Last week’s offer for Micro Focus International (LON:MCRO) means that another well-established UK tech stock is likely to end up in North American ownership.

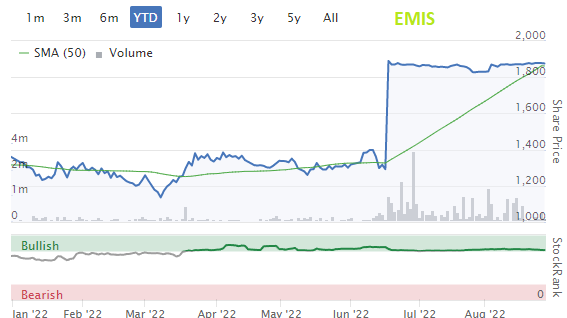

Micro Focus isn’t the first UK tech stock to succumb to a bid this year. In June, UK healthcare software group EMIS (LON:EMIS) (I hold) recommended a 1,925p per share bid from US group UnitedHealth to shareholders – a 49% premium to the prevailing share price.

EMIS sells software that’s used by GP surgeries and elsewhere in the NHS. Jack gave a good overview of the business back in May.

With the EMIS deal expected to complete later this year, I’ve been looking for similar stocks I might choose to replace this healthcare software group in my portfolio. I reckon that fellow AIM software firm Craneware (LON:CRW) could be an interesting choice.

Craneware (LON:CRW)

Craneware was founded by Gordon Craig and Keith Nielson in 1999. Neilson remains CEO and both men still have material shareholdings:

The company’s original product was the Chargemaster system. This helps US hospitals to accurately itemise and bill all of the chargeable services and products used by patients during their stay.

Craneware’s product range has since expanded significantly, but the company’s focus on helping US hospitals to maximise revenue and price accurately hasn’t changed.

The company expanded further last year when it acquired US firm Sentry Data Systems for $400m. Sentry appears to offer similar services for pharmacies to those that Craneware provides in hospitals.

I think it’s interesting to note that Craneware increasingly positions itself as a data company rather than a software firm. One of the selling points for the deal, according to the release, was the “commercialisation opportunity” for Craneware’s Trisus product suite that would come from access to Sentry’s 147m unique patient records.

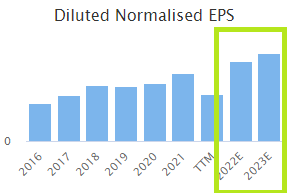

In the past, I’ve been attracted to Craneware’s high margins and recurring revenues, but discouraged by the stock’s strong valuation. That’s less of a problem now.

The group’s earnings stalled in 2018, which seems to have triggered a comprehensive de-rating of the stock:

However, broker forecasts suggest that Craneware's earnings are now expected to hit new highs, helped by the contribution from Sentry:

Craneware’s P/E…