Time to don hard hats?

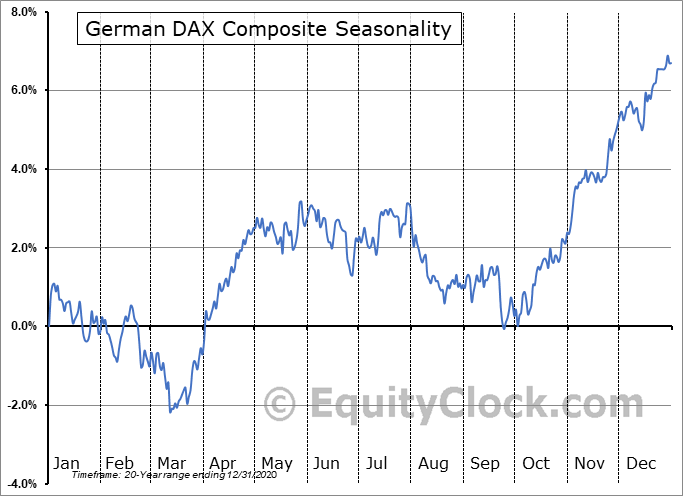

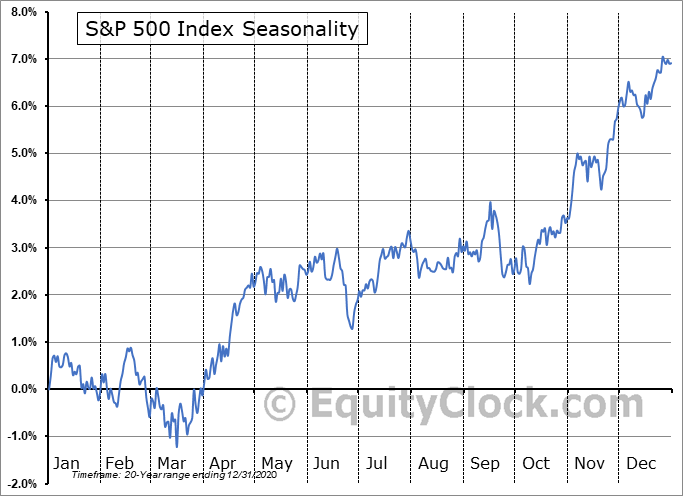

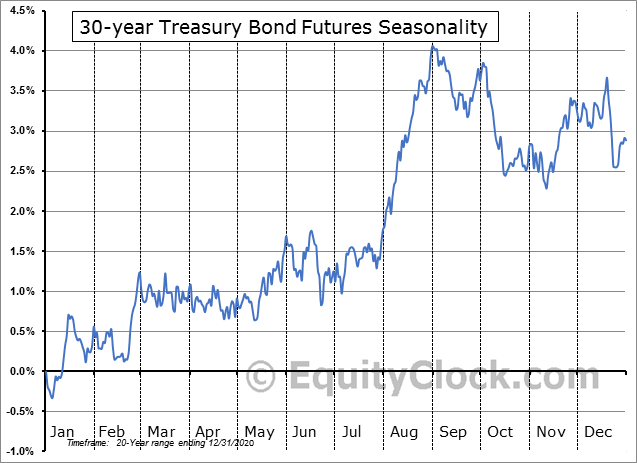

The end of July is here. August and September are typically the weakest months of the year for stock markets, so caution I guess is warranted if you are a stock market investor. European stock markets (like the German DAX) are typically weak over August and September, the US tends to move sideways, while bonds tend to gain.

European stocks suffer, US flatline, bonds gain over August + September

Source: equityclock.com

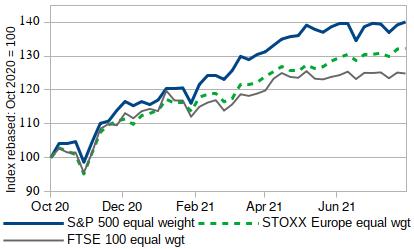

However, when we look at the evolution of stock markets this year, the trends remain firmly upwards for now. This is true whether you look at the S&P 500, the Euro STOXX 50, or even the UK stock market. The notable exception is emerging markets, dominated by The weakness in Chinese stocks as the Chinese government chooses to clamp down on tech companies in particular.

Equal-weight S&P 500, STOXX Europe continue to climb

Source: Bloomberg

In theory stock markets remain supported by two strong drivers. these are:

- strong earnings growth based on continued economic recovery

- long-term real interest rates that have returned to historic lows

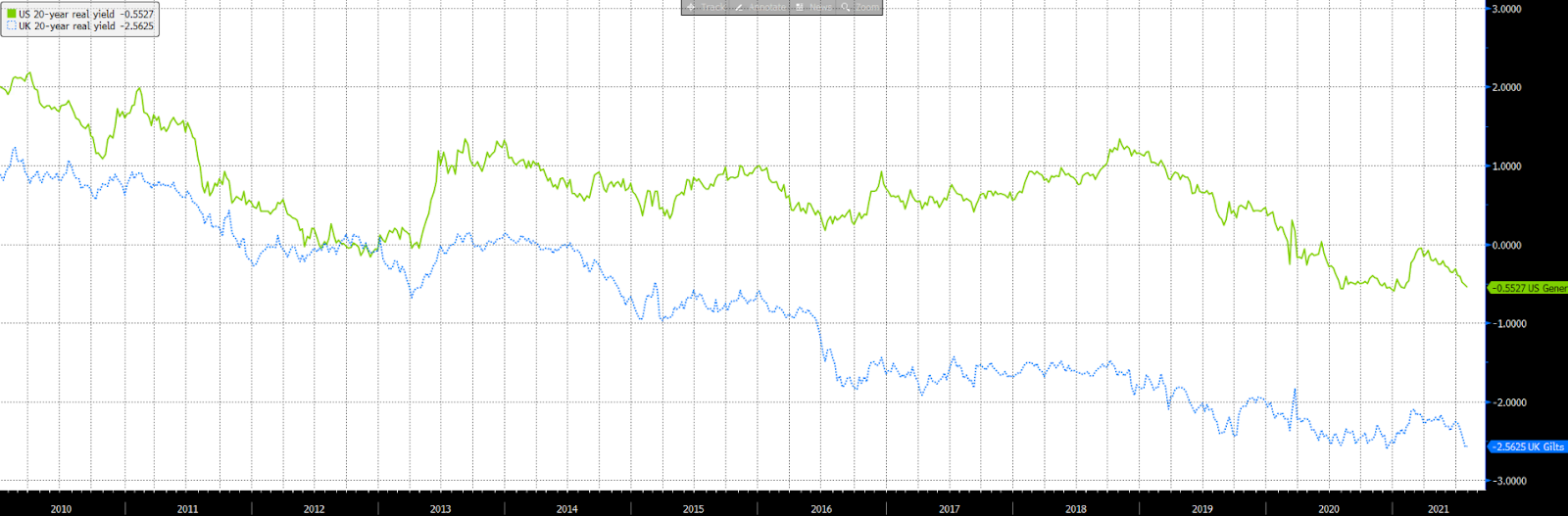

US, UK long-term real interest rates return to lows

Source: Bloomberg

Economic growth has peaked

But beware: global economic growth has already peaked, which was inevitable at some point as the impulse from government spending and extraordinarily easy monetary policy weakened. Interestingly, Bond yields have declined despite the rise in inflation rates. This is an unusual state of affairs, and suggests to me that the bond market is concerned about the withdrawal of government spending, combined with a more hawkish Central Bank, particularly in the US.

There is a risk that persistently high inflation could push the Federal Reserve not only to cut back their bond-buying program (so called tapering), but also to raise interest rates sooner than expected. Doing this at a time when growth is already slowing could even tip the US economy potentially into recession, in the worst-case.

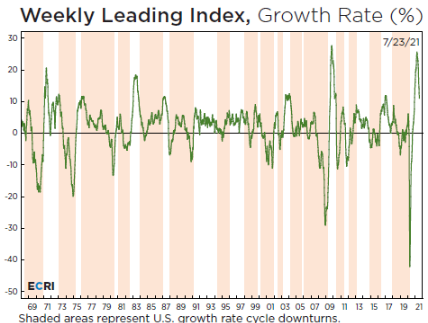

US leading economic indicator: growth momentum slows

Source: ECRI

TINA: There Is No Alternative has finally worked

Judging by the enormous retail investor flows into stock…