At the start of 2022, Royal Mail (LON:RMG) was flying high. The company had reported near-record profits for the two years of the pandemic and appeared to have recovered both its profitability and its mojo following a boardroom shake up.

Unfortunately, events this year have suggested that Royal Mail’s postal business still has the same problems with modernisation, workforce relations, and declining letter volumes that dogged it before the pandemic.

Royal Mail Group shares are now back at pre-pandemic levels:

Recent trading: The group’s first-quarter trading update revealed that revenue fell by 11.5% year-on-year in the Royal Mail postal division, leading to a Q1 operating loss of £92m. The postal operator hopes to break even at an adjusted operating profit level over the full year.

This was a notable contrast with RMG’s other division, international parcel operator GLS, which owns Parcelforce. GLS reported a 3% fall in volumes but said that revenue rose by 7.8% during the quarter, including acquisitions.

Inflationary pressures are putting last year’s 8% operating margin under pressure at GLS, but management still expects this business to generate an operating profit of €370m-€410m this year.

Royal Mail Group chairman, Keith Williams, says that the problem at Royal Mail is that efficiency improvements have stalled and the postal workers’ union won’t accept changes to working practices. He’s planning to end cross-subsidy between GLS and Royal Mail and has threatened to consider splitting the two businesses if no solution can be found.

I can’t predict how all the human and political elements of this situation will turn out. But I can see some reasons to believe that the shares offer value at current levels, however the situation evolves.

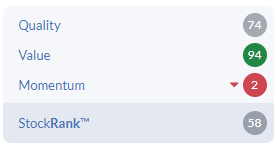

Stockopedia’s algorithms appear to share this view. Royal Mail is badged as a contrarian stock at the moment.

That suggests a mix of good value and quality, but poor momentum. In other words, the shares could be cheap if earnings stabilise:

Let’s take a closer look.

Great value?

Royal Mail is often talked of as a value stock due to its large property portfolio, cash generation and apparently modest valuation.

Book value: Royal Mail does indeed have plenty of fixed assets. The group’s property, plant and equipment (PP&E) was…