OpenAI has filed its initial registration statement (the S-1 form) with the SEC. On their blog, they wrote:

We expect it to leak so we’re just announcing it. We have not decided on timing yet; it may be a while because there are things we want to do that are likely easier as a private company.

This catches up OpenAI with its rival Anthropic, which also recently filed its S-1.

Meanwhile, the SpaceX IPO is happening on Friday:

Ticker code SPCX.

IPO price: $135 per share

Market cap: $1.77 trillion (the biggest IPO ever)

At this market cap, the valuation of SpaceX is over 90 times last year’s revenues, although that is measured prior to the acquisition by SpaceX of xAI. Based on 2026 forecasts, the price to sales multiple is a more modest 70x.

As an aside, I note that the FTSE finished flat yesterday, compared to Friday’s close, entirely unaffected by the weakness in AI shares. It’s up slightly over the past week, while the S&P 500 is down 2.5% and the NASDAQ is down 4%.

Overnight market movements:

The FTSE is set to open unchanged at 10,370

S&P 500 is up 0.3% at 7,430

Brent crude is down 1% at $93.20

Gold is up .4% at $4,350

Bitcoin is unchanged at $63,400

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

GSK (LON:GSK) (£77.5bn | SR94) | Agrees to buy Nuvalent, a Boston-based clinical-stage biopharmaceutical company focused on creating precisely targeted oncology therapies, for $10.6 billion. Net of cash acquired, aggregate investment estimated to be $9.4 billion (£7.1 billion). No change to GSK's 2026 full-year guidance range of 7-9% core operating profit and core EPS growth. | ||

Bellway (LON:BWY) (£2.0bn | SR57) | “...an increasingly challenging market, with customer demand having moderated in recent weeks… Notwithstanding this, and supported by our forward order book, we are on track to deliver FY26 underlying operating profit within the previously guided range of £320m - £330m.” Reiterates volume output of 9,300 to 9,500 homes. | AMBER = (Roland) [no section below] Trading improved in the early part of the spring, but has since moderated. Cost inflation on materials also remains an issue. Bellway says reservation rates remain higher than in H1, but are lower than during the comparative period last year, despite “a good contribution” from bulk sales. Land purchases remain selective and the balance sheet remains in good health. More broadly, I share the StockRanks’ view of this stock as a potential Contrarian play. As I discussed in March, Bellway’s c.40% discount to NAV is wide by historic standards and I view this as a well-run, good quality builder with very experienced management. The issue is the timing of any recovery, as highlighted by the MomentumRank of 1. This combination of in-line guidance but an uncertain outlook means I’m leaving my neutral view unchanged today. | |

Keller (LON:KLR) (£1.72bn | SR97) | Awarded a contract variation order of $207m in relation to the reconstruction of the I-40 highway in the US. Supports longer-term revenue visibility. KLR remains confident of delivering 2026 full year results in line with expectations. | ||

Oxford Instruments (LON:OXIG) (£1.70bn | SR70) | Full-year performance slightly ahead of expectations.Order intake +8% LfL, revenue down 3% LfL, adjusted operating profit down 1.6% LfL. Book-to-bill of 1.06x. “...we are confident in our ability to deliver attractive sustainable growth and value for all our stakeholders in the new financial year and beyond.”. | ||

Breedon (LON:BREE) (£956m | SR62) | Buys Falling Springs Quarry for an enterprise value of $120m (£90m). Falling Springs is “a well-invested, highly automated quarry with 185 million tonnes of limestone reserves strategically located approximately 15 minutes from downtown St Louis, Missouri”. | ||

Molten Ventures (LON:GROW) (£936m | SR88) | Portfolio company ICEYE Oy has raised approximately €450 million. Total transaction size >€1 billion. Valuation >€10 billion. Molten has sold c. £22m but the valuation of its ICEYE holding increases by £238m to £317m vs. March 2026 balance sheet value. This would increase Molten’s NAV per share by 117p to 877p. | ||

Fevertree Drinks (LON:FEVR) (£865m | SR45) | “The Group has made a solid start to the year and remains confident of achieving full-year market expectations.” £30m extension to the buyback programme. | AMBER ↑ (Roland) [no section below] Today’s in line statement suggests we could see modest revenue growth and a stronger recovery in earnings this year, noting that the correct comparator for consensus revenue forecasts of £386m is £375.3m. This adjusted figure is used for comparability as it includes invoiced revenue in the US, not just the royalties Fevertree actually earns through its recent partnership with Tap Global (LON:TAP). The upshot of this is that expected sales growth in 2026 is just 2.8%. As Mark has highlighted previously, this level of top line growth is probably lower than we’d want to see from a successful, branded consumer goods business. For me, the acid test will be whether Fevertree’s margins can recover towards the above-average levels seen historically. As things stand, the stock looks expensive, but consensus forecasts suggest double-digit earnings growth in both 2026 and 2027. That could repair margins and bring the valuation to a more reasonable level. With net cash and no particular problems evident, I think a neutral view is fair here. | |

Costain (LON:COST) (£514m | SR95) | Selected by TfL as one of three contractors on its Infrastructure Improvement Framework, which carries a total value of approximately £700m. Projects to be awarded over a two-year term, with an option of a two-year extension. No reference to expectations. | ||

| Seraphim Space Investment Trust (LON:SSIT) (£444m | SR93) | ICEYE Financing Round | ICEYE is currently SSIT’s largest portfolio holding. “Based on the announced valuation, the implied uplift in the fair value of the Company's holding would be approximately £202 million, which would represent a 102% increase in fair value and would be equivalent to an increase in NAV per ordinary share of approximately 73p.” | AMBER = (Graham) I would have to say that the €10 billion valuation of ICEYE is highly speculative. At a forward price/sales multiple of 20x, there is no other conclusion I can draw. The 73p increase in NAV arising from ICEYE’s new valuation leads to a new NAV per share for SSIT of over 250p. SSIT has enjoyed a c. 41% increase in its total NAV from this single event. These back-of-the-envelope calculations suggest that SSIT is currently (at 212.5p) trading at a c. 15% discount to NAV. But there are some good reasons for caution. |

VAALCO Energy (LON:EGY) (£432m | SR50) | The Baobab field on CI-40 block, offshore Côte d'Ivoire is back online following the successful Baobab Ivoirien FPSO vessel refurbishment. | ||

MJ GLEESON (LON:GLE) (£142m | SR45) | Gleeson Land has been extensively engaged in the sale of a site which would account for c. 50% of the total plots to be sold in FY2026. The transaction is now unlikely to complete in the current financial year. Also two smaller transactions, originally expected to complete in FY26, are now expected to conclude in H1 FY27. Adjusted PBT for FY26 to be £7.5m lower than current market expectations. | BLACK (AMBER =) (Roland) This is a big profit warning, with pre-tax profit guidance for the year ending 30 June cut by c.40%. However, Gleeson’s share price has already fallen by a similar amount since February and I would argue the risk of a warning – previously well flagged – was already priced in. Based on the company’s H1 NAV of 522p per share, Gleeson now trades at a discount of more than 50% to its book value. While there’s some debt, I don’t think it should become problematic and would view this stock as a potential value play. The problem is that there’s currently no sign of any catalyst for a recovery and market conditions could still worsen. For these reasons, I’ve left my previous neutral view unchanged today. | |

Jubilee Metals (LON:JLP) (£86m | SR24) | Run-of-mine (ROM) deliveries to Sable refinery and refining activities recommenced following the successful expansion of Pit 2 as part of the pre-stripping under the updated mine plan to combine Pits 2 and 3. Targeting 6,000tpm for June, rising to 10,000tpm by October 2026. | ||

Andrada Mining (LON:ATM) (£80 million | SR20) | High-grade lithium mineralisation confirmed across multiple drill holes, with consistent associated tin and tantalum mineralisation confirmed across all holes. Has now completed Stage 1 drilling campaign of 143 holes. | ||

Orosur Mining (LON:OMI) (£80 million | SR11) | First new hole at APTA (MAP-106) returns 229.7m @ 0.88g/t Au with “numerous higher-grade intervals”. Results are said to have “substantially enhanced the prospectivity of APTA with three areas of potential requiring follow up”. | ||

LBG Media (LON:LBG) (£73m | SR78) | Revenue +19%, pre-tax profit down 79% to £1.8m. Lower margins driven by “planned investment in our Direct sales and operations”, as well as an adverse revenue mix. Outlook: now expects FY26 revenue of £100-107m and adj EBITDA of £15-20m (prev. £110m and £22m). | BLACK | |

Time Finance (LON:TIME) (£42m | SR70) | Strong performance has continued. Year-end (31 May) gross lending reached £217m and is currently at £250m, an all-time high. Q4 TU scheduled for 25 June. | ||

Rome Resources (LON:RMR) (£27m | SR24) | 2026 field programme starting at three priority targets in New Brunswick, targeting tin and tungsten. | ||

Vianet (LON:VNET) (£20m | SR93) | Revenue +1.5%, adj operating profit -7.6% to £3.1m. EPS -51% to 1.43p. Hospitality business gaining traction with expanded offering. Outlook: well-positioned for sustainable medium-term growth. | ||

FIRST CLASS METALS (LON:FCM) (£17m | SR15) | Has raised £1m before costs through a placing of 26.3m new shares at 3.8p per share, a 9.5% discount to the closing price on 8 June 2026. | ||

Alien Metals (LON:UFO) (£13m | SR17) | Execution of joint ventures at Elizabeth Hill Silver and Munni Munni PGM projects has reduced funding requirements. Net loss of $0.7m in 2025, with year-end net cash of $1.5m. Raised £2.8m in placings last year. Going concern warning: current resources are not sufficient to cover projected expenditure over the coming year. | ||

Thor Energy (LON:THR) (£12m | SR29) | Phase-2 soil air geochemistry survey at the HY-Range project has recorded natural hydrogen readings of up to 3% (30,000 ppm) on licence, while validating three of Thor’s highest-priority exploration focus areas. |

Graham's Section

Seraphim Space Investment Trust (LON:SSIT)

Up 14% at 212.5p (£664m) - ICEYE Financing Round - Graham - AMBER =

We haven’t covered this much but I understand that it's a popular and interesting story, often featuring in our list of “Most Viewed” stocks.

I initially took a look at it in April at a share price of 180p.

It has been as high as 270p, before dropping back:

Today’s update relates to a satellite company originally from Finland, ICEYE, in which both Seraphim Space Investment Trust (LON:SSIT) and Molten Ventures (LON:GROW) are invested.

A description of ICEYE, from its own website:

ICEYE owns the world's largest and most advanced SAR (synthetic aperture radar) satellite constellation. We deliver persistent monitoring capabilities to detect and respond to changes in any location on Earth.

Key points:

ICEYE is privately raising €450m at a valuation of over €10 billion

At March 2026, ICEYE was 47.1% of SSIT’s NAV.

The new valuation would increase SSIT’s NAV by 73p

The Chief Investment Officer at SSIT’s manager says:

"For SSIT shareholders, this financing round demonstrates the Company's ability to provide access to category-leading SpaceTech companies at the forefront of some of the most important technological and geopolitical trends shaping the global economy."

Graham’s view

Before checking SSIT as a whole, I’d like to briefly look at some of ICEYE’s financials.

It posted its 2025 results as follows:

Revenue >€250m

EBITDA >€100m

Cash >€350m

Cash from operations >€130m

Contracted backlog €1.5 billion

They launched six new satellites, bringing their total number of launched satellites to 70.

They said that ICEYE “doubled in 2025 and is set to grow at a similar rate in 2026”.

Now let’s suppose that ICEYE’s revenue reaches €500m this year.

At a €10 billion valuation, that’s a price to sales multiplier of 20x. Great value compared to SpaceX, at least!

All references to EBITDA and cash from operations are irrelevant as the tooth fairy doesn’t pay for capex, not even in space.

To my eyes, therefore, I would have to say that the €10 billion valuation of ICEYE is highly speculative. At a forward price/sales multiple of 20x, there is no other conclusion I can draw.

Seraphim Space Investment Trust (LON:SSIT)

Turning away from ICEYE to look at SSIT, this is now a FTSE-250 component.

Q3 results were published last week with the following info:

NAV £421m as of March 2026

NAV per share 177.6p, up 24.8% quarter-on-quarter

Shares in issue 237m

This was a tremendous quarterly gain, “largely due to continued strong performance of ICEYE, funding rounds at Xona Space Systems and Tomorrow.io and the HawkEye 360 indicative IPO pricing…”

Their portfolio was made up as follows:

ICEYE 47.1%

ALL SPACE 13.6%

HawkEye 360 9.8% (Stockreport: HawkEye 360 (NYQ:HAWK))

Xona Space Systems 6.7%

…and various smaller positions.

The 73p increase in NAV arising from ICEYE’s new valuation leads to a new NAV per share for SSIT of over 250p. SSIT has enjoyed a c. 41% increase in its total NAV from this single event.

These back-of-the-envelope calculations suggest that SSIT is currently (at 212.5p) trading at a c. 15% discount to NAV.

But there are some good reasons for caution:

A highly concentrated portfolio with ICEYE being responsible for the vast majority of value means that NAV becomes less useful as a metric.

ICEYE’s valuation is itself open for debate and in my view should be controversial. Over what timeframe will it conceivably generate €10 billion of value for its investors, when its total revenue backlog is currently about one seventh of this?

SSIT itself is involved in heavy fundraising activity. 137m new C-shares have already been issued. While the dilutive effect of these shares is being mitigated in the short-term by keeping them distinct from SSIT’s ordinary shares, there could be complications arising from managing two separate pools of capital and attempting to merge them over time.

I’m going to stay neutral on SSIT. To be clear: I do not understand the value of ICEYE. And SSIT itself is now largely being driven by ICEYE’s valuation. But if I view SSIT purely as a vehicle with which to own space-related investments, and considering that the valuation of these investments is only going upwards for the time being, I can remain neutral.

If the space theme turns out to be a bubble (which I strongly suspect that it is), and it pops, I’ll want to have a negative stance on SSIT then. But for now, it seems that we are go for launch.

Roland's Section

MJ GLEESON (LON:GLE)

Down 4% at 238p (£139m) - Update on Gleeson Land - Roland - BLACK (AMBER =)

In February, I highlighted housebuilder Gleeson’s dependency on a big contribution from Land sales in H2 to meet profit expectations for the full year, which ends on 30 June 2026.

While lumpy contributions from the group’s Land business are the norm, this situation seemed more uncertain than usual, with a single site expected to account for 50% of all plot sales in FY26. The risk was that this – and other land sales – might slip into FY27, triggering a profit warning.

Today we have confirmation that this is what’s happened:

The majority of conditions required to achieve formal technical approval have been agreed, and the Group expects to conclude the remaining conditions soon. Completion of the transaction is now anticipated during the first half of the new financial year.Two additional, smaller land sales are also now expected to slip into FY27. This is said to be due to delayed decisions by major housebuilders, reflecting the current market environment.

Gleeson Homes: the good news is that trading at the group’s homebuilding business is in line with full-year expectations.

Revised outlook: the delayed land sales mean that MJ Gleeson’s adjusted pre-tax profit for the year is expected to be c.£7.5m below expectations.

Previous market expectations for pre-tax profit are given as being £16.4m to £18.5m, with a consensus of £17.8m.

That means this is a big miss – today’s revised guidance suggests pre-tax profit could be c.£10m, or around 40% below previous consensus.

Roland’s view

The market reaction to today’s profit warning has been muted, with the shares down by just 4% as I write, One reason for this may be that today’s warning was widely expected – the shares have already fallen by c.35% since February’s interim results:

Broker consensus has also continued to decline since February, most recently following the trading update on 1 May:

I don’t see any particular reason to doubt that the delayed land sales will complete in FY27, so this potentially helps to underpin forecasts for the year ahead.

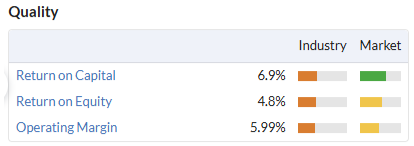

Deep value? Gleeson’s valuation is already deeply discounted, with the shares trading at a discount of more than 50% to the group’s last-reported book value of 522p per share, or £305m.

The majority of this is accounted for by inventories of land and homes under construction which were valued at £417m at the end of 2025. Barring a housing market meltdown, I’d expect these assets to maintain most or all of their value when eventually sold.

One risk is that net debt will have risen further since the half-year mark, due to the delayed completion of these land sales. While H1 net debt of £22.5m looked comfortable against previous profit forecasts, leverage is relatively higher versus today’s revised guidance.

Another potential concern is that the twin pressures on housebuilders’ margins from a lack of pricing power and materials cost inflation will persist for some time, leaving them generating very low returns on equity and thus justifying discounted valuations.

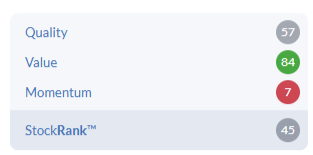

However, on balance I think Gleeson shares are cheap enough to be of interest as a value or Contrarian investment – a view reflected in the StockRanks:

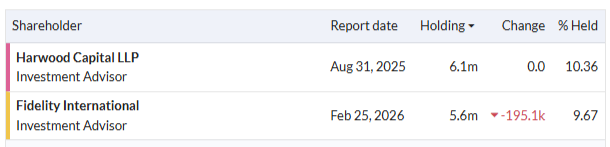

I note that Harwood Capital has become Gleeson’s largest shareholder, suggesting others see value here too:

As with Bellway above, the main risk I can see lies in the uncertain timing of any improvement in market conditions. I was neutral on Gleeson in February and don’t see any reason to change that view today. AMBER =

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.