Recently, as regular readers will probably have noticed, I've been taking a subtly changed sort of approach in my blog posts. Most of this comes down to red, whose approach I have shamelessly plagiarised in the pursuit of self-improvement and better stock picking. There hasn't been a monumental shift in the way I discuss things - there never was going to be - but there is a change of direction in how I calculate and appraise investments on my end. In the simplest terms, I've just been shown a much better way of trying to put abstract concepts into numbers. Check out his blog if you want a far more nuanced and less clumsy explanation/application of his way of calculating 'value', but I'll bludgeon a simplistic version of it in four bullets here, with the proviso that any glaring oversights are entirely a result of my own misinterpretations:

Recently, as regular readers will probably have noticed, I've been taking a subtly changed sort of approach in my blog posts. Most of this comes down to red, whose approach I have shamelessly plagiarised in the pursuit of self-improvement and better stock picking. There hasn't been a monumental shift in the way I discuss things - there never was going to be - but there is a change of direction in how I calculate and appraise investments on my end. In the simplest terms, I've just been shown a much better way of trying to put abstract concepts into numbers. Check out his blog if you want a far more nuanced and less clumsy explanation/application of his way of calculating 'value', but I'll bludgeon a simplistic version of it in four bullets here, with the proviso that any glaring oversights are entirely a result of my own misinterpretations:

- Look at history to come up with a reason cycle-average returns figure for the company in question, making sure to adjust for accounting quirks, exceptionals (?) etc.

- Come up with an operating capital figure. This takes into account leases, your calculation of working capital, and PPE in use.

- You now have a realistic adjusted return on capital figure to compare to a reasonable estimate of cost of capital. The comparison of these two figures is informative - the directionality and size of the gap guides further research.

- Given an assets figure and a return vs. CoC figure, you can calculate the value of the cashflow sans growth. After you adjust for debt/debt-equivalents and tax effects, you have a value figure for the business to compare to the market cap.

Similar to how the DuPont formula guides our analysis of returns - it helps us breakdown the causative factors of a change in returns by splitting a complex figure into easier chunks - by coming up with a value figure with logical and intuitive steps, we can more easily see how things might potentially change. It strikes me as sort of like a DCF, only with the focus on the inputs instead of the outputs.

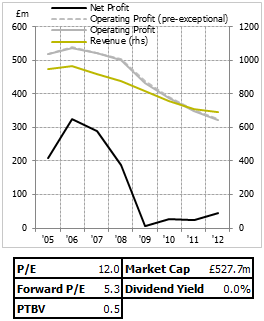

That introduction is important, because it frames my discussion of Enterprise Inns nicely.

The background

Enterprise Inns (LON:ETI) is a pub group - the largest leased and tenanted pub group in the UK,…

.png)