So far, I have written about many of the well-known value ratios: Price-to-Tangible-Book-Value, 52-Week Lows and earnings-based metrics. However, one classic remains: Price-to-Sales.

Price-to-Sales studies

Although the academic finance literature primarily focuses on Price-to-Tangible-Book, Price-to-Sales has a long history among practitioners. For example, in his book, What Works on Wall Street, Jim O’Shaughnessy describes Price-to-Sales as the King of the Value Factors. And I can see why:

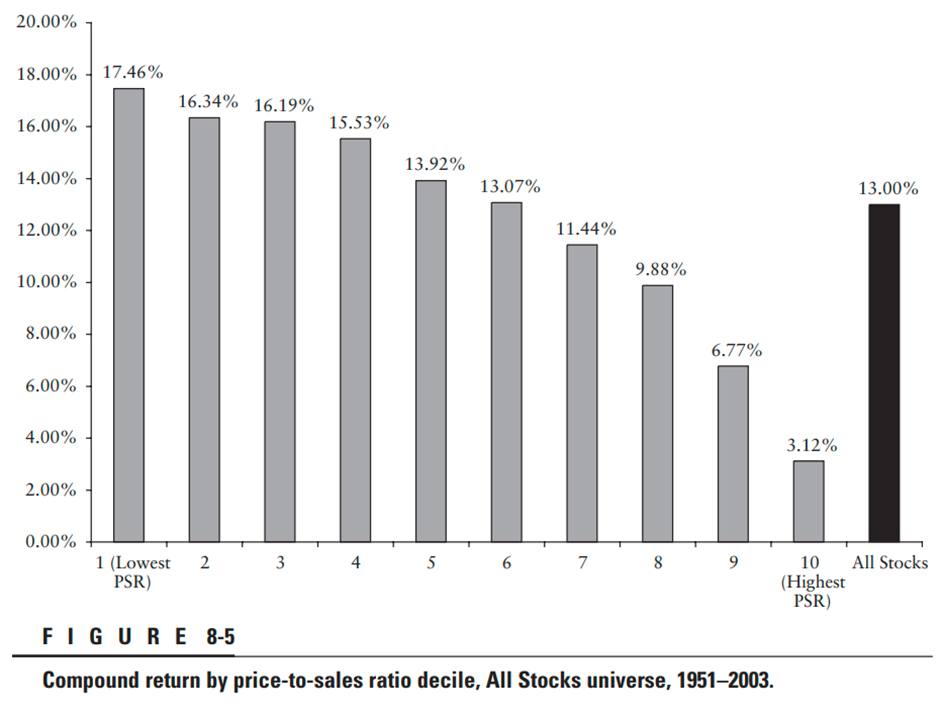

In his study of US stocks from 1951-2003, buying the lowest decile of stocks on Price-to-Sales generated more than a 17% compound return. Better than Price-to-Book, price-to-cash flow or Price-to-Earnings. Although, the differences were not huge, and more recent studies have tended to prefer earnings-based metrics for the best-performing lowest decile. What is noteworthy, however, is how badly the highest Price-to-Sales decile did. This generated just a 3% compound return, less than inflation for the period. In the same study, the highest Price-to-Earnings stocks also did poorly. However, they still generated a 9% annual return since this was a strong period for general stock market returns in the US. This is far more than high Price-to-Sales stocks managed. So if you want to implement a long-short value portfolio, Price-to-Sales may be the one to use.

The problem of high Price-to-Sales

Even if investors are not interested in such quant adventures, it is worth bearing in mind what a high Price-to-Sales ratio means for a stock. While a small company is growing revenue rapidly, investors can justify paying a high Price-to-Sales ratio. However, when it comes to larger and more mature businesses, it can often be a signal indicating overvaluation. One of the most famous explanations of the pitfalls of buying a mature company on a high Price-to-Sales ratio comes from a March 2002 Bloomberg interview with Scott McNeely. McNeeley is the former CEO of Sun Microsystems and was commenting on his own company’s valuation at the peak of the dot com bubble:

At 10 times revenues, to give you a 10-year payback, I have to pay you 100% of revenues for 10 straight years in dividends. That assumes I can get that by my shareholders. That assumes I have zero cost of goods sold, which is very hard for a computer company. That assumes zero expenses, which is really hard with 39,000 employees. That assumes I pay no taxes, which is…