Leading retail investor platform Hargreaves Lansdown (LON:HL.) has seen its growth slow in recent years, as a raft of newer and cheaper competitors have entered the market.

Relatively high prices and a lingering association with the Neil Woodford scandal may also be hindering sentiment towards the business.

However, while Hargreaves undoubtedly faces some near-term challenges, trading appears to be stabilising. April’s third-quarter trading update was good enough to trigger a round of broker upgrades.

Hargreaves’ historic DNA is as a low-cost innovator. Today the company is a hugely profitable market leader. If CEO Dan Olley can combine these strengths to rejuvenate the business, I believe the shares could be cheap on a medium-term view.

In the meantime, I think Hargreaves £500m net cash balance and well-supported 5.7% dividend yield should help to underpin the stock’s valuation.

Summary

Pros:

Market leader with near-40% share

Very strong profitability and good cash generation

Modest valuation if business can return to earnings growth

Cons:

May need to cut prices to become more competitive

Ongoing legal action relating to Woodford affair

Highly competitive marketplace, can HL attract new generations of investor?

Profile

About the stock

Hargreaves Lansdown is an investment platform serving the direct-to-consumer market. It’s classified in the Financials sector, within the Investment Banking & Investment Services industry group.

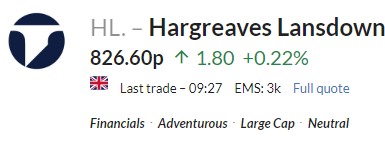

Hargreaves’ floated on the London market in 2007 and is currently a member of the FTSE 250, with a market cap of £3.9bn and a recent share price of 825p.

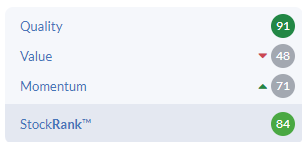

The StockRanks show a high quality score for Hargreaves Lansdown, but fairly average scores for value and momentum.

The stock’s overall style rating is Neutral. This suggests that while the business has some good qualities, it may be less likely to outperform in the near term than some higher-ranked companies.

About the opportunity

Hargreaves Lansdown is the market-leading DIY investment platform in the UK, with a market share of around 40%.

The company delivered an almost unbroken run of profit growth from its flotation in 2007 through to 2020. Profits then fell sharply through 2021 and 2022…