Individual share prices are astoundingly volatile. A useful practical measure of volatility is the difference between the high and low of a share's price over a twelve month period. Since September 2013 the average share on the London Stock Exchange has a high price more than double its low - yes more than double, 112% to be precise. When you consider the FTSE 350 index itself has only had a 14% range over the same period it's a massive difference.

Given this natural volatility, there's a serious risk to your wealth if you only bother to own a solitary stock. Most people take steps to sensibly diversify in order to reduce the chance of serious capital loss. But studies of brokerages show that the average investor only owns around 4 stocks in their portfolio. This extreme concentration suggests that many investors are either shooting for the moon or very poorly informed on the subject of diversification. So lets dive deep...

Just a few stocks...

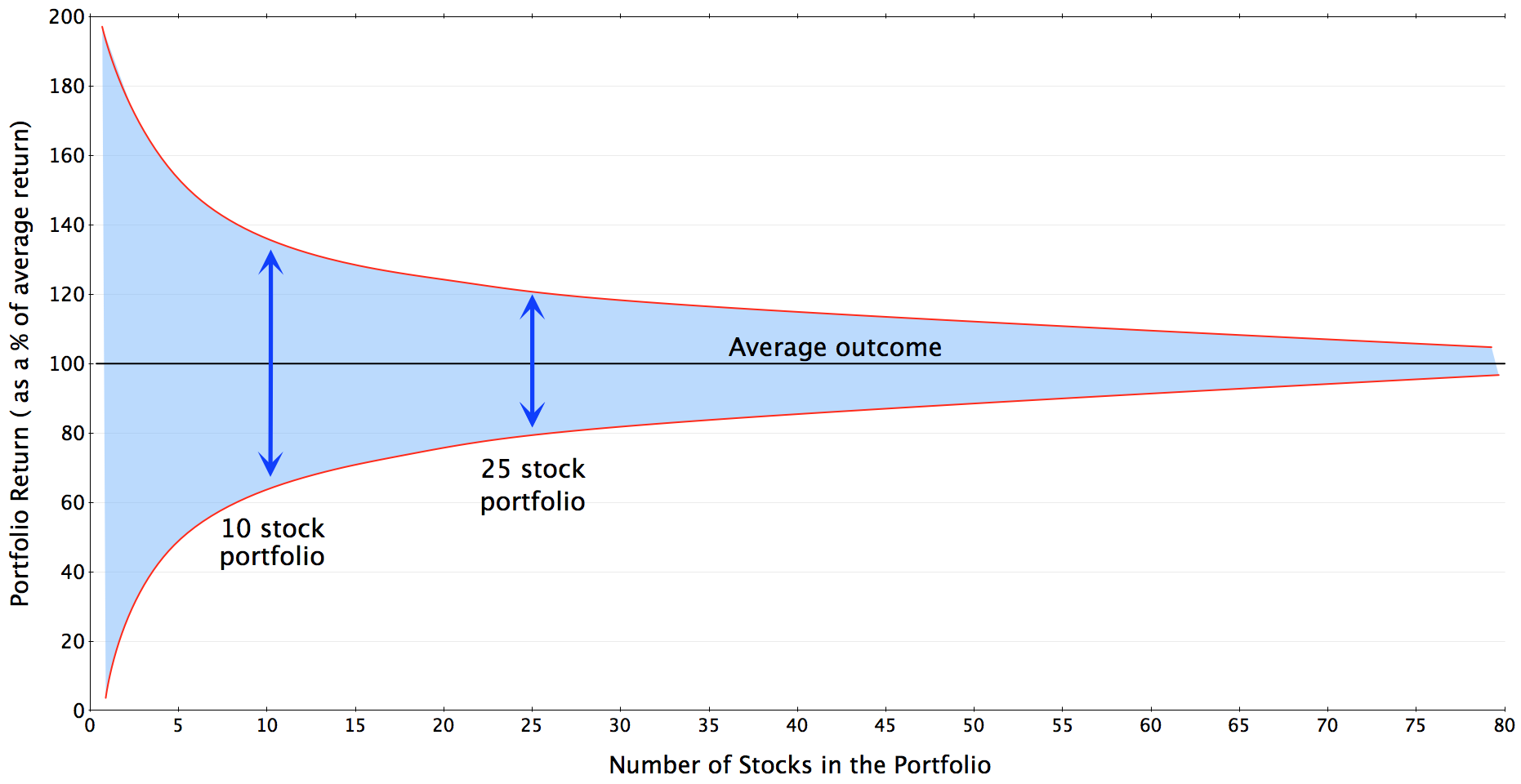

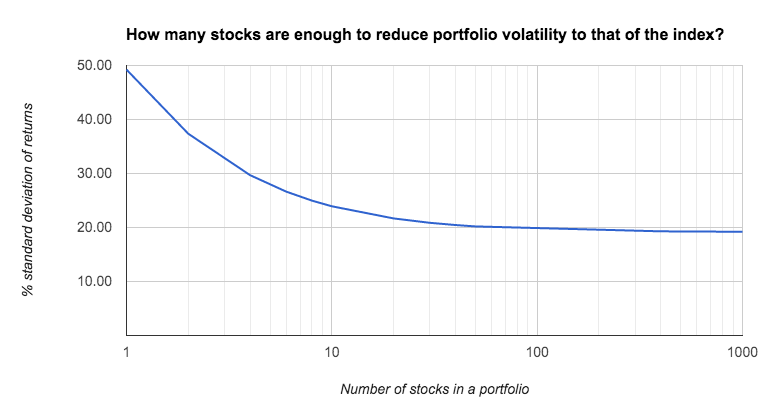

A famous study by Elton and Gruber in 1977 may have started the trend for heavy concentration in portfolios. It's conclusion was startlingly provocative, showing that most of the gains to be had from diversification come from adding just the very first few stocks to a portfolio.

According to these results adding just 4 more stocks to a 1 stock portfolio gives you 71% of the benefits of diversification (in terms of volatility reduction) of owning the whole market, with the benefits tailing off as you add more and more. The chart below using their data clearly illustrates this point.

These results were confirmed in a whole ream of follow up studies by other researchers in the 1980s and 1990s, the general consensus being that the purchase of anywhere between 8 and 20 stocks is 'enough'. But before everyone gets carried away and goes super-concentrated in their portfolios - lets step back and think about this a bit more.

The wrong kind of risk...

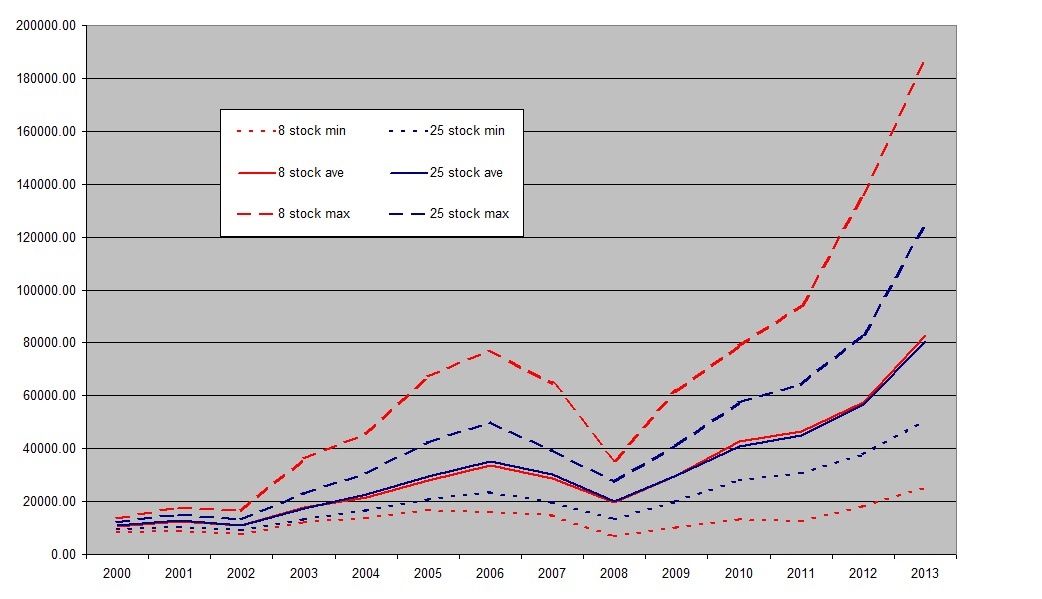

In 1996 Gary Newbould and Percy Poon, a pair of finance professors at the University of Nevada, published an article in the Journal of Investing which seriously challenged these results. The previous research had focused on how many stocks were needed to reduce volatility, but completely ignored the risk that the resulting portfolio would fail to show adequate performance.

"Individual investors face an enormous range of portfolio risk if…