Sixteen companies were forced off the Alternative Investment Market last year because of financial stress or insolvency. That was up from nine companies that suffered the same fate in 2017. When you add them to those that hit problems but somehow managed to cling on (albeit with broken reputations and battered share prices), it’s a reminder of just how perilous the AIM market can be. So how can you try to avoid these kinds of problems?

AIM is popular with investors looking for the kind of explosive growth that happens when smaller, less well known companies come good. A lack of decent research means there can be hidden gems in AIM’s wild expanse of just over 920 mostly small-cap stocks. It’s a market that captures the essence of Jim Slater’s famous observation, that “elephants don’t gallop”. His message being that big companies don’t grow anywhere near as fast as small-caps, and neither do their share prices.

To be fair, there have been some great examples of that kind of growth in recent years. With investors risk-on and funds flowing into speculative plays, some names have seen big re-ratings. They’ve included companies like Burford Capital, Fevertree Drinks, Abcam, Boohoo and Clinigen. From a market cap-cap perspective, Burford’s £3.7bn valuation wouldn’t be out of place in the FTSE 100. Three years ago, it was worth just £400 million.

These are now some of the biggest companies quoted on AIM. Their performances through 2016 and 2017 contributed to the index outpacing all the other main UK benchmarks. But when markets slid through 2018, it was AIM that suffered most - falling 18.2 percent through the year.

Sudden shocks

While AIM has had successes, the trade-off for investing in such a fast-growth, light-touch place is that things go wrong. Unlike the main market, where corporate distress is often (although not always) flagged by analysts, AIM calamities can take everyone by surprise. Just ask investors in Patisserie Holdings.

In 2018, the group behind the Patisserie Valerie chain of cafes - which is majority owned by the chairman and entrepreneur Luke Johnson - was plunged into chaos by an accounting crisis. The full details of what could be a serious fraud still aren’t known. But the shares have been suspended for more than three months while investigations take place. For investors in…

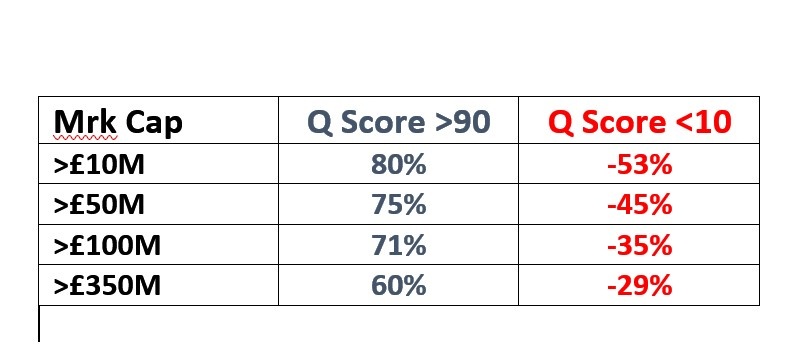

.JPG)