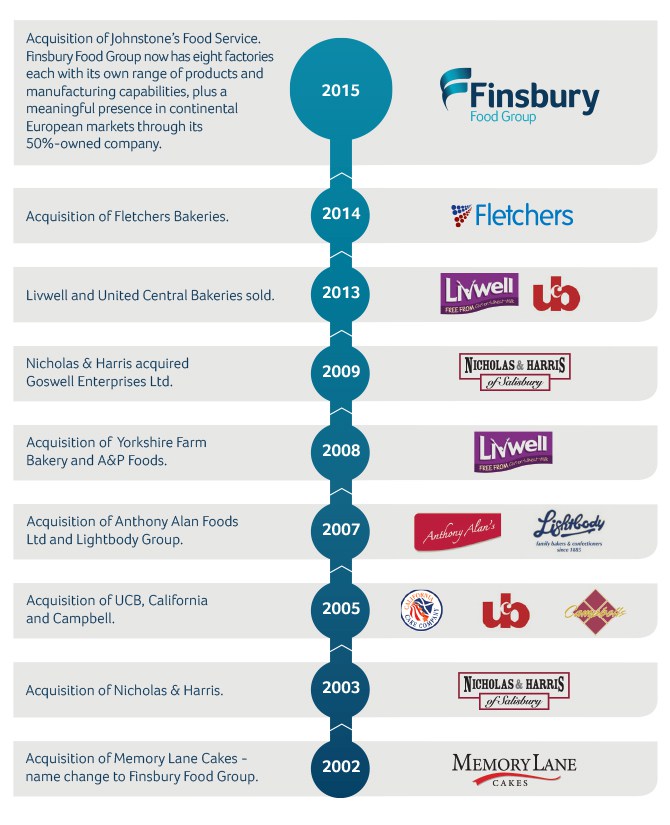

What is Finsbury Food Group?

The company is made up of five divisions, which includes:

1. Foodservices; - The brands involved are Kara and the newly acquired Johnstone’s. Both make special treats and premium snacks for coffee chains, hotels, pubs and fast food outlets in the domestic and international market.

2. Licensed Brands (most significant segment); - Finsbury Food got licenses to manufacture cakes and bread for some of these well-known brands such as Disney, Weight Watchers, Vogel, Thornton, Village Bakery and Cranks.

3. International; - It owns 50% of Lightbody Stetz, which helps distribute its manufactured products, particularly in France.

However, in 2014 it acquired Fletchers Group (a rival bakery business) for £56m that would double the size of Finsbury. This is paid for by raising £35m in equity.

By the time Finsbury report its result on 19th September, revenue (as mentioned in a trading update) would exceed £300m.

The question is how much it will make in earnings?

Given the significant changes taking place for Finsbury Food it is wise not to go into depth on the fundamentals but make observations.

The following are facts and figures on Finsbury Food:

Fact 1: - Revenue to reach £300m in annual turnover following the acquisition of Fletcher Group, compared to £110m in 2007.

Fact 2: - Current market capitalisation is £171m at £1.31/share; this grew from £0.25/share in the past five years.

The market likes the acquisitions and the objectives of management.

Fact 3: - Finsbury is now the second largest manufacturer in Morning Foods.

The company makes famous cakes like The Simpsons, Hello Kitty, Peppa Pig and Me to You.

Fact 4: - Finsbury made annual operating profits of £9.5m in 2015, but its interim results in 2016 jumped to £8m.

Also, operating margins increased to 5.1% in H1 2016, up from 4.2% in the previous period.

Extrapolating 5.1% on revenue of £315m would give predicted full-year earnings of £15.5m-£17m.

Net margin is 3.7% giving it projected earnings of £11.7m giving a PE of 14.

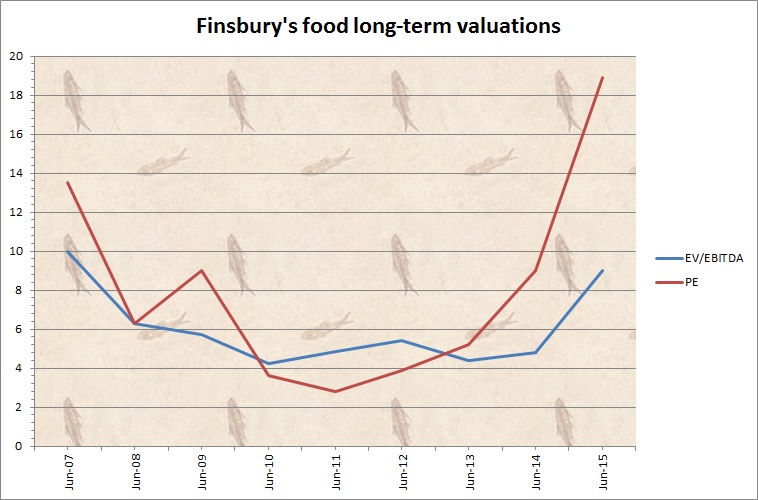

Fact 5: - Here is

the history of its valuation is displayed as follows:

Source: Finsbury Food Group annual reports (Created by the writer).

The high valuations of both graphs are lifting off at record highs.

But as I explain later, this is somewhat misleading.

Now, for my…..

Final thoughts

Despite, the five-bagger you…