FTSE 250 industrial heat treatment specialist Bodycote is in good financial health, reasonably valued, and is benefiting from a post-pandemic rebound in aerospace manufacturing.

Bull points

- Rising aerospace demand as Boeing and Airbus address order backlog

- Defence spending expected to increase from 2023

- Stock looks reasonably valued against cyclical average earnings

- Strong balance sheet, good cash generation

- Track record of above-average profitability

Bear points

- Automotive sector slowdown could hit earnings

- Broader recession might also impact aerospace

- Historical growth has been inconsistent

- Exposure to faster-growing emerging markets is limited

Profile

About the Stock

Bodycote (LON:BOY) operates in the industrial sector and is part of the Machinery, Equipment & Components industry group.

Its shares currently trade at 535p on the LSE Main Market. Bodycote is a member of the FTSE 250 and has 191m shares in issue, giving a market cap of £1bn. Free float is 99%, so liquidity should be excellent.

The StockRanks are broadly favourable for Bodycote, with a particularly strong QualityRank. The company is classified as an Adventurous Mid Cap Neutral stock.

After a one-year share price decline of 35%, the stock is showing signs of stabilisation and an improving StockRank trend, suggesting a possible opportunity:

About the opportunity

Bodycote shares appear to offer reasonable value, with attractive growth and income qualities when compared to the broader market average:

Bodycote can be described as a quality business that’s sensitive to the business cycle. As I discussed last week, the stock’s valuation suggests that current earnings are running slightly below the 10-year cyclical average.

The opportunity here is for Bodycote to benefit from improving post-pandemic demand in the aerospace, defence and energy sectors. The main headwind to the group’s growth is a nascent slowdown in the automotive sector, another key market.

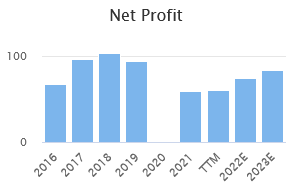

Broker forecasts suggest that profits could recover towards pre-pandemic levels over the next 18 months:

Recent trading shows supply chain issues easing and reduced levels of demand volatility. This should improve efficiency within the business, supporting margins.

Bodycote’s large-scale, specialist facilities also offer benefits to clients seeking to minimise their energy consumption and carbon footprint. As the company’s plants aggregate multiple customers’ work, they run at higher levels of utilisation than individual customers…