Any thoughts most welcome Paul

How do you know they are buys? Yes lots of volume yesterday but the price has not gone up.

Any thoughts most welcome Paul

Once sanity returns to the coal price Opg Power Ventures (LON:OPG) should take off again. Company have kept quiet about the extent of their coal hedges so maybe some investors are nervous, they are committed to fixed term tariffs with their customers (who have probably used less energy than usual). Therefore the extent to which their costs are unhedged is unclear. NTAV is materially higher than before the pandemic as the company has signifcantly reduced debt since then, so the current low SP is unjustified in my view even if they have to take a short term trading loss until they renegotiate client tariffs.

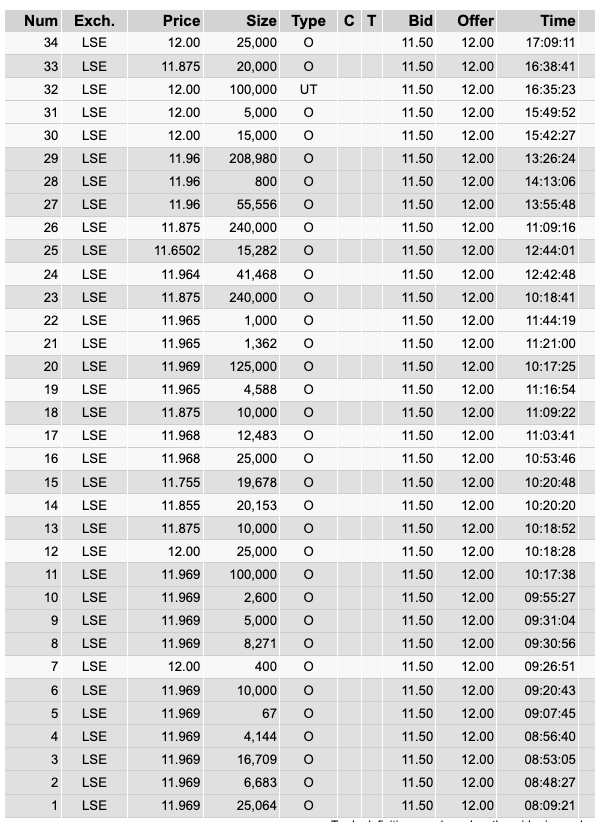

Fridays trades from ADVFN. Not sure of the two 240k trades, but the trade price suggests that they are almost all buys; that's just my guess based on obtaining real time buy and sell quotes during the day. To answer your question Ray, I don't know.

Good morning,

There was a very positive appraisal of Opg Power Ventures (LON:OPG) on Friday‘s MoneyWeek podcast with Investment Fund manager and financial author, Andrew Hunt.

He was asked, by Merryn Web, which companies he believes are materially undervalued in the current market. He was extremely bullish regarding the prospects of the company. The subject of the podcast was deep value investing.

Maybe this had a small effect on the purchases you mention, Turbo?

Interesting listen mcav, thanks for that. Here's a summary of what Andrew Hunt says:

“OPG Power which is listed on AIM have state of the art coal fired power stations in India. India is now recovering really strongly at the moment and power demand is going through the roof, so this sounds like quite a nice way of exposure in India. Do you know what the multiples of this company are? OPG Power is almost debt free, which is very rare for a utility. You can go out today and buy it on a PE of 4 and at a 45% free cashflow yield. That’s probably, what, a tenth of what other investors are paying for Indian exposure. I mean ….. wow!”

Andrew Hunt: why it's a great time to be a deep value investor

Unfortunately I owned £OPG down from 100p but I always quite liked the proposition. I heard the podcast on Friday too and it made me take another look. Certainly looks a good deal of potential upside here.

I very much doubt this stock will gather any meaningful momentum.

Firstly, it's coal, and with that investor sentiment will continue to be negative, stock prices are driven investor sentiment, nothing else. Coal is the dirtiest but unfortunately the cheapest of fossil fuels.

Secondly, utilities tend to be dividend payers and so attract income seekers. OPG pay no dividends, so this second tranche of investors will not look to buy this stock either. IMO if they wanted a stronger market cap they would have been better offering a dividend than paying down debt, clearly they are cash generative and so I'm presuming this could have been an option.

A question earlier in this chain re why recent buying pressure hasn't moved the share price, I'm guessing two fold, firstly they are on the whole tiny trades and secondly I suspect there are a quite a few sellers in the market.

Didn't realise Ben Hobson has recently written about Opg Power Ventures (LON:OPG) under the 'Articles' section of Stockopedia, makes an interesting read.

Why OPG Power Ventures could be well placed to recover from volatility

coal price has dropped from peak of over $250 in early Oct to $150 today so price trend is positive for Opg Power Ventures (LON:OPG) (I hold). The stock is very illiquid, 50% being held by the chairman so most price moves are on low volume and are just noise. Upto 15% Share buyback just approved at the AGM which suggests the company has spare cash . Management get a performance payout if SP hits 28p by Apr 2022

Will the resolve encouraged by Boris at COP26 rapidly dissolve as I expect? I suspect India will be the first to disappoint he and Greta.

Thanks but coal did shoot up around 10% on that day, 141 to 156, so I thought there maybe a connection.

I'm sure many targets will be missed as in the past. Some will be too late anyway. It may even accelerate deforestation before the deadline. The USA, China and India did not sign the coal pact.

If the large polluters don't reduce emissions then we are stuffed. China and USA account for over 40% of pollution. India is third. Methane, the largest polluters did not sign either.

Trading update Summary for Nine Months to 31 December 2021:

· Total generation of 1.55 billion units (1.47 billion units for nine months FY21);

· Plant Load Factor ("PLF") for the period at Chennai was 57% (54% for nine months FY21);

· Average tariff for nine months FY22 was Rs 5.53 per kWh (Rs 5.52 per kWh for nine months FY21);

· Net debt was £16.5 million (£16.2 million at 31 March 2021);

· Investment in Atsuya Technologies Private Limited in line with the strategy to diversify into ESG compliant opportunities and to reduce and offset carbon emissions;

· Indian economy is recovering from COVID-19 pandemic and lockdown; IMF has projected a 9% growth rate for Indian economy in FY22 against global growth rate projection of 4.4% for CY22

Long term holder, waiting for OPG Power Ventures (LON:OPG) to gain traction. Decided to top up today.

Unaudited results for the six months ended 30 September 2023 published in Dec 2023 were good I thought:

Do I see tentative signs of an uptick in the SP, or am I just imagining it....?

Turbo, the price rallied to 14.5p from 8p on expectation of the news last september. Profit taking since then has resulted in a pullback to 10p support, and as soon as it bounced off I bought in. Next set of results is expected to be better than last year as you've pointed out, so I'm expecting some decent share price action leading up to results.

Broker target price of 27p.