In my last piece I looked at three big cap FTSE 100 stocks that scored highly in my recent momentum screen. I drew mixed conclusions about the outlook for these businesses. But I believe I’ve found some more promising opportunities among the smaller companies in the results of my momentum screen.

This week I’m going to look at two mid-cap stocks from my screen that I think could do well on a medium-term view. As always, please let me know what you think if these two businesses in the comments below.

Qinetiq (LON:QQ.)

Last week I looked at defence group BAE Systems. This week I’m looking at a smaller company from the UK defence sector, FTSE 250 member QinetiQ (LON: QQ.).

This stock stumbled in October last year when the company revealed a £15m impairment charge due to “technical and supply chain” issues. However, investor confidence has returned quickly, perhaps due to QinetiQ’s solid longer-term track record:

About QinetiQ: This business was spun out of the Defence Evaluation and Research Agency (DERA) when it was privatised in 2001. Historically, QinetiQ was heavily reliant on a handful of MoD contracts to run facilities such as firing ranges and pilot training, but it's been diversifying in recent years.

The company’s focus is on providing services and specialist technology systems. Examples include launch and arrest systems for aircraft carriers, mission training and simulation, cyber security and targets for live-firing exercises.

Today, the business is built around six core areas of expertise:

- Experimentation and technology

- Engineering services and support

- Cyber and information advantage

- Robotics and autonomous systems

- Test and evaluation

- Training and mission rehearsal

QinetiQ still generates 70% of revenue in the UK, but the company is now focused more broadly on the AUKUS markets – the UK, US and Australia. These countries account for more than 90% of revenue, with the remainder coming from a RoW segment:

Source: QinetiQ half-year results presentation (Nov. 2022)

Management believes that all of the group’s markets offer significant growth opportunities, with a total addressable market of at least £20bn.

Financial performance: Revenue growth has been admirably consistent in recent years, and broker forecasts suggest this performance will continue:

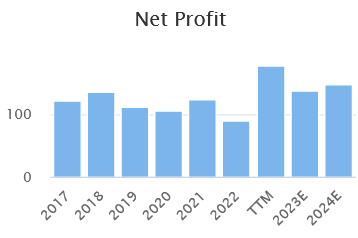

However, profit progression has been much weaker:

This has led…