It’s not everyday that you see an $8B company double in size over 6 months.

And so it is the case with Mineral Resources (ASX:MIN) who from their recent lows of $42.89 in July 2022, has risen by over 100% to now be $88.35 and a $16.6Bil company.

Mineral Resources for those may not be aware is a diversified resources business with interests crossing:

Lithium (World top 5 lithium producer)

Iron Ore (Australian top 5 iron ore producer)

Mining Services (MIN is the world’s largest crushing contractor)

Energy (Largest landholder of gas acreage in Perth and Carnarvan basins)

The success of MIN has led to long-serving MD Chris Ellison to be elevated onto the front pages of the financial press as a pin-up boy for the industry. While this is traditionally a point where I get nervous, Mr Ellison has not sought the limelight, rather the light has found him through the extraordinary numbers they have produced.

As with any company who experiences such rapid rises we need to, first congratulate holders, but then also ask ourselves from this point what are the likely prospects of MIN moving forward and how does the company stack up overall as a potential investment opportunity.

StockRank ™

It may come as a surprise to some that a company with a market cap touching $10B could have an overall StockRank score below 70. We will discuss that now.

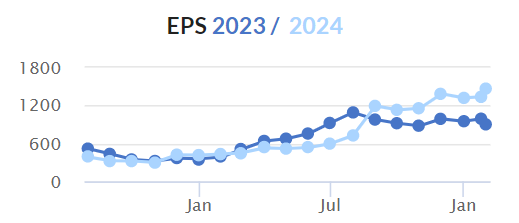

Obviously the 92 for momentum stands out. Not only because of the extraordinary price rise, but also for the fact that analysts had been upgrading their forecast EPS for the company for the past 12 months.

However it should be noted that for the FY23 forecast (the darker line), EPS forecasts have actually moderated somewhat since July, and even after their most recent quarterly (which I will discuss in a moment) there has been a slight downgrade again. Fortunately FY2024 doesn't seem to have been affected and MIN continues to maintain its solid earnings momentum trajectory.

Price too has obviously been on a strong trajectory reflecting the business trajectory of the past 12 months. The price pullback…