The December OPEC meeting in Vienna is coming and the picture of the oil market is mixed at best:

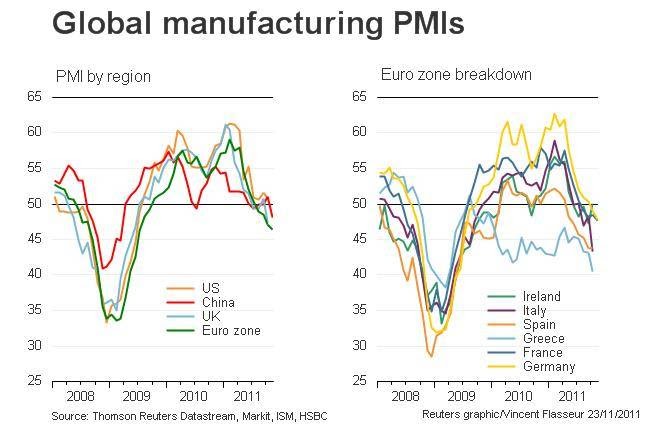

1) China PMI below 50 for the first time since Feb 2009. Global manufacturing PMIs remain weak as the table below shows, particularly in Europe.

2) Bearish US DOE weekly with high inventory build and very low implied demand. The EIA's monthly revised oil demand numbers for September came in at 18.8m bpd, which was down from 19.05m bpd. It was also down 0.7m bpd y-o-y.

3) OPEC production in November: came in at 30.35m bpd, up 390k bpd from October, according to Bloomberg. Increase led by Libya (155k bpd), Saudi Arabia (65k bpd) and Iraq (50k bpd).

In the meantime, geopolitical concerns surrounding Syria and Iran, added to the inflationary pressures of the constant reduction of interest rates in Europe and Australia more recently, have kept oil prices at a very strong level, with Brent at $109.6 at the close of this post.

To me, one of the most interesting trends is that heavy oil continues to re-rate and that Tapis (Asia) remains at a healthy premium to Brent, proving that Chinese and Asian demand remains solid despite the weakness in the data.

In this environment, another interesting trend is shown by the significant increase in the break-even price required by producers to balance their budget. At $80/bbl, Saudi Arabia's commitments to invest in social peace and support the MENA stability is starting to prove costly. But still very comfortable versus the market price. Otherwise, Russia's $110/bbl is a reflection of the strong investment commitments of the country, which are likely to slow down in the next years, so the headline number of break-even price might be overstated in the mid-term.

Considering this, it is not hard to understand why the OPEC World Outlook Reference Case oil price assumption has been increased from last year. It is assumed that, in nominal terms, prices stay in the range of $85–95/b for this decade, compared to $75–85/b in last year's expectation.

At the same time, global refining capacity is soaring and excess capacity is likely to reach 10mmbpd. This will have a significant impact on refining margins and, as such, high oil prices might be cushioned for the final price paid by the consumer by lower…

About the Author

Dlacalle

0 comments