Publicly listed since 2003, Bisalloy Steel (ASX:BIS) offers a range of products including wear-resistant steel plates, military-grade armour, structural steel, and mining equipment. BIS is Australia’s only quench and tempered (Q&T) steel plate producer which serves our mining and defence industries. For further information on BIS’s operations refer to my previous article written on 25/10/2023. You can read it here.

Key Points from my last article were:

I was happy with BIS’s financial performance, profitability ratios and, asset liquidity;

Higher input and freight cost were seen as head winds for FY24 and;

BIS provided little forward guidance but was expecting FY24 to be another positive year.

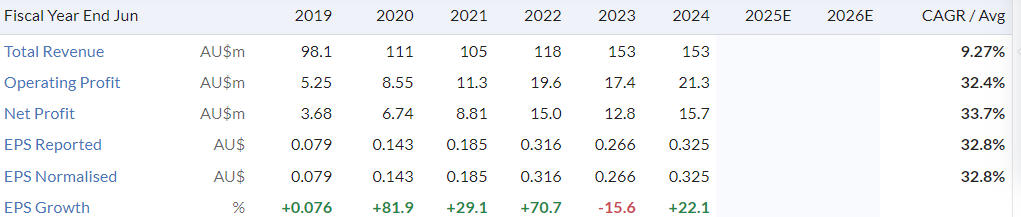

Fast forward to today and FY24 was indeed another positive year for BIS. Despite revenue being flat, they increased margins, profits, and substantially increased their operating and free cash flow. This result was mainly due to the BIS Australian operations being more profitable this period due to lower input and freight costs in the second half of FY24, with NPAT for the segment up from $11.8m in FY23 to $15.9m in FY24 (This figure in not adjusted for share of profit for their JV. Which is why it is higher than reported NPAT).

However, the improved performance in their Australian business was offset by a weaker performance from their Indonesian partnership. But according to BIS, all their overseas partnerships and JV’s did contribute positively to profitability in FY24, with their Chinese JV reporting a profit of $2.4m.

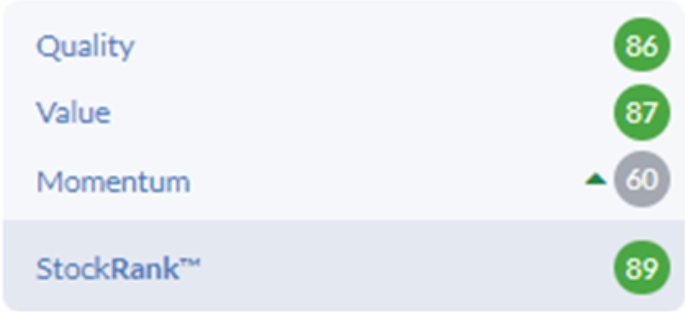

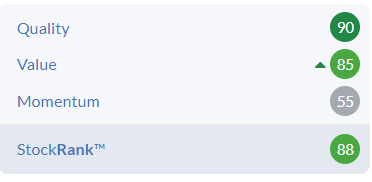

StockRank:

As you would expect on the back of improved earnings, margins, profits and cash flow, BIS has improved their quality factor. With value and momentum factors experiencing a small decline. The rise in quality was offset by the small decline in momentum and value and resulted in BIS’s overall StockRank remaining flat.

October 2023 StockRank

September 2024 StockRank

For me, I like the fact that Value has…