In this week’s Stock Pitch, I take a look at what looks like a small online travel agent - but in reality may be a very cheap social network contained within a successful online business.

Disclosure: at the time of publication, Graham has a long position in HSW.

Share price at the time of publication: 100.3p

Market cap: £125m

The Pitch

Hostelworld (LON:HSW) has a number of unique assets in the travel universe:

A focus on budget accommodation. This small niche, combined with its distinctive brand name, is the basis of its competitive moat.

A burgeoning social network uniquely suited to solo travellers, with over 3 million registered members.

A global event diary launching later this year.

The company was founded in 1999 in Ireland. It is credited with revolutionising the hostel industry by taking it online for the first time.

By 2009, it had been snapped up by a major private equity firm for c. €230m (£200m) - an impressive figure, especially when set against the company’s current market cap.

In 2015, it listed on the LSE. But its life as a listed company has been difficult, especially during the barren years of the Covid era.

It found itself over-leveraged, and the share price has been in the doldrums ever since:

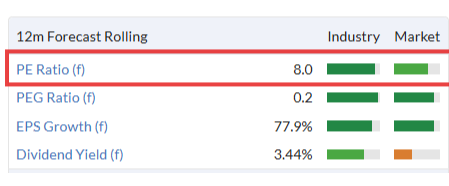

This lack of share price progress has seen the P/E multiple collapse to single digits:

How tough is the competition really?

Now you might argue: why take a chance on Hostelworld when shares in the highly reputable Booking Holdings (NSQ:BKNG) are available at 15x earnings? That sort of valuation is hardly prohibitive.

Indeed, Booking.com is an enormous competitor, and it too offers a very wide selection of hostels.

I randomly selected one night in Bangkok, in order to compare the offerings at each site. Booking.com actually offered more properties in the “Hostels” category than were available on Hostelworld.

However, the gap wasn’t huge (340 for Booking.com against 260 for Hostelworld), and an argument could be had around how many of Booking.com’s choices would truly qualify as hostels.

Whatever the truth of that may be, let’s take it as read that Booking.com is…