At over $20 billion dollars a year, nickel is already one of the world’s most important metal markets. However, with the rise in demand for electric vehicles, nickel is potentially on the cusp of a fundamental supply shift where quality over quantity comes crashing to the fore.

That’s because not all nickel is created equal.

Approximately 62.4 percent of today’s nickel supply is nickel laterites, which produce products such as nickel pig iron and ferronickel. While abundant, these low-grade metals are inadequate for battery manufacture. Instead, the growing demand for EV battery components must be met by higher-grade––but much rarer––nickel sulphides, which produce such products as nickel metal and nickel sulphate.

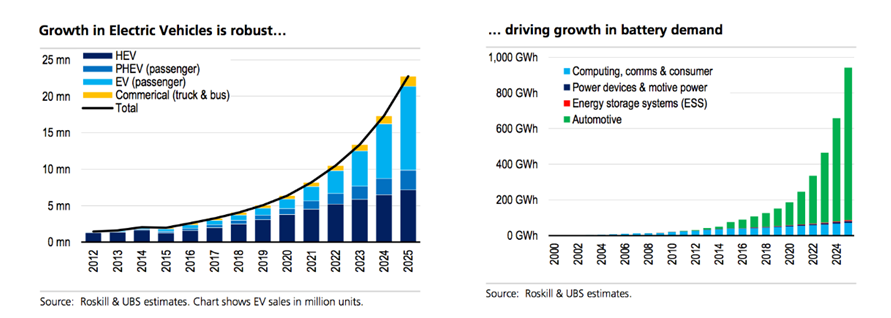

- Only 15kt of nickel was sourced from finished (Class 1) nickel in 2017; a single Chevy Bolt features 23kg of nickel in its battery.

- Future battery chemistries are expected to contain more nickel, not less––comprising up to 80% of the battery cathode mass used by companies like Chevy and Tesla by 2020

- Source: Nickel: The Secret Driver of the Battery Revolution

Class 1 nickel (high purity) and Class 2 (lower purity) nickel and sulphide ore versus laterite ore

Class 1 nickel is the high purity nickel that is used in electric vehicle lithium ion batteries. The stainless steel industry uses both class 1 and class 2 (lower purity) nickel, and is the main driver of nickel demand.

The nickel sulphide ore deposits are the better source for class 1 nickel needed to make nickel sulphate for EV batteries, and typically have significantly lower production and CapEx costs. Class 2 nickel from nickel laterite ores can be converted to nickel sulphate however it requires high pressure acid leaching [HPAL], which is expensive with much larger CapEx requirements. Much of the laterite ores come from the rim of fire regions such as Philippines, Indonesia [PNG] and New Caledonia. Most of the sulphide ores come from Russia, Canada, and Australia.

McKinsey state in their November 2017 report, The future of nickel: A class act (emphasis added):

"Currently, class 1 nickel supply suitable for battery production represents approximately half of global supply of 2.1 million metric tons [MT] – although only 350 metric kilotons [KT] is available to be processed into powder and briquettes that could be used to produce nickel sulphate (in 2017 approximately 65 Kt to 75 Kt of nickel content will be used to make…