Buffett calls the distinction between value and growth ‘fuzzy thinking’ because expected growth is a component of value.

If you think of a stock’s intrinsic value as its future cash flows discounted back to the present day at an appropriate rate - tricky to do in practice, but conceptually sound - then some cash-generative, high ROI stocks on a forecast PE of 50x are in fact cheap and undervalued.

It’s just that much of the value resides in future cash flows driven by present day investment. This future growth is hard to account for but that creates opportunities. Things seem expensive when they are in fact cheap.

So when should you buy a stock trading on a forecast PE of more than 50?

One possible answer is when you are presented with a scalable small cap software company that is a leader in a large market, with temporarily depressed earnings and strong long term shareholder/manager alignment.

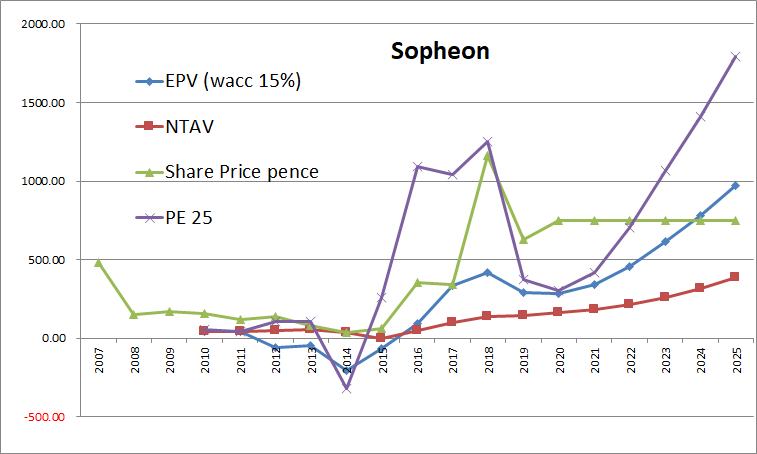

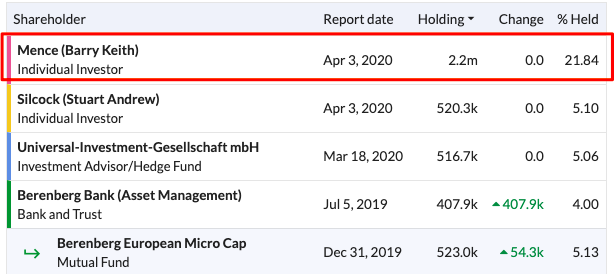

Sopheon (LON:SPE) could be one such case. The group’s shares are down by more than a third from all-time highs over the past year. Co-founder and long time executive chairman Barry Mence retains a large stake in the company though.

A founder/leader of a small company with a substantial shareholding is not a silver bullet, but that degree of focused management-shareholder alignment is very difficult to replicate at larger companies. It’s often a big plus.

Earnings have taken a temporary knock but if they can recover then the group’s shares at 870p might be cheap. Recovering to 2018 levels of profitability would imply a ‘normal’ PE ratio of just over 13x.

That comes with plenty of scope for growth as well, given SPE’s market cap of £89m and a growing net cash position on the balance sheet. Everything I’ve seen so far suggests SPE can increase cash flows and reinvest them back into high return growth projects.

In fact, this is exactly what SPE does for its clients...

What it does

As Bruce Greenwald famously concludes: ‘in the long run, everything is a toaster.’

Technological obsolescence and commoditisation are ever present risks in this age, and change is the only constant. SPE specialises in helping clients to optimise their own investments so that they can maintain their competitive edge.

It does so with software such as…

.jpg)