Last week, I looked at some of the most interesting stocks from my Turnaround Screen. This week, I continue in the same vein with a first look at five more investment ideas for the turnaround investor.

Halfords (LON:HFD)

Many think of Halfords as a cycling retailer. However, their recent trading statement shows that they are increasingly a motor vehicle service centre operator:

The Group has two reporting segments: Autocentres (c.40% of Group revenue) and Retail (c.60%, across Motoring and Cycling). Motoring across both segments represents c.80% of total sales.

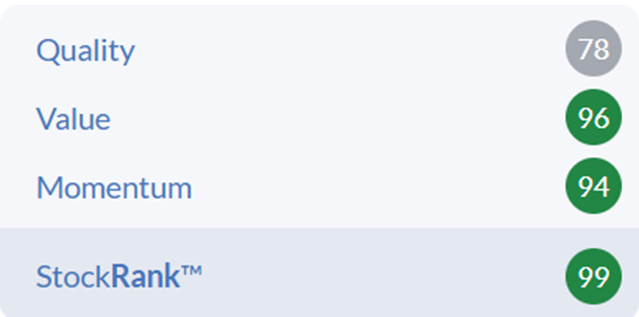

This is one of the highest VM-ranked stocks in the UK:

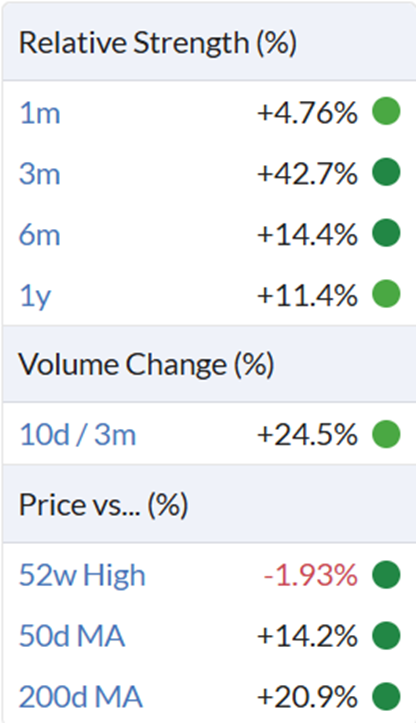

The Momentum Rank is driven by positive price moves across most timeframes:

There has been a strong recovery from April lows:

This is helped by an upbeat trading statement where they said:

Outperformed £30m cost saving target, mitigating more than £30m of inflation in the year.

Underlying Group profit before tax around the upper end of the £32m to £37m range previously guided.

However, the upgrades for future years have been very modest, and FY26 is now expected to be flat on FY25:

This makes it look expensive on forecast earnings. However, many of the other metrics are rated green, hence the high Value Rank:

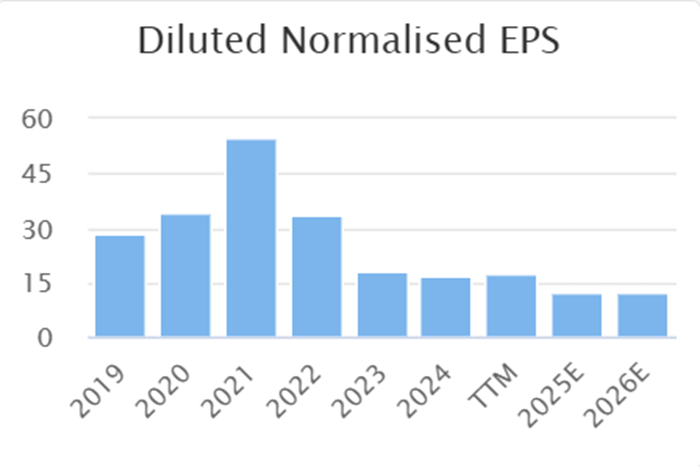

The EPS trend over the years isn't particularly promising:

Of course, 2020 and 2021 represented a cycling boom. However, in 2019 they did much higher EPS and they were forecast to get close to these levels in 2026 before downgrades last year. Like many retailers, the main issue seems to be around higher costs. They have plans to mitigate these, as they said in their recent trading statement:

We have previously communicated that the changes to the Minimum Wage and National Insurance thresholds and rates introduced by the Autumn Budget will result in c.£23m of incremental direct labour cost in FY26. We also expect increased costs to be passed through in contracts for managed services.

We have undertaken a comprehensive review of the business to identify potential mitigations for the additional…