In my last article, I started to look at some of the companies highlighted by the 52-week low screen. Although very few companies will appear on a 52-week low screen when everything about their trading and outlook is rosy, more severe issues led me to exclude some companies from further analysis. I excluded two companies due to excessive debt or pension liabilities. I also excluded two companies because their StockReport highlighted a high risk of earnings manipulation, and their area of operations meant I could not get comfortable with these risks. Finally, three other companies were flagged as at risk of earnings manipulation: Gear4music Holdings (LON:G4M), Capital (LON:CAPD) and £SLP. However, looking at the results announcements directly, they didn’t seem unusual for such companies. So I choose to include these in my further analysis. However, investors may want to conduct their own investigation into these issues.

This left 22 companies that warranted further investigation. In this article, I am going to look at nine of them – the ones that fall roughly into the categories of Retail, Media, and Investment Companies:

Retail

Angling Direct (LON:ANG)

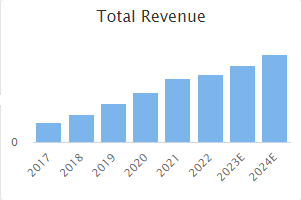

Angling Direct is a specialist retailer that, unsurprisingly, sells fishing tackle, both online and through a network of 42 stores. Revenue growth here is impressive:

Although EPS is much more patchy:

The latest trading update, as part of their full-year results in May, says that, although they are not immune to inflationary headwinds, they expect to trade in line with current market expectations this year. This puts them on a forward P/E of 14.5, so not exactly cheap in the current market.

However, the business has been highly cash-generative and has built up £16.3m of cash at the last balance sheet date. And this is not achieved by stretching their working capital either, with net working capital standing at +£8.1m. I would expect that there may be some working capital movements during the year - retailers don’t pick 31st January as their year-end for nothing - but this still represents over half the market cap. Unfortunately, there is no dividend paid by the company with them choosing to re-invest in growth. However, they spent money on four new stores, a European distribution centre and their IT platforms last year, yet still generated free cash…