’ll explain why Alumasc scores so highly. I’ll also offer my opinion on whether the shares have further upside potential, and highlight some of my concerns.

What does Alumasc do?

Alumasc has a number of operating businesses in two main areas: energy management and water management.

Energy management really means solar shading, roofing and walling, while water management means drainage, guttering and related products. One of the group’s flagship businesses is Levolux. This firm builds solar shading and screening for large commercial and industrial buildings. A recent £3m contract win for Levolux in the USA will see Alumasc design and install a “custom screening solution” for a new gas-fired power plant.

These products may not be that sexy, but they do seem increasingly relevant to modern construction, and likely to remain so.

(Alumasc does also have a die-casting business, but this accounted for less than 10% of revenue last year and is something of a legacy operation, so I’ll ignore it.)

What about the value?

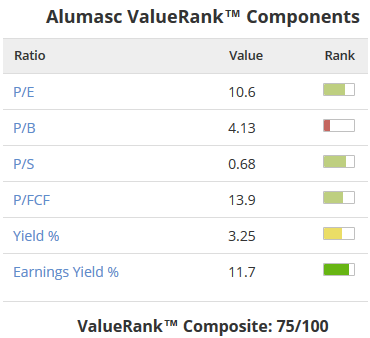

According to Stockopedia, value is Alumasc’s weakest point. The stock’s ValueRank is just 75.

One reason for this is Alumasc’s P/B of 4.1, which seems very high for a manufacturing firm. On closer inspection, this appears to me to be a warning flag. The reason the P/B is so high is because Alumasc’s book value per share has fallen from 88.5p in 2011 to 44.1p last year, despite the share count remaining unchanged.

Although some of this decline is the due to Alumasc selling various non-core business, there is a second reason. The group’s pension deficit has risen from £2.8m to £20.9m since 2011, reducing net asset value.

Alumasc’s large final salary pension scheme appears to…