Back in September 2025, I published an article on the UK’s listed brick producers, noting how brick deliveries had risen sharply from the lows seen in late 2023.

At the time I highlighted recently-increased volume guidance from several big housebuilders, but suggested that brick producers looked the better play to me at that time.

One reason for this was that an increase in brick shipments would provide a rapid lift to profits for brick producers as capacity utilisation rose. In contrast, housebuilders’ profits came later in the day and are more vulnerable to political and macroeconomic pressures.

My plan was always to follow up with a look at housebuilders and my attention was recently caught by the news that planning applications for new housing in England hit a 10-year high in 2025.

Is it time to take a closer look at housebuilders?

Refilling the pipeline?

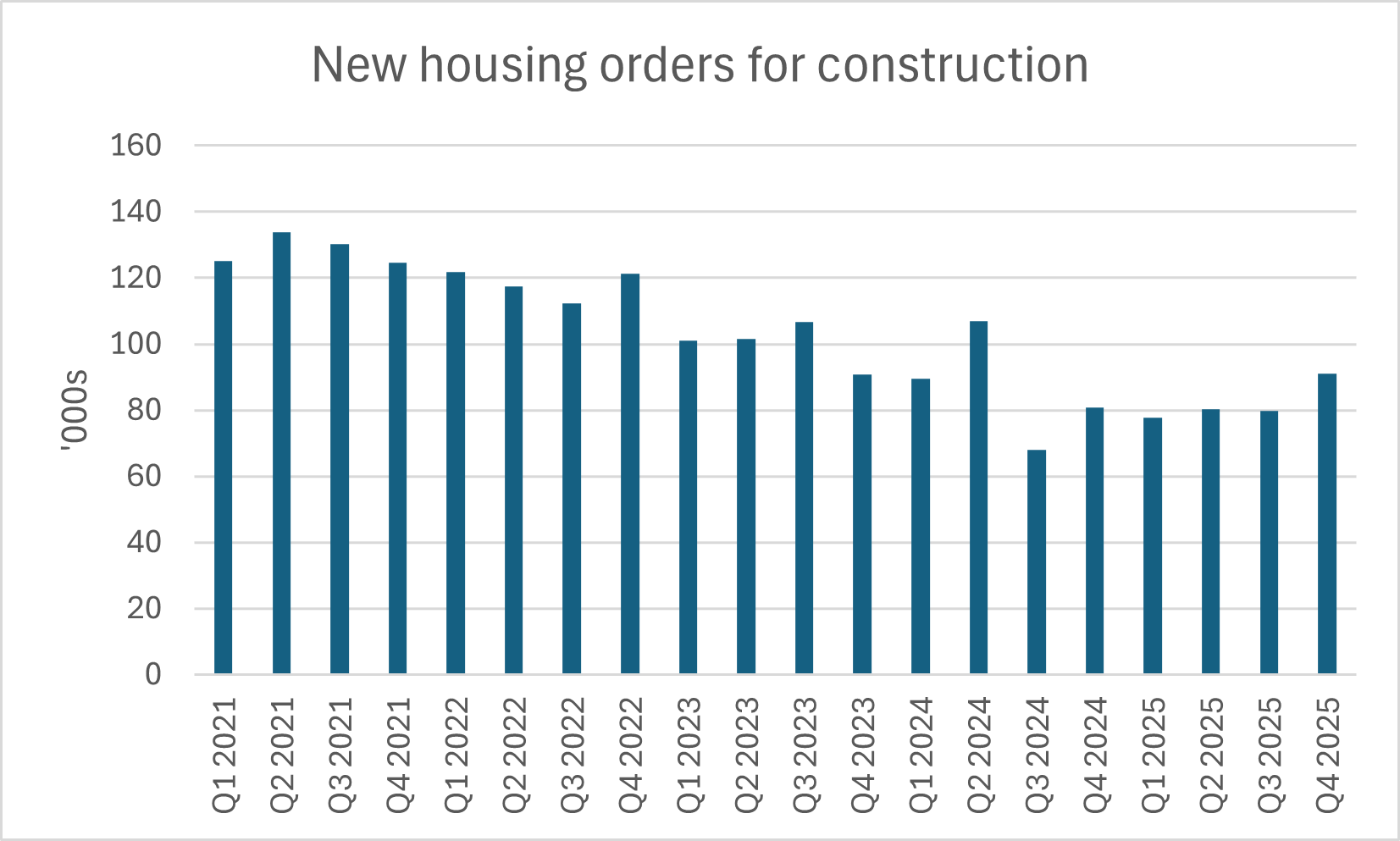

It’s no secret that new housing starts have plummeted since 2023, reaching a post-pandemic low ahead of the Autumn Budget in 2024. But recent data do give me some hope that a gradual recovery might be underway.

Last year saw a sharp rise in new housing orders for construction (contracts signed to build new housing). These rose by 14% sequentially during the final quarter of last year and were also 12.6% higher than the same period one year earlier:

Data source: ONS

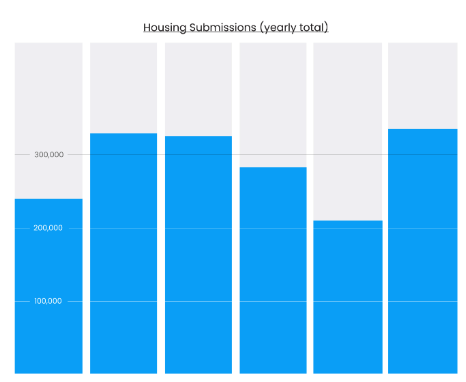

There are also signs the medium-term pipeline of planned housebuilding might be improving.

Planning applications for new homes in England reached a 10-year high during the final quarter of last year, according to planning services specialist TerraQuest:

Source: TerraQuest (l-r 2020 - 2025)

TerraQuest’s data shows that planning permission was sought for 335,387 new housing units in 2025, more than 50% above the level of applications seen in 2024.

There is a caveat here, of course. Planning approvals in England have fallen in each of the last four years:

| Year ending | Units granted planning | Percentage change |

|---|---|---|

30 Sept 2021 | 325,000 | |

30 Sept 2022 | 290,000 | -11% |

30 Sept 2023 | 254,000 | -12% |

30 Sept 2024 | 245,000 | -4% |

30 Sept 2025 | 208,000 | -15% |

Source: Ministry of Housing, Communities & Local Government

Regardless of the cause of this decline – planning delays, policy uncertainty or…