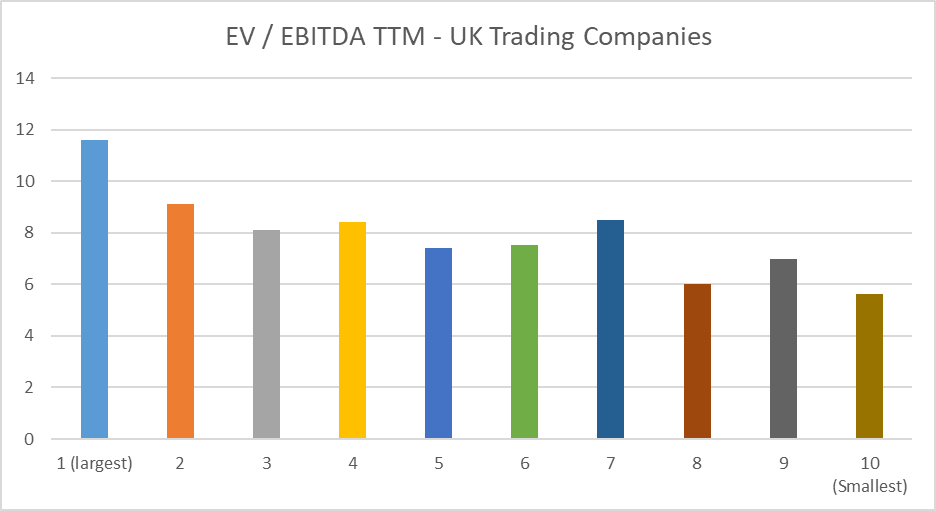

There is no doubt that recent global events have thrown a spanner into the works for many investors. For a while now, I have been pointing out the value disparity between the larger companies and the smaller ones in the UK:

Almost all international funds from asset allocators have flowed into FTSE 100 companies (roughly the first decile). The UK has looked cheap compared to other developed markets, particularly the US, which has led to positive fund flows into the largest UK stocks. In contrast, smaller companies are much more at the mercy of UK-based individual investors, either through their direct equity exposure or through small and microcap funds. Here, confidence has been weak for several years, leading to the smallest stocks trading at less than half the EV/EBITDA multiple of the largest (on average).

It is worth noting that, as long as investors focus on profitable stocks (the smaller-company tail has a higher proportion of more speculative stocks), I can find no difference in quality or outlook between the largest and smallest companies. In fact, small companies appear to retain the stronger growth prospects that typically accompany their nimbler approach, which is usually rewarded with a higher rating than larger companies.

Larger global asset allocators tend to be slow to react, which means that the FTSE100 weakness has largely tracked global equity markets. These have no doubt been painful moves for investors. However, at the smaller end, we have seen some precipitous sell-offs, especially in more popular stocks. The valuation disparity in the graph above has made little difference to investors, as there has been a dash to cash at any price, whether through conscious decision-making or stop-losses.

What was shaping up to be a good year of recovery for those who held cheap small caps is now looking like another year to forget. With small caps once again taking a battering, strategies that tend to be market-cap neutral, such as StockRank-based ones, may face some short-term challenges.

Is this logical?

The ability to act quickly to changing market conditions is one of the benefits of managing one’s own portfolio. When the outlook sours considerably, and higher energy prices and interest rates put a dampener on economic activity, individual investors don’t have to wait for an investment committee decision to get out. The big question is, should they?

On…