I wrote last week about Chinese, Indian and Korean vessels making it through the Strait of Hormuz.

Yesterday, two more supertankers made it through the Strait: one from Singapore and one from Greece. A few Iranian oil tankers also passed through without incident.

According to Bloomberg, tankers are travelling together in small groups - safety in numbers, I guess. They are crossing through a diplomatic grey area, without a US escort but likely having some sort of agreement with Iran.

It’s possible that other vessels have also made it through, but have not been detected due to signal interference.

I find this one of the most intriguing elements of the conflict: commercial vessels floating through waters where jet and drone attacks are also occasionally taking place, and (allegedly) where mines are being placed!

The best-case scenario is that a deal is announced in the next few days. I’ve trained myself to be an optimist - it feels necessary as an equity investor - so I’m going to hope this happens very soon, that commodity prices go back to normal, and our focus can then move on to something else. Negotiations between the Trump administration and Tehran continue.

Overnight market movements:

The FTSE is set to open down 0.1% at 10,490

S&P 500 is unchanged at 7,525

Brent crude (July delivery) is down 2% at $97.90

Gold is unchanged at $4,530

Bitcoin is down 0.5% at $75,700

Today's Agenda is complete. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

AstraZeneca (LON:AZN) (£217bn | SR75) | FDA has extended PDUFA date to review additional data requested to support the NDA for camizestrant in combination with a cyclin-dependent kinase (CDK) 4/6 inhibitor for the treatment of patients with HR-positive, HER2-negative advanced breast cancer whose tumours have an emergent ESR1 mutation. | ||

Scottish Mortgage Investment Trust (LON:SMT) (£16.8bn | SR N/A) | NAV +27.4% for the year to 31 March 2026. “A notable contributor … was SpaceX, where continued strong operational execution has led to a significant upward revaluation, increasing its position as the Company's largest holding by some margin.” SpaceX is reported as 19.3% of the portfolio at 31 March. | ||

HICL Infrastructure (LON:HICL) (£2.4bn | SR86) | NAV per share up 4.6% to 160.2p, NAV Total Return of 10.3%. 12.2% portfolio return, “significantly ahead of expectations”. Dividend of 8.35p with cash cover, FY27 target reiterated at 8.50p, with 8.65p for FY28. | ||

Greencore (LON:GNC) (£1.9bn | SR80) | “… strong half year results for the new Greencore, having acquired Bakkavor in mid-January.” Pro Forma revenue +3.2%, pro forma adj op profit +15.3% to £73.3m. Outlook: expect to deliver FY26 adj operating profit in line with current expectations. | ||

Bodycote (LON:BOY) (£1.43bn | SR84) | Year-to-date revenue +1.9%, with core revenue +9% and strong growth in Aerospace & Defence and Industrial Gas Turbines. FY outlook maintained, expect core revenue growth to moderate in H2. | ||

Pets at Home (LON:PETS) (£830m | SR87) | Revenue -0.8%, pre-tax profit -28.3% to £86.5m. Adj EPS -29.7% to 14.8p. Dividend of 7.4p plus further £50m buyback. FY27 outlook: “we are comfortable with consensus expectations” for adj pre-tax profit of £98m. | ||

Cohort (LON:CHRT) (£580m | SR29) | FY26 revenue +12% to £303m, adj operating profit +31% to c.£36m, ahead of market expectations. Closing order book of c.£620m (FY25: £615m, includes 80% cover for FY27 revenue forecasts: “confidence in a strong 2026/27”. | AMBER/GREEN ↑ (Graham)

We’ve been a little cautious on this one, worried about the H2 weighting it needed to hit full-year forecasts and the high valuation. We were wrong on the first count, although I think there is still an argument to be made that the valuation here is punchy. The ValueRank is only 19, and Stockopedia categorises it as a Falling Star. But when the facts change we should change our minds, and it turns out that there was nothing to fear about the H2 weighting - the company has more than fully delivered on what was expected in H2. So I’ll nudge us up to AMBER/GREEN today. | |

Hollywood Bowl (LON:BOWL) (£436m | SR66) | Revenue +9.5%, UK LFL +1.3%, Canada LFL -3.2%. Adj pre-tax profit +8.1% to £32.1m, adj EPS +11.3% to 14.5p. Outlook: confident in delivering on FY26 expectations. | ||

B.P. Marsh & Partners (LON:BPM) (£243m | SR90) | Final Results for the year to 31 Jan 26 & Directorate Change | NAV +10.3% to £360.2m (959.8pps), total shareholder return of £41.7m (12.8%). Brian Marsh moves from chairman to “Founder and Life President”. New chair appointed. | GREEN = (Graham)

I’m very glad to be a shareholder here again, but there are a few details worth ironing out. I estimate current NAV as 937.5p, implying a discount to NAV today of 26%. I’d also like to reiterate that the diversification of the portfolio is limited, due to some large positions - the level of concentration of BPM’s portfolio is equivalent to holding 7 or 8 different positions. Just something to be aware of, in case you are treating this like some sort of mutual fund - it’s more concentrated than that. |

Sovereign Metals (LON:SVML) (£218m | SR19) | Monazite concentrate containing the most critical and highly valuable heavy rare earth elements Dysprosium (Dy), Terbium (Tb) and Yttrium recovered from four planned pits in the Kasiya DFS mine plan, including pits scheduled for Year 1 production. | ||

Zotefoams (LON:ZTF) (£198m | SR76) | Year-to-date revenue +26% to £64.1m, led by EMEA. Footwear growth moderated but Transport & Smart Technologies continued to grow. 2026 outlook: full-year expectations remain unchanged. | AMBER/GREEN = (Roland) I am tempted to upgrade to be fully positive on Zotefoams, as I think the business is improving and the forward P/E of 10 looks undemanding. However, the group’s continued heavy exposure to Nike (where earnings forecasts were cut recently) and last year’s changes to segmental reporting mean it’s a little hard to be sure about the profitability and scale of the group’s other main division. While it’s possible that I’m being too cautious, I’m going to mirror the falling StockRank and leave my moderately positive view unchanged following today’s in-line update. | |

Afentra (LON:AET) (£168m | SR65) | Afentra has been awarded a 35% operated interest in KON4 alongside Angolan partners. The signing of the contract is expected at a later date. KON4 is situated in a historically productive area, including the Quenguela Norte field where production peaked at 12,000 bopd before being shut in in 1999. | ||

Aptitude Software (LON:APTD) (£119m | SR38) | Two new Fynapse enterprise wins so far in FY26. Rationalising wider product lines. Strategic review remains ongoing with a range of options under consideration. | ||

Andrada Mining (LON:ATM) (£86m | SR22) | Approval for conditional funding of NAD98 million (c. £4.4 million) Bank Windhoek and the Development Bank of Namibia. The expanded diamond drilling programme at its Lithium Ridge project has now been completed. Assay results confirm extensive, high-grade lithium mineralisation, up to 3.02% Li₂O over 5m. | ||

Arrow Exploration (LON:AXL) (£72m | SR69) | Average corporate production of 4,715 boe/d (Q1 2025: 4,085 boe/d). Adjusted EBITDA up 22% ($14.1 million). Net income of $5.2 million. Cash $24m. "The focus for the remainder of 2026 will be to drill additional wells at the Icaco pad, drilling development wells on the Alberta Llanos and Carrizales Norte pads and numerous well recompletions to improve productivity in our currently most prolific fields." | ||

Watkin Jones (LON:WJG) (£59m | SR53) | Revenue down 22% to £100.2m. PBT £0.0m (HY 2025: £0.2m). Adjusted net cash £61.3m. “We have achieved a resilient performance in the first half… While market conditions remain challenging and continue to impact the pace of recovery, the long-term fundamentals of our end markets remain attractive…” | ||

Hardide (LON:HDD) (£40m | SR59) | Orders received from its large North American energy customer to cover the remainder of FY Sep 2026. Value £2.4m is greater than the Board's previous expectations for this current financial year. This will have the effect of materially improving revenue and overall financial performance expectations for FY26. “We expect these orders to continue…. developing a mutually beneficial schedule for orders and deliveries which will underpin FY27.” | ||

Abingdon Health (LON:ABDX) (£30m | SR24) | Abingdon Health USA, Inc. has been certified as eligible to earn up to US$370,000 in performance-based Wisconsin tax credits over a three-year period. | ||

Kendrick Resources (LON:KEN) (£31m | SR21) | Completes internal review and analysis of historic and current work, resulting in targets consistent with expectations for the Company's flagship rare earth projects at Teufelskuppe and Kieshöhe in SW Namibia. These projects are subject of a 70% earn-in interest by the Company. | ||

ImmuPharma (LON:IMM) (£28m | SR4) | Loss for the period £1.8m (2024: £2.5m). Cash £1.4m at Dec 2025. Subsequently raised £6.5m. CEO: "ImmuPharma is entering a pivotal phase, focused on securing a commercial partnership for P140 in 2026 while continuing to develop its broader portfolio, with a key focus on fast tracking Kapiglucgaon over the next two years.” | ||

Europa Oil & Gas (Holdings) (LON:EOG) (£21m | SR19) | 17 months: revenue £3.9m (12 months to July 2024: £3.6m). Pre-tax loss £2.7m. Cash balance £0.3m. Subsequently raised £4.1m. Outlook: well placed to capitalise on momentum, with “EG-08 Farm-out Agreement and anticipated drilling of Barracuda later in the year in particular providing further certainty for the Company's short-term outlook.” | ||

Tekcapital (LON:TEK) (£16m | SR55) | Loss after tax $17.1m caused by the unrealised depreciation of its portfolio. Net assets $55.1m (2024: $70.1m). NAV per share $0.23. | ||

RTC (LON:RTC) (£15m | SR99) | Q2: high fuel costs have impacted margins in Rail and Energy. Materially lower demand for temporary labour. Permanent vacancies at lowest point since 2021, and resignation rate at lowest level since Covid. | ||

Nanoco (LON:NANO) (£13m | SR51) | Proposed cancellation in order to further reduce operating costs. Annual savings of £0.7m. Cash balance £10.1m as at 19th May 2026. Cost savings will extend the Group's cash runway, with a view to being break even in the medium term. | ||

Jangada Mines (LON:JAN) (£12m | SR15) | Ongoing exploration at the Molly Gold Project in Brazil. Molly 1: High-Grade Gold Confirmed, drill holes 3A and 3B intercept significant gold, silver and copper mineralisation. Molly 2: Discovery Confirmed: Maiden Discovery Hole 7A demonstrates previously undrilled deposit related to the Molly 1 system. |

Graham's Section

B.P. Marsh & Partners (LON:BPM)

Up 2% at 688.55p (£248m) - Final Results for the Year to 31 January 2026 - Graham - GREEN =

(At the time of writing, Graham has a long position in BPM.)

I’ve been consistently positive on this insurance investor, and I don’t think today’s results are going to change my stance. So let’s review it quickly.

Key points:

NAV increases 10% to £360m

Total shareholder return (including £8m of dividends) of 12.8%

NAV per share 1,009.9p, or 959.8p fully diluted.

The equity portfolio generated a return of 21.4%

Following £8m of dividends paid in FY January 2026, BPM is planning to pay £13m in FY January 2027 and £7m in FY January 2028. This follows some very successful investments and disposals, which gave rise to an unnecessarily large cash balance. The cash balance is currently £29.6m.

Board changes: Founder and Life President Brian Marsh OBE stepped down from the Board yesterday, after 25 years as Executive Chairman and then a brief period as non-Executive Chairman.

On the topic of Brian Marsh, it has been rumoured that COO Alice Foulk is his daughter. I contacted the company’s PR representatives back in March about this and they informed me that Brian and Alice are not related. So the accusations of “nepotism” don’t seem to have any factual foundation.

He is still the largest shareholder, owning 39% of the business:

When I founded B.P. Marsh my belief was simple: that patient, partnership-led investment alongside talented entrepreneurial management teams could create exceptional long-term value. More than three decades on, with Net Asset Value having grown to £360.2m and a portfolio spanning international insurance and financial services markets, I believe that philosophy continues to be valid…

What gives me greatest pride, however, is not simply the financial performance, but the culture and reputation that the business has built over many years, one based on integrity, long-term thinking and genuine partnership.

The company has a new non-Executive Chair, Rebecca Shelley, with a background primarily in corporate communications (e.g. Group Communications Director at Tesco and Prudential).

CEO Dan Topping summarises the year in review:

The year was characterised by disciplined capital allocation and the continued expansion of the Group's international specialty finance and insurance distribution portfolio. B.P. Marsh increased exposure to several of its strongest-performing investments, including Pantheon, XPT and ATC, whilst also deploying capital into a new generation of high-growth insurance intermediaries, underwriting agencies and complementary financial services businesses.

And discussing how the business is handling a weaker insurance market:

Whilst commercial insurance pricing softened across certain markets during the year, the Board believes the Group's portfolio remains comparatively well insulated from broader market cycles. A significant proportion of the Group's investments are early-stage or recently established businesses focused predominantly on generating new business opportunities, rather than relying heavily on the renewal of historically priced insurance portfolios. As a result, many portfolio companies are driven more by entrepreneurial growth, talent acquisition, product development and market share expansion than by prevailing premium rate conditions alone.

Graham’s view

I’m very glad to be a shareholder here again, but there are a few details worth ironing out.

Firstly, the NAV per share as of year-end is before a 22.3p dividend that was paid in March. So I reduce the current NAV per share to 937.5p.

This gives a discount to NAV today of 26% according to my calculations.

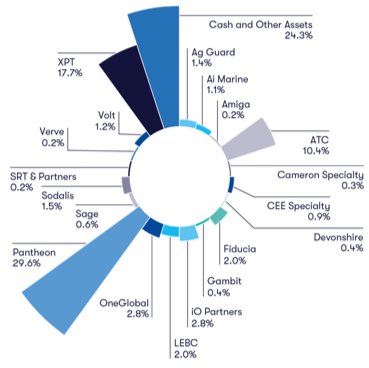

I’d also like to reiterate that the diversification of the portfolio is limited, due to some large positions:

The company has even continued to increase its stake in Pantheon in the new financial year, as noted here.

To help quantify the concentration, I’ve calculated the Herfindahl-Hirschman Index for the portfolio. I get an HHI of 1300 which is actually better than I expected.

The effective number of holdings is given by dividing HHI into 10,000. In this case, I get 7.5 holdings - so the level of concentration is equivalent to holding 7 or 8 different positions. Just something to be aware of, in case you are treating this like some sort of mutual fund - it’s more concentrated than that.

Personally, I’m not worried by this level of concentration. My own portfolio is far more concentrated, and BPM is just a small slice of that. I would even be open to owning more BPM at the current valuation. But before closing, I should mention a few more of the risks:

Brian Marsh’s holding - what might he plan to do with it?

The next generation of managers - they are all very highly experienced and trustworthy, but they also have very big shoes to fill. Very similar to the Warren Buffett question (disclosure: I’m long BRK.A).

Similar to Judges Scientific (LON:JDG), they may find it challenging to source good deals that move the needle and that they understand, now that they have a larger pool of capital to invest.

As I said, I am comfortable with all of these risks and would be happy to own more BPM. But I’m open to any counter-arguments!

Cohort (LON:CHRT)

Up 8% at £13.34 (£627m) - Full Year Trading Update - Graham - AMBER/GREEN ↑

Great news here - revenue and adjusted operating profit are ahead of expectations.

FY April 2026:

Revenue £303m (consensus expectations: £293.9m)

Adjusted operating profit of c. £36m (expectations: £34.7m)

Order intake £313m which the company points out is ahead of revenues

The closing order book therefore grows to a new record c. £620m, although only 1% higher than last year’s £615m order book.

Cohort has therefore beaten revenue expectations by 3% and operating profit expectations by almost 4%.

Visibility is excellent:

The order book underpins c.£253m of current market revenue expectations for the new financial year (30 April 2025: £230m) or c.80% cover.

This is the same percentage of cover that the company enjoyed at the time of last year’s trading update, also near the end of May.

Cash: net funds ended that year at around £3m, much improved from the £32.5m of net debt at H1. They expected net funds to be even stronger, but some expected receipts slipped into Q1 of the new financial year.

CEO Comment:

"I'm particularly pleased with the strong maiden full year contribution from EM Solutions. The business has made good progress in capturing opportunities for growth and collaboration with other Cohort subsidiaries.

"Our strong balance sheet and liquidity provides a robust platform from which to continue to invest in the business while considering further targeted acquisitions.

"The high level of order cover provides confidence in a strong 2026/27 financial year."

Graham’s view

We’ve been a little cautious on this one, worried about the H2 weighting it needed to hit full-year forecasts and the high valuation.

We were wrong on the first count, although I think there is still an argument to be made that the valuation here is punchy. The ValueRank is only 19, and Stockopedia categorises it as a Falling Star.

But when the facts change we should change our minds, and it turns out that there was nothing to fear about the H2 weighting - the company has more than fully delivered on what was expected in H2.

Defence has been a great sector in which to invest, given the unfortunate geopolitical trends of recent years. Cohort provides a wide variety of surveillance, communications, sonar and underwater systems. With the company continuously enjoying robust demand, and demonstrating sturdy earnings forecasts, I’ll nudge us up to AMBER/GREEN today.

Roland's Section

Zotefoams (LON:ZTF)

Up 7% at 426p (£211m) - Trading Update - Roland - AMBER/GREEN =

Today’s trading update from high-performance foam specialist Zotefoams covers the four months to 30 April 2026. It’s short but mostly positive.

Key points:

Group revenue rose by 26% year-to-date to £64.1m, or by +7.1% on an organic basis.

This result reflects a flat organic performance in the group’s largest region, aided by growth in smaller markets and a contribution from a recent acquisition:

EMEA: revenue +24% to £50.1m, although this was boosted by a £9.8m contribution from Spanish firm OKC, which was acquired in November. Excluding this, EMEA revenue was flat at £40.3m (FY25: £40.4m). Management says this reflects lower footwear revenue, but continued growth in Transport & Smart Technologies.

North America: revenue up 30% organically to £12.1m. Reflects increased manufacturing capacity from “our second low-pressure vessel” and good demand in Consumer & Lifestyle and Transport & Smart Technologies.

Asia: revenue of £1.9m (FY24: £1.0m), showing “good growth”. Continuing to invest in new facilities in Vietnam and South Korea which are expected to be operational “towards the end of the year”.

As a reminder, Zotefoams now reports revenue according to the markets in which the group generates revenue, rather than by product type. The downside of this approach, in my view, is that it obscures the performance of the company’s various product verticals and makes it difficult for us to gauge revenue growth or margins in different areas, beyond what the company chooses to disclose.

Financial performance for the period is said to have been in line with expectations, reflecting operational improvements and cost savings.

The integration of OKC (Overseas Konstellation Company) is also progressing to plan. Zotefoams paid up to €36m for OKC last year, which represented a 7.4x multiple of EBITDA. It’s said to be a leading specialist foam producer in Europe, with particular expertise in applications for “protective components, acoustic insulation and specialty packaging”.

In other words, OKC is mainly additive to the Transport & Smart Technologies side of the business, which should aid further diversification.

2026 Outlook - there is no change to guidance today:

The Board is encouraged by the solid start to 2026 and its full-year expectations remain unchanged. Whilst mindful of elevated uncertainty in the macroeconomic backdrop, we continue to expect demand in key target markets, together with the contribution from OKC, to more than offset the moderation in Footwear.

Roland’s view

I have been encouraged by the changes made by CEO Ronan Fox, who has curtailed speculative investment and focused on growth opportunities in the group’s core lines of business. This has led to several earnings upgrades over the last 12 months:

The result of these changes – so far – has been an improvement in quality metrics and and respectable revenue growth:

The Normalised EPS figure on the StockReport suggests Zotefoams’ adjusted earnings are expected to fall this year, but that’s not actually the case.

Last year’s results and forecasts from house broker Singer Capital in March show that the following progression is expected:

FY25 actual adj EPS: 38.0p

FY26E adj EPS: 40.8p (+7.4% vs prior year)

FY27E adj EPS: 43.5p (+6.6% vs prior year)

FY28E adj EPS: 47.3p (+8.7% vs prior year)

In other words, earnings are expected to continue growing at c.7% per year over the next few years.

One catalyst for this is expected to be the company’s new manufacturing and design facilities in Asia, which should come on stream later this year. Strong growth in markets such as aerospace and space is also helping to drive growth.

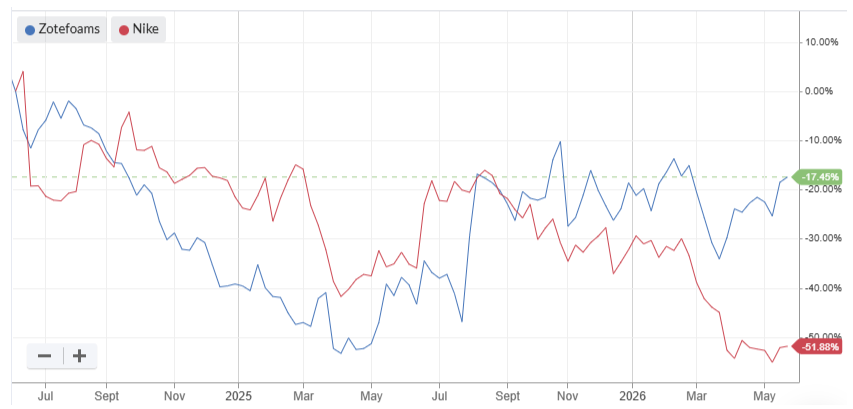

The expansion of the Transport & Smart Technologies business should also provide a second benefit for shareholders by reducing Zotefoams’ dependency on core customer Nike (NYQ:NKE), which I believe may have generated around half the group’s revenue in 2025.

If Zotefoams can continue to deliver on current forecasts then the shares might be too cheap at current levels.

However, by way of caveat I would note that the StockRank has fallen steadily since March, from 93 to 76:

There is clearly still some risk of macro disruption and perhaps more importantly, of further weakness in Footwear.

I’m fairly sure Zotefoams’ fortunes remain quite closely-linked to demand from Nike, whose earnings forecasts were recently downgraded (again):

I would speculate that one reason for the change in Zotefoams’ reporting might be to make it harder for shareholders to gauge the group’s exposure to Nike, which wasn’t disclosed last year (previously, it had been).

For this reason as much as anything else, I am going to resist the temptation to upgrade to be fully positive today and retain my previous AMBER/GREEN view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.