Good morning and welcome to today's report.

The agenda is complete.

Mello 2025: just a quick reminder that this fantastic investor conference is getting underway in London today. Ed, Graham & Mark will be there as will many of the companies we report on in these pages. I believe a few tickets may still be available - we are able to offer a discount code "STOCKOPEDIA50", which can be used at this link.

Warren Buffett's evolving style: finding our own style as investors can be a key element of success. Alex has published an interesting new article today charting the evolution of Warren Buffett's style over his career as an investor - it's well worth a read.

14:20: we're wrapping up the report for today - see you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

British American Tobacco (LON:BATS) (£73.5bn) |

On track for FY25, revenue slightly ahead of guidance, exp FY rev +1-2%, adj op profit +1.5-2.5%. | AMBER/GREEN (Roland) [no section below] | |

Rotork (LON:ROR) (£2.6bn) | Commenced buyback programme up to £50m. | ||

Pennon (LON:PNN) (£2.4bn) | Rev +15%, adj EBITDA flat at £335.6m. Adj LBT of £35.1m. Outlook: return to profitability. | ||

Chemring (LON:CHG) (£1.3bn) | Rev +5%, adj PBT +6% to £24.1m. Record order book of £1.3bn, outlook in line w/ exps. | AMBER (Roland) Today’s results from this defence contractor look solid enough and show very strong growth in the order backlog. However, much of this seems to be being driven by Energetics, with weakness elsewhere in the business. This situation may improve in H2, but I can’t help feeling that a fair amount of growth is now priced in here, so I’m going to maintain our neutral view. | |

Spirent Communications (LON:SPT) (£1.1bn) | Acquirer Keysight has entered an agreement with the DoJ to spin out Spirent’s ethernet channel prior to acquisition. | PINK (under offer) | |

Dalata Hotel (LON:DAL) (£1.0bn) | Possible cash offer of €1.3bn or €6.05 per share. | PINK | |

Kier (LON:KIE) (£756m) | Trading in line, order book +2% at £11bn w/ 80% secured for FY26. The group’s target operating margin for 3-5 years from now has been increased to 4.0-4.5%, from 3.5%+ previously (FY24 actual: 3.4%). Targets for month-end net cash and 3x dividend cover through the cycle are unchanged. | AMBER (Roland - I hold) [no section below] Management says that improved bidding discipline and risk management has improved the quality of the order book, which should support higher margins in the future. A number of recent infrastructure project wins are mentioned, as is improved performance from the group’s property development business. There doesn’t seem to be much top-line growth here, with the order book flat on H1 and only 2% higher than at the end of FY24. However, if Kier can improve its profitability this should feed through to the bottom line and perhaps reduce the risk of future problems. Kier is a member of the SIF folio so I’m pleased by today’s update. But I’m going to maintain our neutral view as this is an in-line update and the promised margin improvement is not expected for at least 3 years. | |

FD Technologies (LON:FDP) (£538m) | Rev +2%, adj LBT of £29.1m. Net cash £55m. KX trading ahead of exps. FY26 exp ARR growth >20% | PINK (under offer) | |

Newriver Reit (LON:NRR) (£379m) | Net property income +10.5% to £50.4m, dividend -1.5% at 6.5p. NAVps -11% to 102p. LTV 42.3%. | ||

MJ GLEESON (LON:GLE) (£301m) | PW: FY op profit to be 15-20% below exps due to lower gross margins and a failed land transaction.

FY26 gross margin is now also expected to be c.1% below previous exps. Singer Cap EPS forecasts: FY25E cut by 20% to 28.7p per share. | BLACK (AMBER/RED) (Roland) | |

Gateley (Holdings) (LON:GTLY) (£173m) | Rev +4% to >£179m, adj PBT exp “broadly in line” with consensus. Notes lower interest income. | AMBER (Megan) It’s a short statement and the word “broadly” worries me slightly in the company’s comment on trading compared to consensus. The shares look decent value, but not quite cheap enough. | |

Eleco (LON:ELCO) (£136m) | Trading in line with expectations. Resilient underlying demand for product. | ||

Gooch & Housego (LON:GHH) (£129m) | H1 revenues +7.5% on an organic basis to £71m. Improved op margins. Unchanged full year expectations, but pipeline execution risk higher in H2 owing to macro headwinds. | AMBER (Megan) Demand is strong in two of the company’s three operating divisions, but so is competition. GHH has had to cut prices and is seemingly offering more favourable sales terms in order to battle the competition. There isn’t an awful lot of reassurance in these numbers. | |

Pebble (LON:PEBB) (£70m) | Trading in line with expectations although cautious about US tariffs and wider macro-economic headwinds. Remaining £2.4m of previously announced buyback programme to be replaced with a £6.5m tender offer. | ||

Inspecs (LON:SPEC) (£55m) | US tariff uncertainty impacting group sales. Revenue in the full year now expected to be flat, profit guidance unchanged. Founder stepping down as chairman. | ||

Maintel Holdings (LON:MAI) (£34m) | Macroeconomic headwinds means sales momentum had a slower than expected start to the year. Full year results now expected to be second half weighted. | ||

Renalytix (LON:RENX) (£24m) | Collaboration with New York Kidney and Hypertension Medicine | Partnership to expand access to Renalytix prognostic test for chronic kidney disease. | |

tinyBuild (LON:TBLD) (£22m) | Sales slightly ahead of expectations for the first five months of the year. Strong pipeline of new games with release schedule weighted to H2. | ||

Chesterfield Special Cylinders Holdings (LON:CSC) (£15m) | The first set of results from the newly streamlined business formerly known as Pressure Technologies. Revenues in the remaining cylinder producing division -17% to £5.4m. Adjusted op loss -£1.7m. | ||

Sundae Bar (LON:SBAR) | Sundae Bar is a company creating a marketplace for AI Agents. It begins trading on AIM today. |

Backlog items: ADF

Megan's Section:

Gooch & Housego (LON:GHH)

Unchanged at 499p (£129m) - Interim Results - Megan - AMBER

The headline numbers from photonics group Gooch & Housego are decent, but digging into the detail reveals that investors are right to be cautious about the group’s ‘recovery’.

Starting with the headline positives.

Demand for photonics engineering is high across at least two of the three industries that G&H specialises. We don’t cover the company a lot in the daily report, so for those of you who aren’t sure, photonic engineering involves the manipulation of light for communication purposes. G&H designs and manufactures the camera and other optical equipment needed for this sort of thing.

It’s increasingly important in aerospace engineering and in modern defence systems. Aerospace and defence contributes a third of G&H revenue and grew 30% on an organic basis in the first half.

Demand is also strong in the life sciences space (24% of total sales). The company reported a 14% increase in the division’s like-for-like sales thanks largely to a big order by one customer.

In the company’s largest division (industrials), like-for-like revenues dropped 6.5% to £30.1m as the semiconductor industry remained subdued. Still the division is benefiting from a surge in demand for more complex fibre optic cable networks in industries like subsea data. These more complex products come with higher margins which sent the division’s operating profit up 10% to £3.8m.

Overall, company sales were 11.4% higher at £71m, or 7.5% higher on a like-for-like basis compared to the first half of FY24. Adjusted pre-tax profits (after stripping out amortisation and non-recurring items) rose 91% to £5.1m.

But challenges remain, most notably in the fact that G&H is not the only company attempting to take advantage of the higher demand for photonics equipment in defence and life sciences. In the former, the company is only just profitable and in the latter it remains loss making. Management has said in the past that it is wary of low-cost competition and this continued to be a problem in the first half of 2025, forcing the company to undercut its prices.

G&H also seems to be having to offer more favourable terms regarding the payment of goods sold. Receivables were £6m higher at £37m - equivalent to more than 50% of total sales booked in the period. Management says that this higher level of receivables was due to higher invoicing in March and the cash for those sales has been collected since the period end, but it’s still not a particularly reassuring number.

Megan’s view:

There has been some recovery in the share price in the last few months, after management said that the company might be a net beneficiary of disruption caused by Donald Trump’s US tariffs. The thinking being that the additional costs would have a bigger impact on the company’s competitors than on G&H itself.

But that recent surge doesn’t yet mark a sustained turnaround after a difficult few years. The trouble is that this high tech company shouldn’t really have a problem with competitors and margins as it should benefit from high barriers to entry. But that isn’t the case. Operating margins have averaged just over 4% in the last five years with ROCE just 3.6%.

I’m happy to retain our previous view of a disinterested AMBER.

Gateley (Holdings) (LON:GTLY)

Down 2% to 127p (£171m) - Trading Update - Megan - AMBER

There are a few things that I don’t really like about the outlook statement from Gately within this morning’s trading update:

The Group's underlying PBT* for the period is expected to be broadly in line with market consensus**

The first is the need for two lots of caveats which require the reader to scroll to the bottom of the statement for clarification.

Underlying PBT has a lot of elements stripped out of it and some of those aren’t especially clear. ‘Post-combination services’, for example, refers to sales booked after acquisition and ‘exceptional items’ aren’t defined.

Those consensus estimates are for revenue of £184m and adjusted PBT of £24m, “based on the latest published equity research”. Those figures could probably have been included in the original sentence.

The second thing about the outlook sentence which is vaguely troubling is the use of the term “broadly”. That doesn’t instil a huge amount of confidence given management has also pointed out that lower interest rates have had a negative impact on interest income.

Gately, which was the first law firm to list on the UK markets back in 2015, but has since diversified into a more general ‘professional services’ group, has attempted to deliver returns to shareholders and staff through acquisitions and diversification.

Paul pointed out on several occasions that these types of ‘people’ businesses can be problematic because of conflicting interests between the fee earners and shareholders. That holds true in this statement which reveals the company has moved into a net debt position in order to set up an employee benefit trust, which will help incentivise senior staff.

Megan’s view:

Gately was quite an exciting prospect when it listed in 2015 and early investors enjoyed decent returns in the first few years. But during the pandemic the share price dropped off a cliff and although it looked like there could be some value in the price, a recovery has never managed to materialise.

A PE ratio of less than 10 is tempting. As is the dividend, which is yielding 7.4% at the time of writing. But I’d be more inclined to wait for a spark which could signal a bit more meaningful growth so I will remain neutral. AMBER

Roland's Section:

MJ GLEESON (LON:GLE)

Down 20% to 410p (£240m) - Trading Update - Roland - BLACK (AMBER/RED)

Unfortunately it’s a big profit warning from this affordable housebuilder this morning - Gleeson's management now expects profits for the year ending 30 June 2025 to be significantly lower than previously expected:

Gleeson Homes anticipates reporting an operating profit circa 15% - 20% below current expectations.

Today’s update is quite short, but the warning on profits contains a number of elements that have combined to cut expectations for not just FY25, but also FY26 and FY27.

Cost headwinds & weak market conditions: the company says that build costs have continued to increase during the year while selling prices have remained flat. Management also flags up the continued use of incentives (i.e. discounts in disguise) and “several bulk sale transactions”.

The end result was that these conditions are expected to result in a gross margin c.1% lower than expected.

Land sale not proceeding: it looks like management had hoped to offset this weakness with profits from a large land sale in East Yorkshire, where Gleeson has “extensive land holdings”. This sale is no longer expected to proceed. As a result, FY25 operating profit is expected to be 15-20% below expectations.

FY26 outlook: planning delays during the current year will mean that Gleeson will be selling from fewer sites than previously forecast in FY26. Cost and price pressures mentioned above also mean that FY26 gross margin is expected to be c.1% below market expectations.

Gleeson Land: the group’s land division has completed three transactions so far this year and is working on seven disposals that are “anticipated to complete before the year end”.

Checking back to the interim results, previous guidance was for “four to eight site sales in H2”. Timing of completions is difficult to predict with land sales. I would speculate that there’s some risk that not all of these seven remaining sales will complete in the next 27 days. I don't know how many sales are factored into today's revised expectations, but I'd guess that there could be some variation in the FY25 outcome depending on progress in this area.

Updated Estimates: with thanks to house broker Singer Capital we have access to updated forecasts this morning. Unfortunately, Singer’s analysts have cut their estimates for FY25 through FY27:

FY25E EPS -20% to 28.7p

FY26E EPS -19% to 33.6p

FY27E EPS -18% to 41.1p

For context, previous consensus earnings estimates on Stockopedia were 35p (FY25) and 40.4p (FY26).

Roland’s view

When Gleeson issued its half-year results in February, the tone of the company’s commentary seemed relatively upbeat, reporting a 4.8% increase in average selling prices and “encouraging signs of a recovery in demand”.

Graham took a positive view, noting that falling interest rates and a reduction in build cost inflation (only 1% for GLE in H1) could provide a tailwind for profits.

The tone of today’s update seems notably more downbeat to me. While the failure of the expected large land sale in East Yorkshire may be a one-off issue with no wider significance, issues that seemed to be improving in H1 are now being put forward as headwinds that are holding back margins.

It looks to me like conditions in Gleeson’s markets may have weakened since February. For example, at the end of H1 the company said this about incentives and selling prices:

As market conditions improve, we anticipate there will be opportunities to reduce the level of discounts and incentives offered, whilst continuing to selectively increase prices.

Today’s update refers to “flat selling prices” and “continued use of incentives and several bulk sale transactions”.

One possibility I can see is that the benefits from falling interest rates and slowing inflation are taking longer to feed through to Gleeson’s core customer base in the North of England and Midlands. The company’s focus on affordable housing means it targets less affluent customers. These would-be buyers’ personal finances may not yet have recovered from the cost-of-living inflation seen over the last few years.

This morning’s fall has left Gleeson shares trading around 20% below their last reported book value of 509p. On a medium-term view I can see some value at this level, but for now I’d argue that this seems about right. My sums suggest Gleeson’s full-year return on equity is likely to be around 6%, similar to the last couple of years:

If the company can hit revised forecasts, I think ROE should trend back towards double digits over the next 18-24 months. In that scenario, I’d also expect the shares to trade at or slightly above book value.

I’m going to downgrade our view to AMBER/RED today to reflect today’s profit warning and the risk of further disappointments – for example, if hoped-for land sales don’t complete by the end of June. However, I think it's fair to say that if external conditions improve, expectations could also be revised upwards over the next 12-18 months.

Chemring (LON:CHG)

Up 8% to 525p (£1.4bn) - Interim Results - Roland - AMBER

Record order book, full year expectations unchanged, strong long-term prospects

Defence sector: the UK government released the results of its strategic defence review yesterday. Plans include building more submarines, expanding the army’s electronic warfare capabilities and maintaining much larger stocks of ammunition – the latter two are key lessons from the Ukraine war.

Against this backdrop, bullish investor sentiment towards FTSE 250 defence contractor Chemring is not surprising. This firm specialises in technology used in areas such as electronic and cyber warfare, ammunition and countermeasures. The business seems likely to benefit from higher volumes in the future – indeed, these interim results show growth in demand for some (but not all) of its markets already.

However, these strategic reviews don’t always translate into concrete long-term spending proposals required to persuade private sector contractors to deploy significant new capital to support growth. Persuading the MoD to adopt new technologies and secure their place in long-term budgets is reportedly not always easy either (FT paywall).

Another concern for UK contractors with heavy US exposure (including Chemring - c.30% of revenue) are also still waiting for the outcome of the current US defence spending review. The outcome of this seems hard to predict. Chemring’s FTSE 250 peer QinetiQ has already warned on profits this year due to changing US spending patterns under the current administration.

Chemring shareholders have enjoyed strong gains over the last year, but with the stock now trading on 25x FY25 forecast earnings and guidance unchanged today, I wonder if the situation for potential buyers is perhaps not as clear-cut as it was:

Let’s take a look at today’s results.

H1 results summary: Chemring has an unusual 31 October year end, so today’s half-year figures cover the six months to 30 April 2025.

Headline figures are positive although bottom line growth is not exactly explosive:

Revenue up 5% to £234.3m

Underlying pre-tax profit up 6% to £24.1m

Underlying earnings per share up 3% to 6.8p

Net debt up 24% to £93.3m

The increase in net debt gives us a useful clue as to what’s happening; Chemring, at least, has decided to commit new capital to upgrade and expand its manufacturing capabilities. This seems to be supported by very strong order intake:

H1 order intake +42% to £488.0m

Order book up 25% to £1,303.8m

However, today’s segmental results highlight some of the uncertainties I mentioned above and reveal a very uneven performance across Chemring’s operations so far this year:

Countermeasures & Energetics: revenue up 20% to £141.7m, op profit +73% to £20.4m

Sensors & Information: revenue down 12% to £92.6m, op profit down 26% to £16.1m

Countermeasures & Energetics: order intake rose by 68% to £418m, “with multi-year orders received across this sector”.

This division covers a number of operations in the UK and elsewhere. Energetics includes products such as explosives and propellants for use in artillery rounds and missiles. This business is driving much of Chemring’s growth at the moment as government customers increase stockpiles of ammunition.

Sensors & Information: order intake fell by 27% to £70m during the half year and management says that growth in this business, which includes Roke, was held back by delays caused by the UK’s strategic defence review:

whilst we have seen no evidence of Roke programmes either being lost or cancelled, the rate of new order placement has slowed and there has been an increase in project extensions.

The company says that an “upturn in demand” is expected during the second half of the year. But they also comment that Roke’s cost base was right-sized during the period, with c.50 redundancies. This makes me wonder just how quickly a recovery is expected.

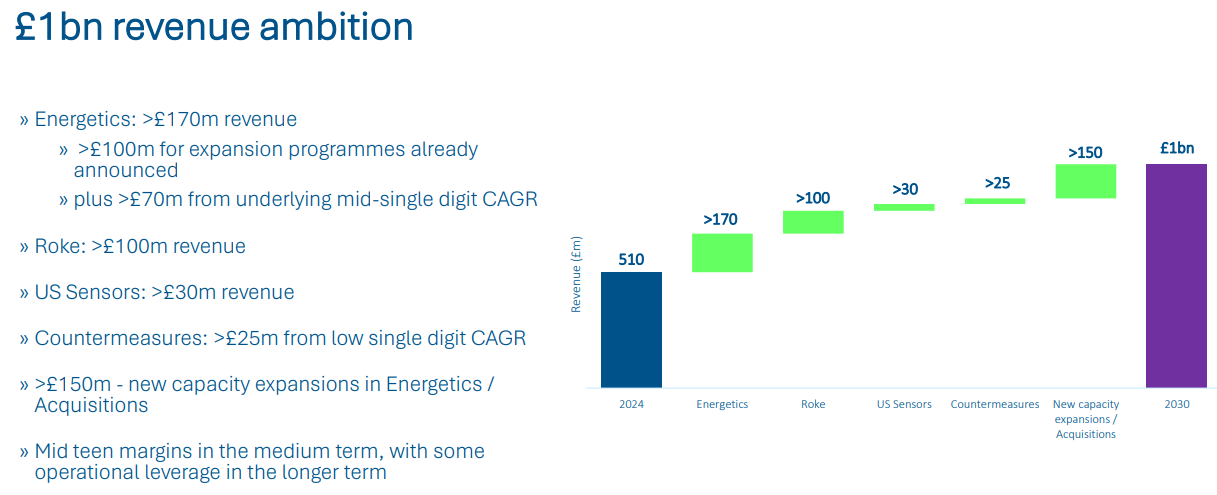

Growth plans: in today’s results presentation, the company says it’s targeting £1bn in annual revenue by 2030, which would mean doubling in size relative to last year’s revenue figure of £510m. The company expects to drive much of this growth with its Energetics business:

A £200m investment programme was announced in 2023 to support Energetics growth. Chemring is contributing £110m, having secured £90m of grant income in Norway.

Management expects this spending to generate £100m of additional revenue and £30m of additional operating profit by 2028. If so, that would represent a healthy 15% return on capital employed, above the company’s current run rate.

Today’s results also note that yesterday’s defence review could support permanently higher spending on munitions:

The SDR also commits to investing £1.5 billion in an "always on" pipeline for munitions and building at least six new factories in the UK to produce munitions and energetics, which are key components of weapons, including propellants, explosives, and pyrotechnics. It also commits to building up to 7,000 UK-built long-range weapons to strengthen Britain's Armed Forces. The Group is well placed to benefit from these opportunities.

Outlook: Chemring says that its order backlog at the end of April provided 85% coverage of expected 2025 revenue. This is lower than the equivalent figure of 93% of H2 revenue provided last year.

I recognise that some of the company’s products are on fairly short order cycles, but I guess I might have expected order coverage to be slightly stronger than this, given the size of the company’s backlog.

This situation suggests to me that some of the existing backlog may reflect capacity constraints on current production, particularly in Energetics. Elsewhere in the business, utilisation may be weaker. Comments about Roke seem to support this view.

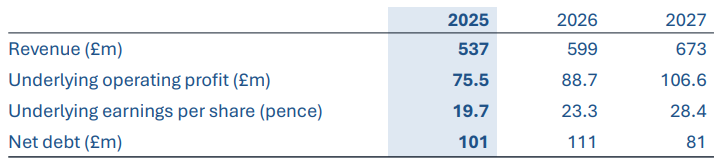

Overall expectations for the full year are unchanged today. Chemring has helpfully included its view of current market consensus for FY25 through FY27 in today’s presentation:

These figures are very close to the consensus estimates shown in Stockopedia, giving us a FY25E P/E 26.6 and FY26E P/E of 22.5 after this morning’s share price gain.

Roland’s view

Chemring appears to be in a strong position currently to benefit from higher volumes for some of its core products. At this stage, I have no real reason to doubt the company’s expectations for a recovery in Roke and other areas where performance has been weaker.

The company’s growth plans seem to be supported by material levels of investment and plans for further acquisitions; the £1bn revenue target doesn’t seem implausible to me.

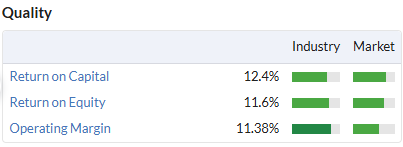

However, I think it’s worth noting that Chemring’s quality metrics highlight fairly average levels of profitability:

Today’s underlying results are consistent with these margins. Net debt rose to just under 1.0x EBITDA during H1. That’s not a concern in itself, in my view, but it’s worth considering that companies with relatively average profitability are less able to self-fund growth and may need to rely more heavily on debt.

Another consideration for me is that acquisitions made in the current environment could be expensive, a view highlighted in Chemring’s own StockRank:

From a value perspective, I think Chemring’s share price looks up with events at the moment. At the same time, I’m not convinced the company’s quality metrics are strong enough to justify viewing this as a high-quality business.

Momentum has been very strong, but the StockReport highlights that recent price gains have been achieved on falling volumes:

I’m finding it difficult to choose between AMBER and AMBER/GREEN following today’s results.

My concern is that the good news is already in the price and that Chemring now needs to actually deliver the promised growth. On the other hand, if structural changes in defence spending become entrenched, it’s not hard to see this business becoming permanently larger and perhaps more profitable.

On balance I’m going to maintain our previous neutral view today, at the risk of possibly missing a longer-term opportunity. AMBER.

Backlog

Facilities by ADF (LON:ADF)

Down 3% to 15.5p - Notice of AGM & Update re. Proposed Dividend - Mark - AMBER/RED

This is more than what the RNS title says and includes a trading update:

Trading in the current financial year remains in line with market expectations with activity levels expected to be weighted to the second half. The Board continues to expect the Company to be cash generative in the year ending 31 December 2025 ("FY25") with closing cash balances anticipated to be in line with current market expectations.

We may have been able to guess the second half weighting from the comments in the Final Results statement. However, this appears to be the first time they have been explicit about this. Second-half weightings are sometimes precursors to profit warnings, of course, and the market rarely likes this uncertainty.

The other news is that the originally planned 0.9p final dividend has been reduced to 0.5p. They say they discussed it with shareholders holding over 40% of the issued share capital. Which, looking at the shareholder register, suggests BGF, Harwood and at least one of the others:

To be fair, it did look a little foolhardy to maintain the dividend for a period where they also announced an increase in net debt:

Net debt, excluding IFRS 16 leases at the end of FY24 was £13.8 million (FY23: £12.8 million). Hire purchase liabilities reduced from £16.3 million at the end of FY23 to £16.2 million at the end of FY24, and cash reduced from £3.6 million to £2.4 million.

…liquidity metrics look like this:

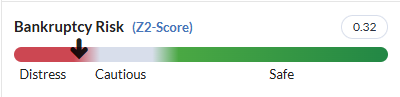

…and the Stock Report flagged the company as in distress:

I’d imagine that as part of the discussions, major shareholders will have given an assurance that they would support the company if it needed a capital raise. However, that doesn’t preclude them from extracting their pound of flesh!

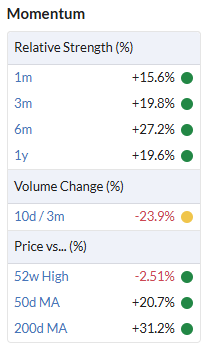

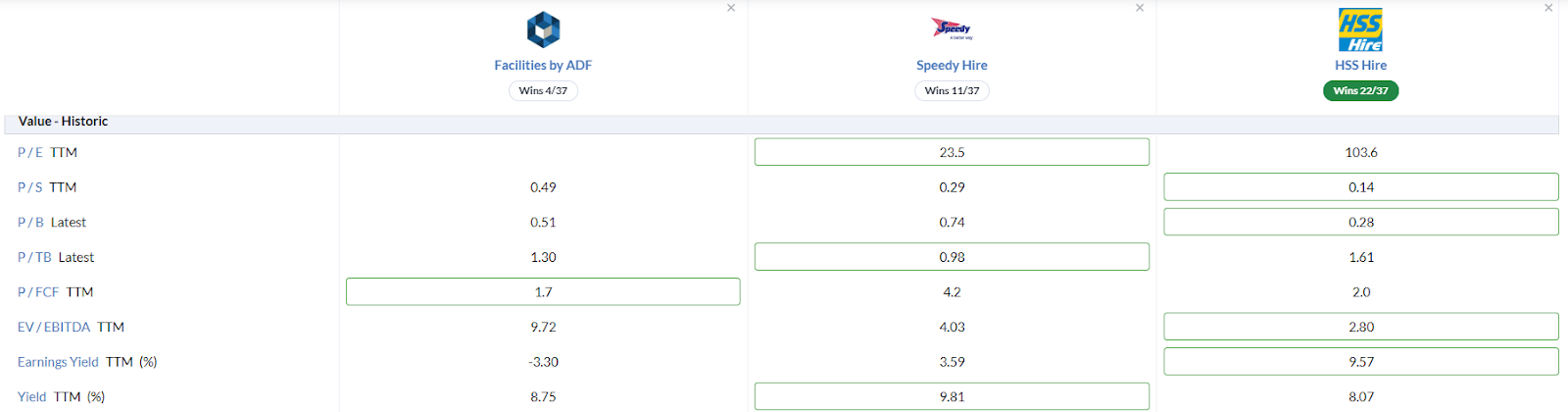

It also strikes me that this is really a small specialist plant hire company, and while that specialism can mean higher margins, it hasn’t helped profitability here recently. On a valuation front, I think this should be compared to other small listed plant hire companies. So far, despite big falls over the last year and a Momentum Rank of just 4, this comparison looks unfavourable:

Mark’s View

This company doesn’t look particularly cheap on any value metric apart from yield, and this has been downgraded materially in this announcement. Typically, in downturns, plant hire companies can just cut capex to generate cash. The company has certainly cut capex, but has also increased leased assets and acquired another business, leaving their debt looking high. Cutting the dividend seems a sensible thing to do in such a scenario, but that doesn’t improve the investment case, which remains at the AMBER/RED level, in my opinion.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.