I have been investing for more years than I care to admit but I suspect like many find the current market in UK small caps shares especially torrid and difficult to navigate.

My investment approach could be described as value orientated and to an extent long term. I will generally sell a holding if:

- I think it has become overvalued.

- Management depart from their original script.

- On a profit warning.

- Where I screwed up and didn't do sufficient research. A recent example being Synthomer (LON:SYNT), where I sold for a 30% loss

Having learned from early painful experience I avoid companies which are overly indebted or in my view over hyped. In large part I try to adhere to Peter Lynch's mantra of avoiding the hottest stocks in the hottest markets and buying shares in companies that I understand. Occasionally I have strayed outside my self imposed rules and such forays as might be anticipated usually 'end in tears'. Hence I have never owned shares in Novacyt Sa (LON:NCYT), Tesla, Netflix or companies involved in fashion retail, the exception being Next (LON:NXT) . I fully appreciate that many subscribers have and to an extent successfully done so.

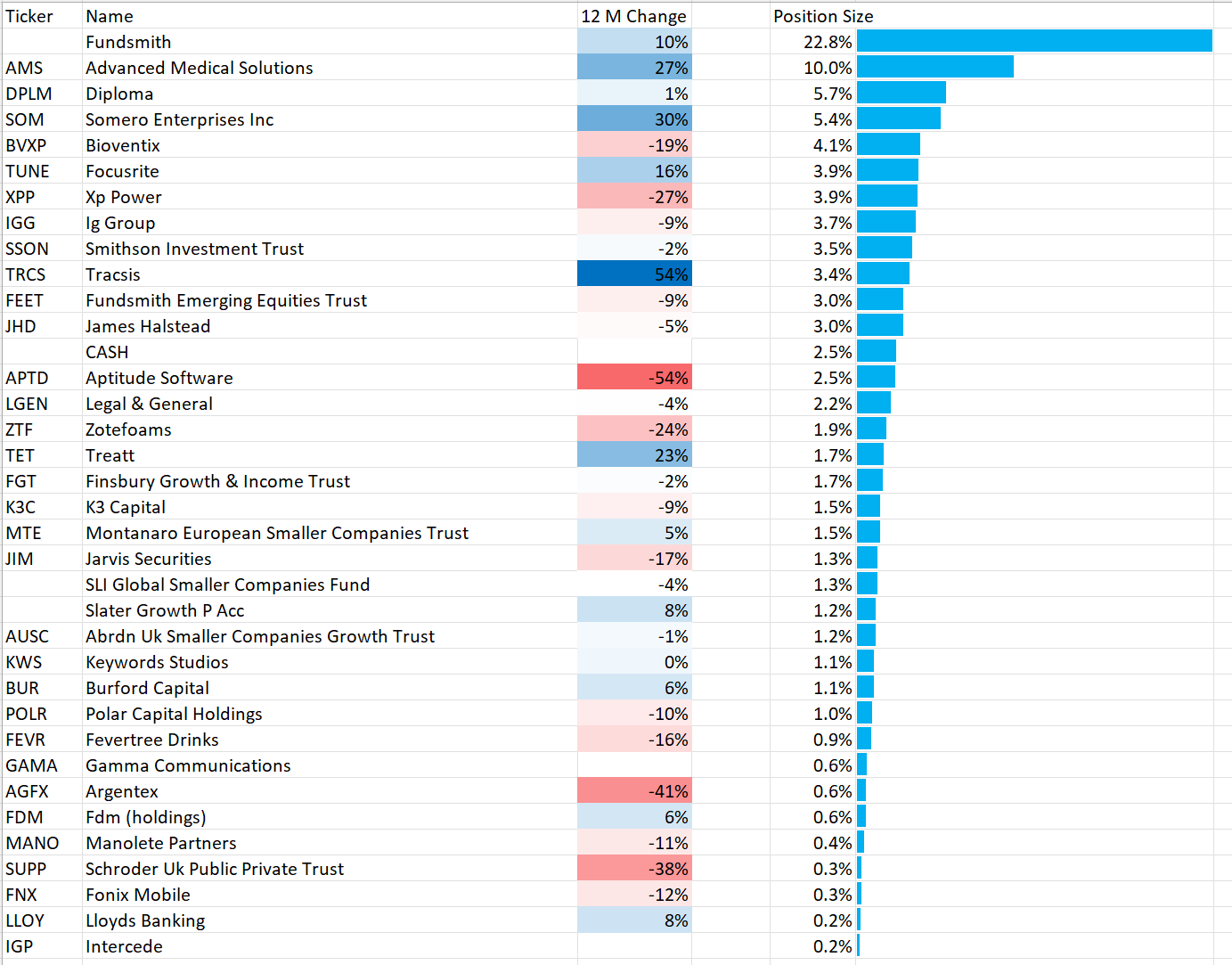

Anyway the aim of this post is to try get a flavour of where other Stockopedia members have recently been investing during the current market turmoil. For my part I have added to the following holdings:

Smiths News (LON:SNWS) because the management has so far done everything it said it would in the turnaround of the company. It has disposed of its pension scheme, debt has been refinanced and reduced. Free cash flow is excellent, PE sub 4, yield 6% plus. Management currently looking at ways it can use its distribution expertise to add other revenue streams. It is difficult to believe that private equity has not run the rule over the company given the predictable free cash flow.

Headlam (LON:HEAD) because of its balance sheet strength, self help measures such as rationalising its distribution network, including transport systems and recent positive trading update. It has a clear strategy for increasing revenue by targeting parts of the market where it is under-represented such large retailers and house builders and a goal of increasing operating margins from 5% + to 7.5%.

Bloomsbury Publishing (LON:BMY) for reasons given in my post of 6th January in…