Good morning!

Congrats to shareholders in Spectris (LON:SXS) - news emerged yesterday afternoon of a possible cash offer at £37.35 (a premium of over 80%!).

Spreadsheet that accompanies this report: link.

We ran out of time for today, cheers!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Frasers (LON:FRAS) (£3.3bn) | Frasers confirms it is considering a possible offer for Revolution Beauty (LON:REVB), which would be all cash if it is made. | ||

Spectris (LON:SXS) (£3.2bn) | Possible cash offer from private equity at £37.35 plus £0.28 interim dividend. Due diligence ongoing. | PINK (Graham) [no section below] | |

Bellway (LON:BWY) (£3.2bn) | Fully sold for y/e 31 July 25, FY units 8,600-8,700, “on track” to deliver FY volume and profit growth. Average selling price exp £315k (FY24: £308k). Forward order book +7.7% at 5,759 homes, expect further increase before year end. | AMBER (Roland) [no section below] Today’s update from the housebuilder supports the view that housing demand may be recovering, with management guiding for cumulative volume growth of 20% in the two years to 31 July 2026. As far as I can see, profit expectations are unchanged today. These suggest to me Bellway’s return on equity will remain in mid-single digits in both FY25 and FY26. The company is promising an update on its capital allocation plans later this year which may alter this view. But for now, I’d argue this level of profitability means the shares could be fairly valued at a slight discount to book value. Bellway’s share price has risen by 17% since I covered it in February, so I’m edging down our view to neutral. | |

Hochschild Mining (LON:HOC) (£1.6bn) | SP -22% to 236p | BLACK (AMBER/RED) (Roland) [no section below] Problems at the Mara Rosa gold mine mean that FY production is now expected to be well below previous guidance. This mine was previously expected to contribute c. 25% of group production this year. Based on the YTD run rate, I estimate today’s news could imply a c.10% reduction in FY production guidance for the group. Following the COO’s recent departure, HOC’s CEO has taken charge of this situation directly. An update on progress and revised FY guidance are promised in due course. HOC shares were trading on a modest P/E of 9 prior to today, but this relies on a stable gold price and hitting production targets – at least one of these now seems unlikely. I think it’s sensible to expect earnings forecasts to be downgraded based on today’s news, so I’m taking a cautious view until there’s more clarity. | |

Safestore Holdings (LON:SAFE) (£1.4bn) | Rev +4%, adj EBITDA -1.5% to £66.1m. LFL occupancy +0.6% to 78.2%. NTAVps +11.3% to 1,117p. | ||

Firstgroup (LON:FGP) (£1.1bn) | Rev +7.5%, adj op profit +9% to £222.8m. FY26: outlook in line with exps, adj EPS flat or better. | ||

Oxford Instruments (LON:OXIG) (£1.1bn) | FY25 results delayed due to audit request; remain in line with exps. NanoScience unit sold for £60m. | ||

GB (LON:GBG). (£675m) | FY25 in line with exps w/ rev +3%, adj EPS +14.9% to 17.4p. FY26 outlook unchanged. | AMBER/GREEN (Roland) The main weakness of these results seems to be limited top-line growth and weak profitability. However, free cash flow was strong and for investors who are willing to look past the bloated goodwill line on the balance sheet, I think underlying profitability could be attractive at the current valuation. I’m leaving our moderately positive view unchanged and will continue to watch GB’s turnaround with interest. | |

Tatton Asset Management (LON:TAM) (£363m) | Rev +23%, PBT +29% to £21.6m. Record net inflows of £3.7bn, AUM +24% to £21.8bn. Outlook unch. | ||

Filtronic (LON:FTC) (£285m) | Received follow-on SSPA order worth $32.5m for FY26. Confident will exceed FY26 rev exps. | AMBER/GREEN (Roland) | |

| Gulf Marine Services (LON:GMS) (£246m) | General Meeting | Shareholder GM request proposing board changes & dividend found to be invalid, again. | |

B.P. Marsh & Partners (LON:BPM) (£233m) | PBT +140% to £104.7m. NAV +42.4% to £326.4m (890pps). Outlook: “robust pipeline”. | GREEN (Graham) Looking at some data points, I think the current share price offers a discount to NAV that is fairly normal for BPM. While there is some risk that scaling up their investment strategy will bring challenges, I think they are highly credible. | |

Quadrise (LON:QED) (£90m) | Updates on various trials. Has momentum but some are taking “longer than originally anticipated” | ||

Vianet (LON:VNET) (£22m) | Rev £15.3m, PBT £0.9m (FY24: £0.8m). Confident for earnings growth in FY26 and beyond. | ||

Powerhouse Energy (LON:PHE) (£22m) | Very late results. Rev £0.5m, op loss £4.7m. Focus on marketing its feedstock testing unit in 2025. | ||

Surface Transforms (LON:SCE) (£17m) | Rev +13% (£8.2m). Loss after tax £22m. Outlook: continued growth. Material uncertainty. | ||

Zinc Media (LON:ZIN) (£16m) | Further Middle East Growth [contract award] | Seven figure commission in the UAE. No reference to any change in expectations. | |

Diales (LON:DIAL) (£13m) | H1 revenue flat (£21.6m), adj. op profit falls to £700k. Outlook in line. Higher enquiries in Q2/Q3. | ||

IXICO (LON:IXI) (£11m) | Imaging analysis via IXICO’s AI-driven platform supported FDA clearance for a new blood test. |

Graham's Section

B.P. Marsh & Partners (LON:BPM)

Up 4% to 650p (£241m) - Final Results - Graham - GREEN

B.P. Marsh & Partners Plc (AIM: BPM), the specialist private equity investor in early-stage financial services businesses, announces its audited Group Final Results for the year ended 31 January 2025.

I tend to be positive on this one due to its tremendous track record as an investor in its specialist niche - startup financial companies, mostly in the insurance sector.

Today’s results for FY January 2025 are excellent:

PBT £104.7m (previous year: £43.6m).

NAV increases by 42% or £97m to £326m.

NAV per share 890p or 847p fully diluted for shares in the employee benefit trust.

The extraordinary profits were helped by two large disposals during the year, so cannot be expected to repeat on a regular basis.

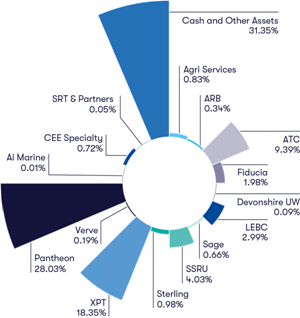

Here’s a visual breakdown of the company’s NAV. Overall diversification seems quite good to me, given that BPM is still only worth c. £300m:

Comment by Chairman Brian Marsh:

"I am pleased to report a year of exceptional performance, realisations, new investments, and cash returns to shareholders. B.P. Marsh creates real value, and, with a robust and diversified portfolio, we will continue to identify opportunities, support entrepreneurial teams and exit only when it is appropriate.

BPM finished the year ending Jan 2025 with a cash balance of £74m. The focus remains on new investments, but it has also enlarged its shareholder rewards:

Dividends: £8m is being paid out for the current year (including a £3m special dividend), and then £5m in each of the next two years. That’s 21.64p per share followed by 13.56p per share (twice).

Buybacks: under its current policy, BPM can buy back its own shares when they trade at a greater than 10% discount to their most recently announced NAV per share. As their most recently announced NAV is now 890p, I guess this means the company can buy back shares below 801p.

With a share price of only 650p today, I have to think they’ll buy back shares here. However, there’s an important limitation: the Chairman already owns 38% and the company doesn’t want to trigger mandatory bid obligations for him, or to increase his stake to over 42.5% (this was decided at a general meeting recently). So in practice, any buybacks are likely to be modest in size.

New investments: following the successful exits last year, BPM has also been reinvesting in the new financial year (FY Jan 2026). In both April 2025 and June 2025, it made new £10m investments.

Outlook sounds good, with good prospects for more deals:

We continue to demonstrate our ability to create long-term value and deliver strong returns. Deal origination remains active, particularly in the underwriting and broking sectors, and the new investments made during the year reflect the Company's proven capability in identifying well-positioned and compelling opportunities.

The Group remains committed to supporting its portfolio companies, not only with follow-on capital where appropriate, but also through strategic input aimed at unlocking further growth. With a robust pipeline of prospective investments in both the UK and international markets, supported by a strong cash position, the Group is well placed to act decisively where it sees exceptional potential.

Market commentary: for those who track the insurance sector, BPM informs us that premiums continue to soften, due to competition among insurers. Global insurance rates declined 3% in Q1.

Graham’s view

BPM is a class act and I regret not owning it currently - I have owned it in the past. Probably I should try to pick up a few while it’s still trading at this discount to NAV. Although it’s always a little tricky to buy when the chart looks like this!

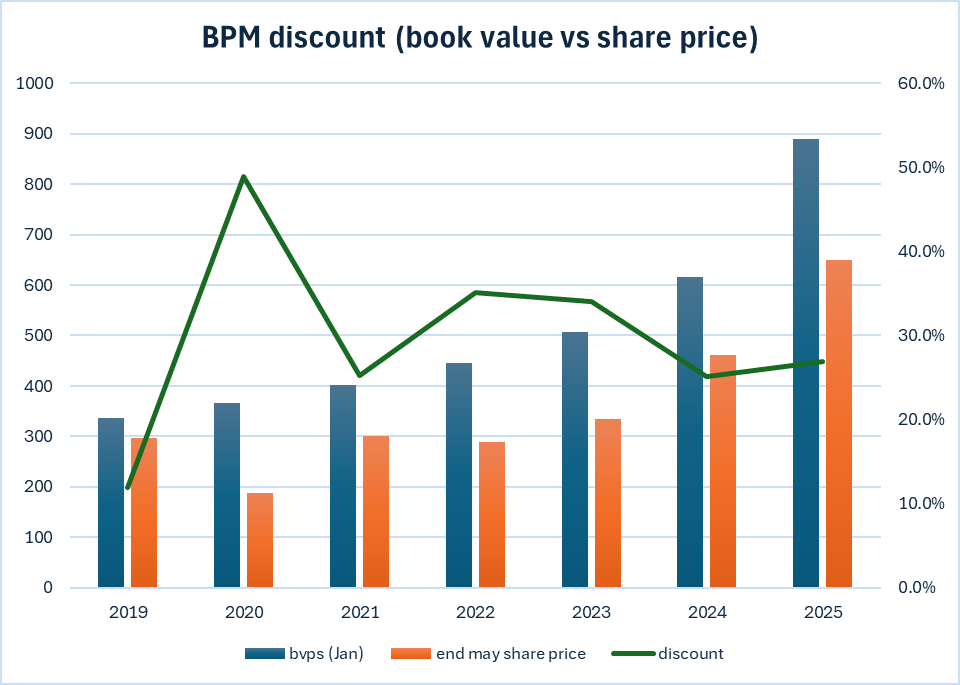

I’ve gone back over the last five years and checked where the company’s share price was trading at the end of May each year, vs. the book value it published for January that year.

For the current year I’ve used today’s share price. While these are only a few data points, it seems to me that the current discount to NAV (27%) is pretty normal for BPM. It has been higher than this, but it has sometimes traded a little lower. Given its track record, I'm inclined to think the risk/reward is attractive!

Brian Marsh is 84 years old and has taken a step back for many years, with the company being run by a very loyal MD and Chief Investment Officer.

While I try not to get into the weeds of BPM’s specific investments - that’s the job of the company - I have noticed that one of their recent investments is quite unusual. They’ve invested outside of the insurance sector in a “buy-and-build” opportunity in the alternative finance space, called iO partners.

This obscure new venture has just bought a stock funding outfit called Seneca and a probate lender called Provira. I’m intrigued to see whether it will succeed - as I’ve just said, it’s an unusual investment for BPM to be involved in! The global investment giant Janus Henderson is a co-investor.

Overall, I’m very happy to stay GREEN on this. It’s a stock that I would not mind owning again.

Roland's Section

Filtronic (LON:FTC)

Up 8% to 140p (£307m) - Largest contract award to date with SpaceX - Roland - AMBER/GREENE

the Board is now confident the Company will exceed current revenue expectations for FY2026

Filtronic has secured a significant follow-on order from SpaceX valued at $32.5m (£24m). This is the largest order to date from the US satellite company.

The order is for Filtronic’s “market-leading E-band Cerus 32 Solid State Power Amplifier” (SSPA) – this product is used in SpaceX’s Starlink ground stations. This is the product line that has driven the high volume of orders from SpaceX over the last year or so.

Filtronic expects to deliver the majority of the order in the FY26 financial year, which runs to 31 May 2026.

The company also confirms today that Filtronic has exercised all of the 10.9m warrants it was entitled to under the agreements satisfied to date. This is equivalent to 5% of the company. I believe these warrants were exercised at 92.8p, somewhat below the current share price.

SpaceX has also previously exercised warrants relating to a further 4.96% of the company, taking the total to date to 9.96%.

Seeing as there is no trace of SpaceX in the shareholder register, I wonder if the US firm has immediately flipped its Filtronic shares.

Assuming the latest 10.9m tranche of shares were sold at 130p, that might have generated a c.£4m profit for SpaceX – effectively a c.15% rebate on the value of this latest order.

Updated Estimates: ahead of today, consensus forecasts were for revenue of £50m in FY26.

Today’s order is for nearly half this amount (c.£24m), so intuitively we might expect today’s order to have a material impact on expectations for the year.

However, as I’ve mentioned previously, FY26 broker forecasts were already pricing in a certain volume of new orders still to be received. This is normal for many industrial businesses, but unfortunately Filtronic doesn’t report order/revenue coverage for the year ahead in the way that some companies do.

This means that we have had no way of knowing how much of the forecast revenue for FY26 was already underwritten by committed orders.

Fortunately, house broker Cavendish has provided an updated note today including new forecasts and providing some insight into this situation – many thanks for making this coverage available.

The change to Cavendish’s revenue forecast for the current year is surprisingly modest, in my view, and profit forecasts have been left unchanged:

FY25E revenue £55m / EPS 5.9p (unchanged)

FY26E revenue +8% to £54m (previously £50m)

FY26E adj PBT unchanged at £8.3m

FY26E EPS unchanged at 3.2p

These update forecasts seem to suggest that once again, much of today’s new order intake win was already priced into expectations.

These numbers also mean that the overall shape of profit expectations shown on the StockReport remains unchanged, with earnings expected to fall by 45% in FY26:

Cavendish says it has left profit forecasts unchanged today because it expects Filtronic to experience additional upfront costs relating to recent new business wins (e.g. ESA, Leonardo and Airbus).

Further cash investment “in support of growth” is also expected, meaning that net cash forecasts have also been reduced for the current year.

Filtronic shares are up by nearly 10% as I write. When paired with today’s unchanged earnings forecasts, this means that the shares are now trading on 44x FY26 forecast earnings. This valuation is reflected in the StockRanks’ very low value score:

No forecasts are yet available for FY27. I assume these will be initiated when Filtronic publishes its FY25 results, probably in late July/early August. In the meantime, this lack of visibility is a potential concern, in my view.

Roland’s view

I recognise that I’m at risk of sounding like a stale bear on Filtronic. This isn’t the case at all. I think the company’s achievements with SpaceX have been impressive and I’m very happy to see what could be another British engineering champion emerging.

However, based on current expectations, I think it’s fair to say the shares are expensive. I also think it’s fair to assume from today’s update and previous orders that at least 50% of FY26 revenue is currently expected to come from SpaceX, potentially from a single product type.

This kind of customer concentration is always a risk, especially as there seems to be a growing lack of visibility on future revenue beyond the current year.

Filtronic reiterated today that sales under the next phase of the SpaceX agreement are “subject to meeting certain criteria in relation to new technology”.

I don’t think management has provided much insight for outside investors on progress or timings relating to this new technology.

However, what’s clear is that Filtronic has been scaling up its cost base significantly – headcount rose by 16% in H1 25 and its manufacturing facilities have been expanded.

While recent contract wins with other non-SpaceX clients sound encouraging and should help to diversify the group’s revenue base, they haven’t moved the needle on forecasts. They also appear to require additional upfront investment.

My concern is that for some reason – political, commercial, or technological – the torrent of revenue from SpaceX could reduce to a trickle at some point, leaving Filtronic with a bloated cost base and too much capacity.

I would be more reassured if SpaceX had become a strategic shareholder with a near-10% stake, but this doesn’t seem to have happened. Instead, I’ve noticed that all of the company’s largest shareholders have been using this year’s strength to trim their holdings:

While Filtronic’s High Flyer styling remains unchanged, the StockRank has also started to fall recently, perhaps reflecting the stretched valuation:

Of course, I could be completely wrong. I think it’s fair to assume the underlying growth of the LEO satellite market will continue for some time yet, especially as European operators are increasingly planning rival systems to Starlink.

If demand for Filtronic’s SSPA type products remains strong and the company launches planned new products successfully, then the company’s growth could remain very strong for some time yet.

As I’ve stressed before, investors need to form their own view on this situation and decide how to proceed.

Personally, the combination of Filtronic’s valuation and the lack of any next-year forecasts means that I’m struggling to remain positive.

However, given the scale of today’s contract win and the stock’s continuing strong momentum, I feel objectively that it’s appropriate to remain moderately positive. My view remains unchanged ahead of the company’s year-end update and full-year results. AMBER/GREEN.

GB (LON:GBG)

Down 7% to 251p (£625m) - Final Results - Roland - AMBER/GREEN

Today, GBG, a global identity technology business enabling safe and rewarding digital lives, announces its audited results for the financial year ended 31 March 2025. These results are in line with the trading update published on 24 April 2025.

This digital identity verification specialist is a company I’ve seen as a potential turnaround and have been keeping an eye on.

Today’s results are billed as in line with guidance provided in April and expectations for the year ahead are said to be unchanged.

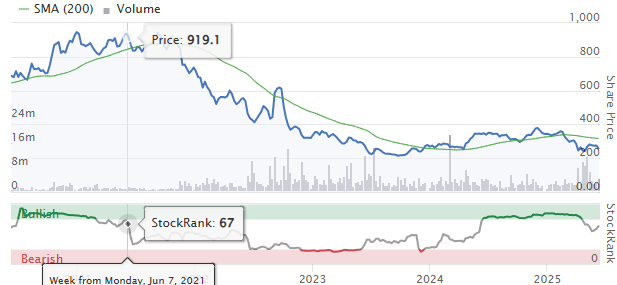

However, the market doesn’t seem impressed and the shares are down by 9% as I type, continuing a decline that’s seen the stock fall by over 70% in four years:

Let’s take a look to see what’s been happening.

2024/25 results summary: the company launched its GBG Go platform last year, which management says is an important step in the unification of its various services into a single global platform. Using GBG Go will allow users to “instantly verify identities and detect fraud”.

The group operates in three segments, two of which delivered revenue growth last year on a constant currency basis:

Identity +3.1%

Location +6.2%

Fraud -4.0%

In Identity and Location, net revenue retention improved to 101.1% (FY24: 99%), suggesting the firm’s products are fairly sticky and maintained their pricing power last year.

The fall in Fraud revenue was said to be due to the timing of licence renewals, with annual recurring revenue up by 5%.

This operating performance seems reasonable, although revenue growth seems pretty weak to me when inflation is taken into consideration.

This top-line weakness is reflected in GB’s group revenue, but profitability does seem to have improved last year:

Revenue +3% to £282.7m (constant currency)

Adjusted operating profit +9.5% to £67m

Adjusted EPS +14.9% to 17.4p per share

Net debt -40% to £48.5m

The numbers above translate into an adjusted operating margin of 23.7% (FY24: 22.1%), but this relies on a heavily adjusted profit figure.

Reported operating profit is markedly lower at just £22.7m, giving an 8% operating margin.

The vast majority of this adjustment relates to a £34.8m charge for the amortisation of acquired intangible assets. Rather than getting bogged down in a debate over the merits of this approach (which I dislike), I’ve turned to the free cash flow statement to see how much surplus cash GB actually generated last year.

The news is quite good, in my view. Free cash flow drops out at £41.6m by my calculations, midway between the group’s reported and adjusted measures of profit. This explains last year’s big reduction in net debt and gives rise to some potentially attractive metrics, in my view:

FCF margin (vs revenue): 14.7%

FCF yield (vs share price): 6.8%

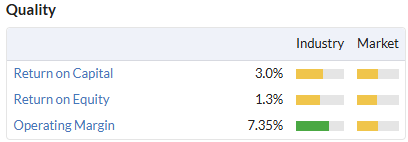

The main weakness here for me is that GB does not seem to be generating very attractive profits relative to the assets on its balance sheet.

My sums give the following return metrics for last year (adjusted/reported):

Return on equity: 7.3% / 1.4%

Return on capital employed: 9.5% / 3.2%

These measures are similar to the quality metrics shown on the StockReport:

Even using adjusted profit, these profitability measures do not seem very high for a software group that claims a strong competitive positioning and boasts numerous high-profile customers for its identify and location services:

Outlook: management guidance unchanged, but there is expected to be an H2 bias to growth to reflect the strong performance in H1 last year:

The new financial year has begun as expected and our outlook for the full year is consistent with current market expectations. Given the relative strength of the first half of FY25, our FY26 growth in constant currency terms will naturally be second half weighted.

Exchange rates are also expected to be a headwind this year, albeit the company says the majority of this impact is already reflected in market expectations.

I don’t have access to any updated broker notes for GB.

However, Stockopedia’s consensus figures ahead of today’s results suggested that adjusted earnings could rise by 5% to 18.3 per share this year. Assuming this consensus remains unchanged, this puts GB on a forward P/E of 13.5 after this morning’s drop.

One point worth noting is that expected growth this year narrowed sharply following April’s trading statement – analysts appear to have raised forecasts for FY25 but cut them for FY26:

Roland’s view

I would not be entirely surprised if consensus expectations edged slightly lower after today’s results. But I think the broad picture here could still be of interest.

My reading of the low returns being generated by this business is that they result from past acquisitions, perhaps in particular the £305m acquisition of Acuant in 2021. As a result of this and other deals, the balance sheet carries £550m of goodwill.

I’m not sure that current profits justify the past spending implied by this level of goodwill. However, this is in the past now. If management can resist any further expensive acquisitions, I think GB’s underlying profitability could potentially be attractive at the current valuation.

In my view, the missing ingredient that would be needed to support a share price recovery is stronger revenue growth. Consensus forecasts seem to suggest the top line will remain broadly flat again this year, unfortunately.

Without stronger evidence of momentum, I can’t take a fully positive view. But I’m going to maintain Graham’s previous AMBER/GREEN view today and will continue to watch GB’s progress with interest.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.