Kelsian (ASX:KLS) has a portfolio of passenger transport assets and tourism assets. They were previously known as SeaLink Travel Group. Today they own fleets of buses and ferries in different locations in Australia, Singapore and the UK and recently acquired bus operations in the Channel Islands. Their portfolio includes about 4,000 buses and 113 boats.

The nature of the business is that they have long-term service contracts that are usually government backed. This enables a predictable revenue base. They are also able to pass on increases in fuel costs, wages and general inflation under the terms of most of the contracts which protects margins and reduces variability of bottom line profits.

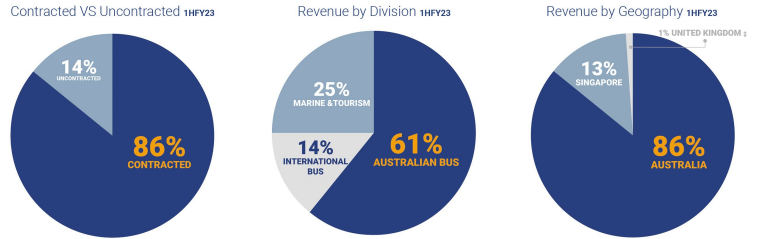

Revenue is diversified across business units and geographies, however Australian buses are the dominant contributor as outlined in the charts below.

Source: Kelsian Group Limited, FY23 Half Year Results Investor Presentation, 23/2/23

As would be expected, the pandemic marked a difficult period for Kelsian as people’s movements were greatly restricted. The impact was less pronounced for operations under government contracts, as despite the lower patronage, they still received payment to keep the routes operating. The impact was harder felt in the tourism segment where revenues are more closely tied to usage. 2020 was the only year in the last ten where they have returned a loss, and they were exceptional times.

The company has been growing its revenue at a very strong rate. From $200 million in 2017 to a forecast $1.4 billion in 2023 which equates to a compound annual growth rate of 46%. A large portion of this growth has come from acquisitions, but they have also been steadily winning additional contracts. Looking to the future, their growth strategies include looking to acquire bus and ferry assets in New Zealand, North America, Europe and parts of Asia.

But top line growth does not necessarily mean EPS growth. EPS was $0.23 in 2017 and $0.26 in 2022. Analysts are forecasting that it will reach $0.32 in 2023. The reason for this is that a lot of the growth has been funded by issuing new shares, so whilst the company today is bigger, long-term shareholders are not receiving much more income on their shares. Average shares on issue have gone from 104 million to 219 million.

The other component to funding…