The UK back on the International Investment Radar

Summary:

- An amazingly strong week for the FTSE 100 at long last, post Brexit deal relief

- But note the scale of the under-performance of UK large-caps versus global stocks since the mid-2016 Brexit referendum

- New variant COVID v Vaccines: who wins?

- Inflation watch: Could the US see rising inflation soon?

- Precious metals: as buying opportunity post Friday’s sell-off

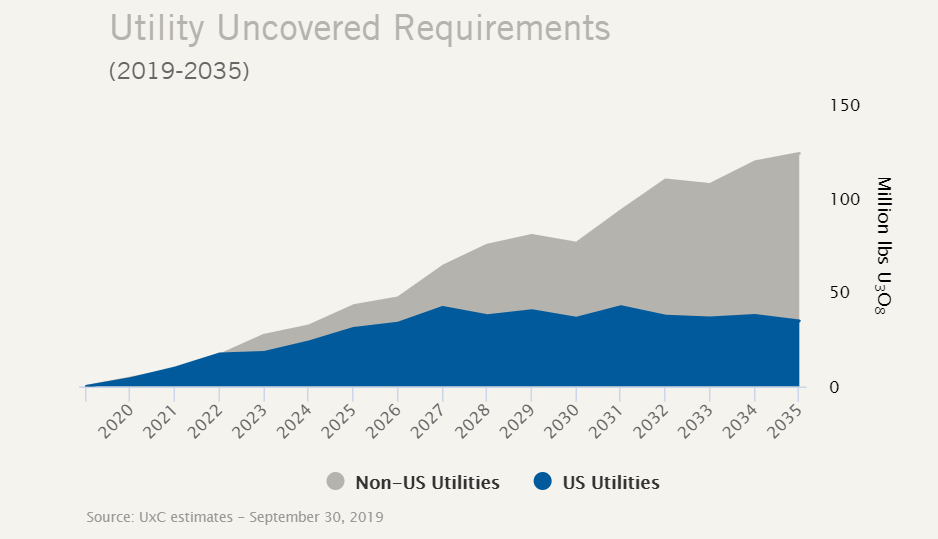

- Uranium: an energy commodity finally coming in from the cold?

Brexit deal relief boost UK stocks

This last week has been impressive for UK stock market indices notably the FTSE 100 large cap index. Clearly, the Brexit trade deal signed at the last minute with European Union has been an important catalyst for UK stocks. The 6.5% advance for the FTSE 100 over the last week has been impressive, led by a number of cyclical stocks that benefit from rising bond yields such as UK banks.

Within the UK large-cap index, I continue to prefer international sectors such as the mining sector, for its exposure to both precious and base metals. As for the domestic stocks, the real question remains as to whether the renewed UK lockdown will hurt performance, or whether investors will instead look to the spreading covid vaccination program for more medium-term optimism. For now, it is clear that investors are looking more to the medium term and are less worried, at least for the moment, about the short term progression of the new variant of the coronavirus.

But if we look to the longer term, it is quite clear from any cursory examination of the performance of the various UK indices by size of company, that small caps and indeed mid caps have vastly outperforms the FTSE 100.and, if we really are to expect a strong economic recovery over the course of 2021, then it is likely that small and mid-cap stocks will again shine brighter than the FTSE 100.

For me, The catalyst for this continued out performance of small and mid-cap stocks would be an acceleration in the covid vaccine nation programme combined with a release from lockdown, which would then potentially release pent-up consumer demand. We should remember that savings rates have remained high over much of 2020, and preliminary evidence from pre-Christmas trading from retailers such as Sainsbury suggest that consumers are ready to spend more money once they can once again.