When I sell a company from my portfolio, I don’t usually look back. But I’m starting to wonder if I should consider buying back into consumer goods group PZ Cussons (LON:PZC), which I ditched in 2024 after it ran into a raft of problems (and lost a lot of money).

The best consumer goods businesses are naturally defensive and can deliver reliable long-term performance and growth over remarkable timeframes. While I’ve been fairly critical of PZ Cussons in the daily report over the last couple of years, recent news from the company – which is a long-term holding of noted private investor and ISA millionaire Lord Lee – has left me feeling much more positive.

A Stock Pitch review provides the ideal opportunity for me to revisit the story and ask whether I should consider another investment in this venerable, family-controlled business.

Share price at the time of publication: 80p

Market cap: £337m

Disclosure: at the time of publication, Roland has no position in PZC.

The Pitch

PZ Cussons owns brands including Imperial Leather, Carex, Cussons Baby and many others:

Source: PZ Cussons website May 2026

The group can trace its history back back to 1884, when it was founded by George Paterson and George Zochonis (PZ) as a trading business in Sierra Leone. It’s been listed on the London Stock Exchange since 1953 and merged with Cussons – itself founded in 1909 – in 1976.

Recent years have seen difficulties with underperforming brands, a sprawling cost base and some painful currency losses in Nigeria. However, the company has now tightened its strategy around its core Hygiene, Baby and Beauty categories and refocused on its core geographic markets.

I think the business could be turning a corner, but I don’t think this is reflected in the current valuation; a forward P/E of 10 is unusually low for a branded consumer goods group.

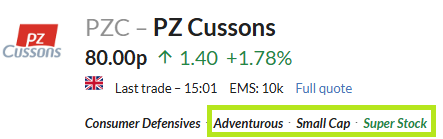

In March, the company guided for FY26 results to be “at the upper end of guidance”. The StockRanks also paint a relatively optimistic picture:

If the company can continue to hit forecasts in FY27, I’d expect the shares to perform well.

The Big Picture

Like its much larger rival, Unilever (disc: I…