Insurance stocks can generate attractive returns and reliable cash flows – just ask Warren Buffett. But these specialist financials aren’t without risk, so in my experience it’s wise to focus on companies with proven financial strength and underwriting discipline.

In this Stock Pitch I’m going to take a look at niche motor insurer Sabre Insurance (LON:SBRE) and explain why I think this company offers an attractive mix of strength, discipline and growth potential.

Share price at the time of publication: 165p

Market cap: £408m

Disclosure: at the time of publication, Roland has no position in SBRE.

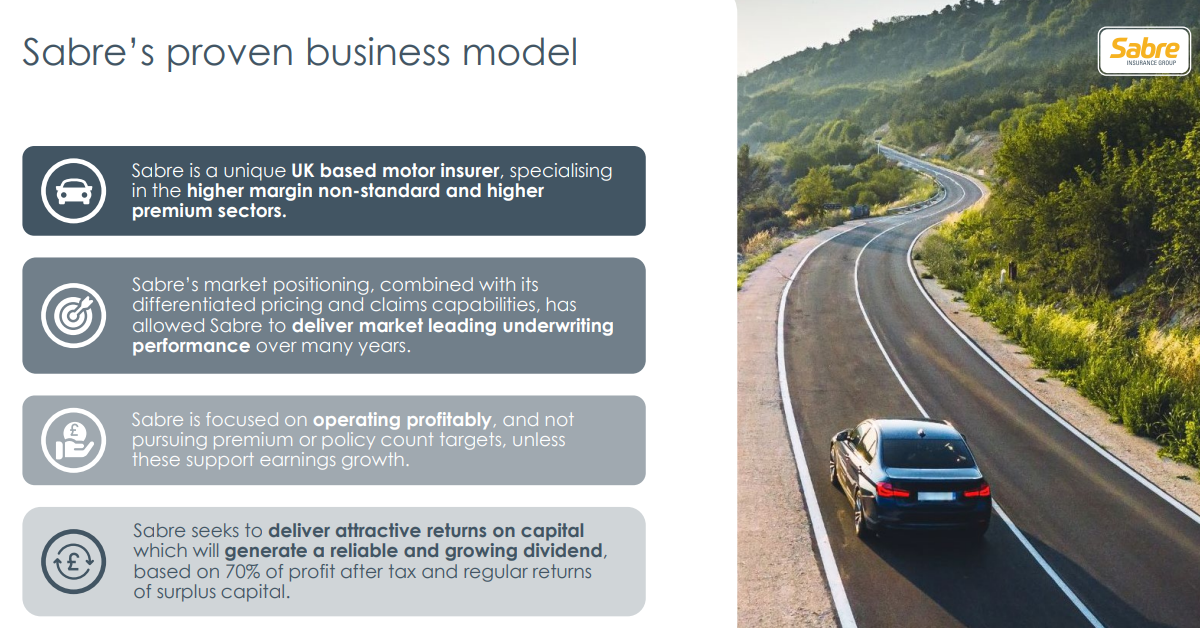

Source: Sabre Insurance website June 2026

The Pitch

Motor insurance is a ruthlessly competitive sector that’s exposed to macroeconomic pressures. Investors were reminded of this when even UK sector leader Admiral saw its profits halve in 2022. Others fared much worse.

Sabre sidesteps the bear pit of competing solely on price by focusing on more profitable and less competitive sub-segments within the overall motor market. These include “high-premium, high-margin policies” for riskier car drivers, plus coverage for taxis and motorcycles.

The business sells policies through brokers and directly through its own brands, which include Insure2Drive, GoGirl and Sabre Direct.

Despite its small size, Sabre has established a reputation for skilled and disciplined underwriting – management aren’t afraid to turn down volumes to protect margin.

Source: Sabre Insurance Capital Markets Update 2024

The company has now embarked on an expansion plan targeting pre-tax profit of “at least" £80 million in 2030. That’s equivalent to an annualised growth rate of around 9% per year from the 2024 figure of £48.6m.

If the company can hit this target without any mishaps, my number crunching suggests that the shares could enjoy a material re-rating from current levels. In the meantime, Sabre offers a forecast dividend yield of 8% – potentially tempting.

The Big Picture

Sabre has a solid track record of profitable underwriting in its core markets of higher-risk car drivers, taxis and motorcycles. As broker Panmure Liberum commented in March, the company’s “previous strategy of focusing on profitability over volume has worked well, ensuring positive earnings throughout, unlike peers” (my emphasis).

The company’s new growth…