For much of the last few years, anyone betting on a recovery in fund manager stocks has been long and wrong, as the saying goes. That has included me at times.

For years, active managers have faced steady pressure on fees due to competition from cheap passive funds. More recently, most UK fund managers have also faced sustained outflows as investors have jumped ship to US equities or simply withdrawn from a lacklustre UK equity market.

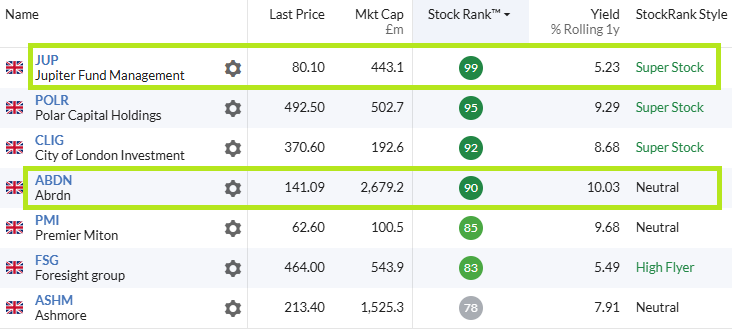

However, the StockRanks are pointing to a number of potential opportunities in this sector, notably in two of the most unloved fund managers of all – Abrdn (LON:ABDN) and Jupiter Fund Management (LON:JUP).

I’ve been taking a closer look at both of these firms. I think this could be a case where the objective metrics powering the StockRanks are highlighting an opportunity that’s not yet being recognised by the wider market.

Despite the (many) good reasons to be cautious about these businesses, I think the investment case for each is worth exploring.

Abrdn (LON:ABDN)

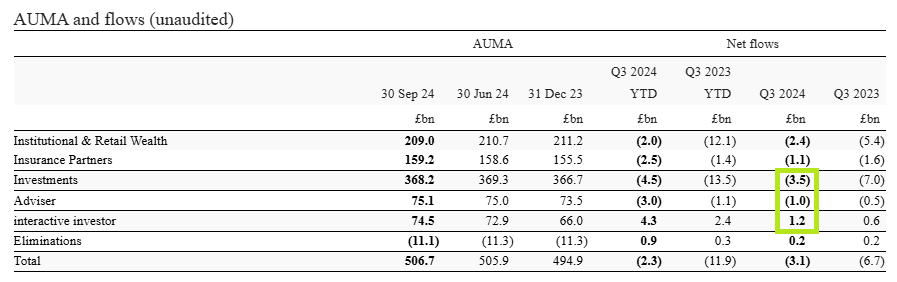

Fund manager Abrdn is a traditional fund manager, but the group also has an Adviser platform (providing services for financial advisers) and owns the interactive investor retail investment platform.

In other words, Abrdn aims to serve the full spectrum of investment clients, from institutions such as pension funds through to DIY investors.

While I was planning this article, the company issued a Q3 trading update revealing net outflows of £3.1bn during the third quarter. These were driven by outflows from the funds and adviser divisions, offset by inflows to interactive investor.

While this was an improvement on the net outflows of £6.7bn seen during Q3 2023, it wasn’t what the market was hoping to hear:

Continued outflows are obviously a potential concern. But Abrdn is hardly alone in this regard. I don’t see it as a dealbreaker at the current valuation.

Despite the structural headwinds to their business, my working assumption is that the cycle will turn for active managers at some point. On this basis, I think there are some good reasons to think that Abrdn could be attractively priced at current levels. Let’s take a closer…