Summary

Wholesaler Kitwave (LON:KITW) specialises in supplying frozen, chilled and ambient goods to convenience stores and foodservice businesses across the UK.

The group floated on the AIM market in 2021 and continues to be run by founder Paul Young. The shares score well for quality and momentum factors but remain reasonably priced, in my view. I think this business has considerable growth potential and recently added the shares to my SIF Folio.

Bull points:

Strong record of buy-and-build growth

High ROCE and good cash generation

Experienced owner-management

Reasonable valuation

Bear points:

Significant exposure to a few large customers

Exposed to macroeconomic headwinds in foodservice

Acquisitive model could go badly wrong

Profile

About the stock

Kitwave operates in the Consumer Defensives sector and is part of the Food & Drug Retailing industry group.

The group floated on the AIM market in 2021 and the stock has recently traded at 290p, giving a market cap of £202m. Liquidity is reasonable for a small cap, with a 73% free float and recent average volumes of c.300k shares per day – about £900k.

The StockRanks show high quality and momentum ratings, suggesting Kitwave could possibly fit the adventurous growth profile Megan discussed last week.

Kitwave shares have doubled since their IPO, but a forecast P/E of 11 and 3.8% dividend yield suggest to me that the business may still be reasonably valued.

About the opportunity

Stockopedia’s algorithms currently view Kitwave as a Super Stock.

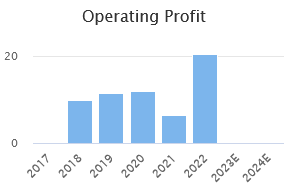

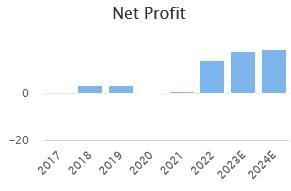

The business delivered organic revenue growth of more than 25% last year, together with improved profitability and strong cash generation.

Consensus forecasts suggest another strong performance during the year to 31 October 2023, with growth expected to flatten out during the following year.

At some point, I expect growth to slow as the business reaches a more mature scale. But the markets in which Kitwave operate are relatively fragmented and it may be possible for the company to continue expanding for some time yet.

Rival Booker (owned by