Technology stocks on the ASX have been on a tear, with the S&P/ASX All Technology Index having produced a total return over the last 12 months of 62.6%. A technology stock that tends to fly beneath the headlines is Objective (ASX:OCL). Maybe that is because it has underperformed the index with a total 12 month return of a mere 56.7%.

Or maybe it is due to the nature of the business. They provide solutions for public sector organisations and regulated industries. How boring is that? Surely that can’t be a growth industry?

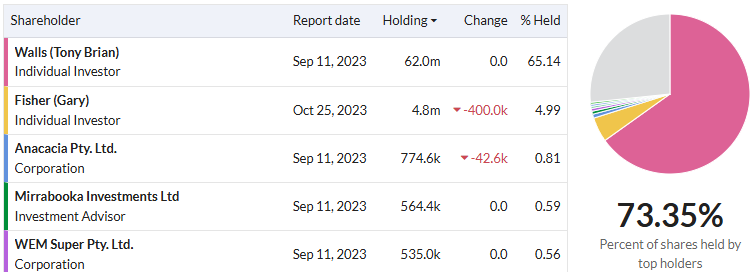

It is also a very tightly held stock.

Tony Wells is the founder, Chairman and CEO and holds 65% of the stock. Gary Fisher, who was a director from 1991 to 2023 holds a further 5%. The total market capitalization is $1.65 billion, so this leaves a free float of approximately $500 million. Still a substantial amount when compared to other small cap stocks. There has been an average daily traded value of $860k over the last year.

Objective is not a new start up with a hot idea surrounded by a lot of marketing hype and buzz words. They were founded 37 years ago and have been listed on the ASX for over 25 years. Their key target markets include governments, councils, regulators and local planning authorities. They break out their revenue according to three main product lines:

Financial year 2024

Content solutions | $80.3m | 68% |

Regulatory solutions | $22.2m | 19% |

Planning and building | $12.3m | 10% |

Public sector organisations are subject to increasing public expectation that they will offer efficient digital solutions. Objective are helping these businesses to go completely digital.

In terms of their own business model, they have now transitioned themselves to a subscription only software business. 81% of their revenue is recurring and they have low churn rates. Software as a service (SaaS) businesses like to measure their annual recurring revenue (ARR). Objective have now passed ARR of $100 million. Their total ARR grew by 11% in FY24 and their SaaS ARR grew by 15%. They were targeting total ARR growth of 15% but fell short due to the late deferral of several material opportunities. Also, soft economic conditions in NZ led to soft building consents in NZ where they have a pure transaction…